Financial Health Pulse® 2022 U.S. Trends Report

Financial Health Snapshot 2022

The percentage of people spending less than their incomes, reductions in short-term savings, and confidence in long-term savings all contributed to negative trends in financial health between 2021 and 2022. The percentage of people reporting spending less than their incomes hit the lowest level since 2018, our first year of Pulse research, while other indicators remained at levels comparable to 2021.

Figure 1. Financial health indicators

Percentage point change in positive responses for each financial health indicator (2021-22).

Overview

The State of Financial Health in 2022

In the fifth year of measuring financial health in the U.S., the percentage of people considered Financially Healthy declined for the first time, from 34% in 2021 to 31% in 2022. The percentage of people considered Financially Coping increased from 52% to 55%, while the percentage of Financially Vulnerable people did not change significantly in the past year.9 These changes bring the financial health of people in the United States back in line with pre-pandemic levels; the percentages of Financially Healthy and Coping people in 2022 are not significantly different from what they were in 2019, though the percentage of people considered Financially Vulnerable remains significantly lower (Figure 4).

Figure 2. Financial health declined for the first time since 2018.

Percentage of people categorized by financial health tier (2018-22).

These findings align with other research, which show reductions in financial health and diminishing consumer sentiment over the past year. In June 2022, respondents to the Index of Consumer Sentiment reported the lowest assessment of their financial situation since 2013, with many citing inflation as a contributing factor.10 Gallup research found that 46% of consumers viewed their financial situation as either excellent or good, down from 57% in 2021.11 The Morning Consult Well-Being Scale also found that traditionally secure groups, such as people with higher incomes, have felt the effects of the current economic conditions: Individuals with incomes of $100,000 or more had the largest drop in financial well-being in the past year.12 At the same time, inflation has also eroded the wage increases experienced by people earning low incomes last year.13

Figure 3. Less than one-third of adults in the United States are Financially Healthy.

Estimated share of adults in the U.S. by financial health tier (2022).

Note: Financial health tiers are calculated using the FinHealth Score. See the Methodology section in the PDF version of this report for more on the measurement methodology. Population counts are derived from the 2022 April Current Population Survey using population estimates for U.S. noninstitutionalized adults ages 18 and older.

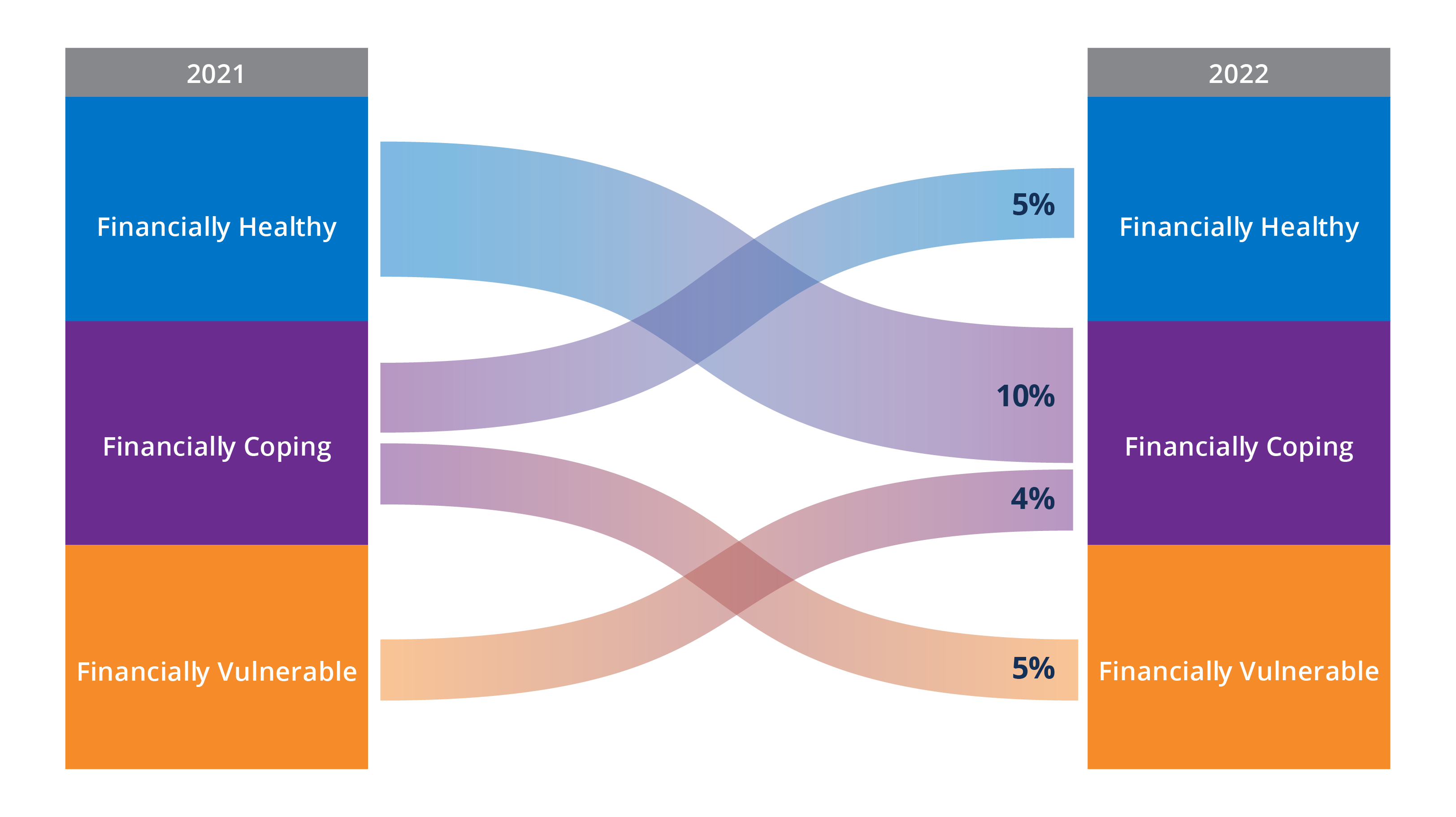

In the longitudinal sample of respondents who took Financial Health Pulse surveys both in 2021 and 2022, a larger percentage of people experienced declines in their financial health than experienced improvements. In that sample, 15% of people moved down a financial health tier and 9% of people moved up a tier in the past year. The largest change was between the Financially Healthy and Financially Coping tiers: 10% of sample respondents dropped from Healthy to Coping, while only 5% of the sample climbed from Coping to Healthy.

Figure 4. A greater percentage of people experienced financial health declines than improvements.

Percentages of people with changes in financial health tier (2021-2022).

Demographics & Socioeconomics

Financial Health Declines Affected Nearly All Groups

Financial health disparities across household income, race and ethnicity, gender, LGBTQIA+ status, and ability persisted in 2022, with groups that historically have been advantaged reporting far greater levels of financial health than underserved groups. However, some historically advantaged groups, which also typically report high levels of financial health, experienced notable drops in financial health in the past year. People with household incomes over $60,000, White people, men, people who do not identify as LGBTQIA+, and people without disabilities experienced significant declines in their financial health, mirroring the national trend (Table 2). Meanwhile, Black people and women also experienced declines in their financial health.

Declines for some of these groups may be a reflection of their already greater financial health: Unlike factors such as inflation, which likely affected virtually all socioeconomic and demographic groups, historically advantaged groups were in a position to more acutely experience reductions in long-term savings. As such, those who owned investment accounts were directly exposed to the volatility in financial markets, which may have reduced their savings. Historically marginalized groups, on the other hand, may have never had savings large enough to incur comparable declines.

Household Income

The large gaps in financial health across household income levels persisted in 2022.

This year, fewer people with less than $30,000 in household income continued to be considered Financially Healthy than their counterparts with higher incomes. Over the past year, the percentage of people with household incomes between $60,000 and $99,999 who are Financially Healthy declined by 7 points, from 43% to 36%, while the percentage of people with household incomes of $100,000 or more who are Financially Healthy fell from 59% to 54% in the past year. Meanwhile, there were no significant changes in the percentage of people with household incomes below $60,000 who are considered Financially Healthy. A greater percentage of people at all income levels reported spending more than their income in 2022 (Table B2).

People with household incomes below $60,000 still felt the impact of inflation on their finances, though there was not a statistically significant change in their distribution across financial health tiers. People with household incomes less than $30,000 more frequently reported some level of stress due to inflation than people with higher household incomes (Table B3). The percentage of people with household incomes less than $30,000 reporting sufficient short-term savings also significantly declined (Table B2).

There was a significant decrease in the percentage of people with household incomes of at least $60,000 who were confident they were on track to meet their long-term financial goals. Since people with $60,000 or more in household income are more likely to own long-term financial assets and are therefore more invested in equity markets, the market decline of 2022 likely had a more profound impact on their financial health than people with less than $60,000 in household income.27

Race and Ethnicity

The percentage of Black people who are considered Financially Healthy decreased by 6 points, from 21% to 15%, in the past year. This decrease eroded most of the financial health gains Black people had previously experienced between 2020 and 2021.

Increases in spending relative to income contributed to the decline, as the percentage of Black people spending less than or equal to their incomes declined by 7 points in the past year (Table B5).

The likely culprit of this change is inflation, which tends to be higher and more volatile for Black households. Research from the Federal Reserve Bank of Richmond shows that Black households allocate a greater proportion of their expenditures to essential goods, which also have volatile prices that are impacted by inflation, than White households. The difference in consumer baskets accounts for two-thirds of the difference in inflation experiences for Black and White households.28 Results from the Pulse survey also show that Black people more frequently used their savings to pay for goods, shopped at discount retailers, and carried credit card balances to cope with inflation than White people (Table B4).

White people were 4 percentage points less likely to be Financially Healthy in 2022 than the prior year, with a multitude of factors contributing to the decline. Compared with 2021 figures, a smaller percentage of White people reported spending less than or equal to their incomes, having sufficient short-term savings, having confidence in meeting their long-term financial goals, having manageable or no debt, and having confidence in their insurance coverage (Table B5). Because White people are more likely to own long-term financial assets such as retirement accounts, they are more exposed to volatility in financial markets than Black or Latinx individuals, who are less likely to own these assets.29 Market fluctuations might explain why White people experienced declines not just in the short-term aspects of their financial health, such as spending and saving, but also in long-term aspects, such as borrowing and planning. There was no significant change in the percentage of people considered Financially Healthy among Latinx people, people who indicated they were of multiple races or ethnicities, or people who selected other response options.

Despite these shifts, enduring disparities remain. A much greater percentage of White and Asian people were still Financially Healthy relative to people of other races or ethnicities. Conversely, Black and Latinx people tend to be Financially Healthy at much lower rates, reflecting historical disinvestment and segregation, structural barriers to financial health, and the continuing reality of discrimination.30, 31, 32, 33 Consequently, financial health in America and race remain deeply intertwined.

Gender

The gender gap in financial health, which expanded between 2020 and 2021, persisted in 2022, as a lower percentage of women were Financially Healthy than men. However, both men and women experienced declines in financial health over the past year. The percentage of men who are Financially Healthy declined from 43% to 39%, while the percentage of women who are Financially Healthy decreased from 26% to 23%. Declines across the eight indicators were similar between men and women in the past year: The percentage of men and women who spent less than or equal to their incomes, had sufficient short-term savings, and had confidence that they were on track to meet their long-term financial goals declined between 2021 and 2022 (Table B6).

Recent research from the Financial Health Network examined the gender gap in financial health. Women face financial disadvantages in every facet of their finances, and they are more likely than men to report that their financial situation is worse now than prior to the pandemic. Compared with men, working-age women:

- Have lower household incomes on average.

- Are more likely to be subjected to workplace harassment and discrimination.

- Report making career changes due to parenting responsibilities at higher rates.

- Are more likely to say their current level of debt is unmanageable.

- Are less likely to report having a retirement savings vehicle in their own name.

Closing the wage gap, building a better care infrastructure, making retirement security more accessible, and making higher education more affordable are top priorities for closing the gender gap in financial health.

LGBTQIA+ Status

![]()

The financial health gap between LGBTQIA+ and non-LGTBQIA+ people continued in 2022. 23% of people who identify as LGBTQIA+ were considered Financially Healthy versus 32% of people who do not identify as such, likely a reflection of discrimination they face when accessing resources that are critical for their well-being, such as housing and medical care.34 The percentage of Financially Healthy people among those who do not identify as LGBTQIA+ declined by 4 points, as spending increased relative to income and these individuals reported declines in savings (Table B7). Meanwhile, the financial health of people who identify as LGBTQIA+ did not change significantly in the past year.

Ability

People without disabilities experienced declines in financial health, but remained more likely to be Financially Healthy than people with disabilities. In 2022, 20% of people with disabilities were considered Financially Healthy, as opposed to 35% of people who do not have disabilities. The percentage of people without disabilities who are considered Financially Healthy decreased by 4 points; changes in their financial health indicators largely mirrored national trends (Table B8), while the financial health of people with disabilities did not change significantly. In 2023, with support from Principal Foundation, the Financial Health Network will conduct in-depth research into the financial health of people with disabilities and the financial challenges they face.

These findings suggest that groups with high levels of financial health – White people, men, those with $60,000 or more in household income, individuals identifying as non-LGBTQIA+, and people without disabilities – experienced significant declines in their financial health over the past year, along with Black people and women. These declines appear to be related to increases in spending, which was likely caused by higher inflation. Declines in long-term savings also contributed to these declines, as groups who are more likely to own long-term financial assets – people with at least $60,00 in household income and White people – felt the financial health repercussions of the downward trend in equity markets. However, these people will still be in a position to improve financially when financial markets recover, while those who do not own these assets may struggle to keep pace.

A Boost From Better Jobs

The tightening labor market appears to have been particularly important to the financial health of workers with household incomes less than $30,000 a year.

People with household incomes in this range who received wage increases in the same job, increased the hours they worked, or voluntarily got a new job saw large improvements in their FinHealth Scores relative to workers in the same income bracket who did not experience these events. Those in the same income group who received a raise or increased hours at their jobs experienced an eight-point increase in their FinHealth Score relative to those who did not, and those who switched jobs voluntarily experienced a nine point increase (Figure 5).

There was no statistically significant association between these events and FinHealth Score changes for higher-income groups, possibly because modest increases in income are less likely to have a dramatic effect on the ability of those with higher incomes to meet their spending needs. Considering that people with household incomes of less than $30,000 had an average FinHealth Score of about 54 points in 2021, an eight-point change represents a substantial shift in financial circumstances for this group (roughly a 15% score increase at the mean).

Figure 5. People with household incomes less than $30,000 who experienced a positive employment event increased their FinHealth Scores.

Despite these findings, people with household incomes less than $30,000 did not experience significant increases in financial health on average between 2021 and 2022. This may be in part because positive employment changes were relatively rare for this group. People at this income level were far less likely to be employed than those in higher-income households, and even those who were employed received raises less frequently (Tables B9 and B10).36

Painful Price Increases

Inflation likely affected the finances of every person in the U.S. to some degree, but respondents’ subjective assessments of inflation’s toll varied widely.

![]()

The most common categories for which people reported price changes impacting their standard of living were food (38%); transportation, including gasoline (38%); and utilities (30%).37 People were less likely to report impact in healthcare (18%), housing (16%), education (6%), and child care (5%). In most spending categories, a greater percentage of people with household incomes less than $30,000 reported a standard of living impact from inflation than people from households with incomes of $100,000 or more (Table 3).

Table 3. People with low incomes reported inflation impacts more frequently.

Percentage of people reporting at least a moderate impact on standard of living in each spending category, by 2021 household income.

| Overall | Less than $30,000 | $30,000 to $59,999 | $60,000 to $99,999 | $100,000 or more | |

|---|---|---|---|---|---|

| Food | 38% | 45% | 44% | 35%* | 27%* |

| Transportation | 38% | 40% | 44% | 38% | 28%* |

| Utilities | 30% | 38% | 35% | 26%* | 20%* |

| Healthcare | 18% | 18% | 21%* | 17% | 15%* |

| Housing | 16% | 22% | 19% | 10%* | 11%* |

| Education | 6% | 8% | 5%* | 4%* | 6% |

| Child care | 5% | 5% | 4% | 5% | 4% |

* Statistically significant vs. those with household incomes less than $30,000.

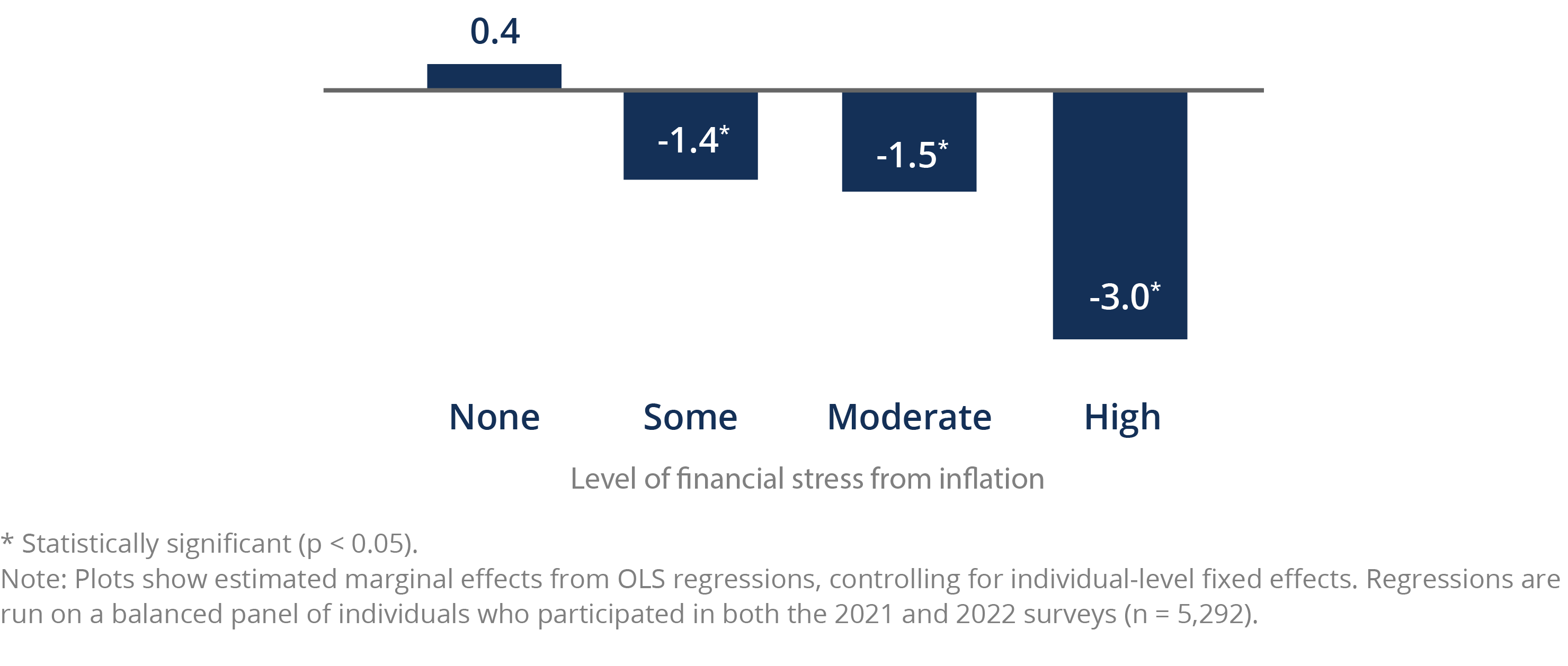

The degree of financial stress that respondents attributed to recent price increases varied widely: 29% of people reported feeling moderate or high financial stress from inflation, while 37% reported feeling no stress at all (Table B11). There was also a relationship between the level of stress reported and changes in financial health (Figure 6). Those who reported a high level of stress experienced an average decrease of three points between 2021 and 2022, about three times the mean FinHealth Score decrease in the population overall. Those who reported no stress or said they did not notice price changes did not experience a statistically significant score change. Respondents reporting “moderate” or “some” stress experienced decreases of about 1.5 points, closer to the average score change for the entire sample.38

Figure 6. Level of stress from inflation is associated with change in FinHealth Score.

Estimated FinHealth Score change relative to the prior survey year, by level of inflation-induced financial stress.

Waning government assistance may also explain some individuals’ notable decreases in financial health from 2021 to 2022. For example, the 2021 Pulse survey was fielded soon after the final round of relief payments from the federal government, which temporarily boosted checking and savings balances.39 Likewise, advance Child Tax Credit payments ended in December 2021 and several aspects of expanded federal unemployment assistance expired in September 2021.40, 41 The expiration of these programs likely affected the financial health of the families receiving them relative to those who were not. Unfortunately, the timing and frequency of the Pulse survey do not allow us to reliably estimate the effects of their expiration.

These findings illustrate that two major macroeconomic trends – inflation and a tightening labor market – were not experienced uniformly in the U.S., and that financial health changes over the past year were associated with those experiences. The ability to capitalize on tight labor market conditions was an important indicator of financial health mobility for people in households with incomes under $30,000, but these same people were also much less likely to be in a position to benefit from those conditions. Low-income households also bore the brunt of inflation’s impact, and those who reported more stress from inflation experienced worse financial health outcomes.42 However, these correlations are not so strong that people with low incomes experienced larger average score decreases overall. For people with low incomes and very low FinHealth Scores already, adverse effects from inflation may not be detectable in their scores.

The Financial Health Network is collaborating with the University of Southern California’s Dornsife Center for Economic and Social Research to field the survey to its online panel, the Understanding America Study. Study participants who agree to share their transactional and account data use Plaid’s data connectivity services to authorize their data for analysis.