The Gender Gap in Financial Health

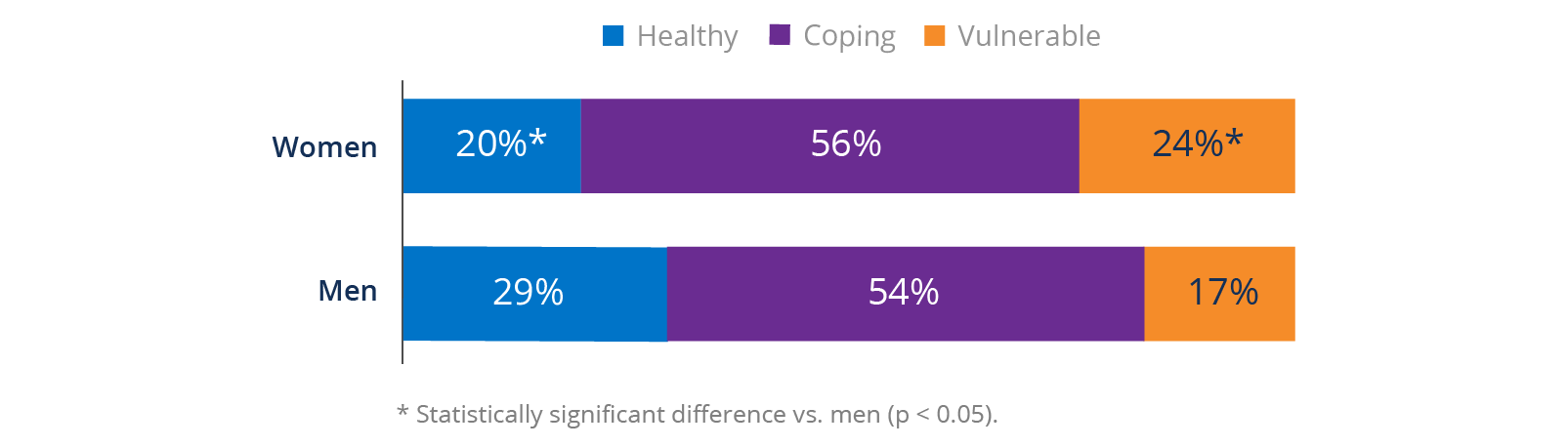

The data by gender is stark: Women are far less likely to be Financially Healthy than men. Only one in five working-age women (20%) are considered to be Financially Healthy, versus 29% of working-age men. Furthermore, nearly one-fourth of women ages 18-64 (24%) are classified as Financially Vulnerable, compared with 17% of men in the same age bracket.

Figure 1: Men are nearly 1.5 times more likely to be considered Financially Healthy than women.

Financial health distribution by gender.

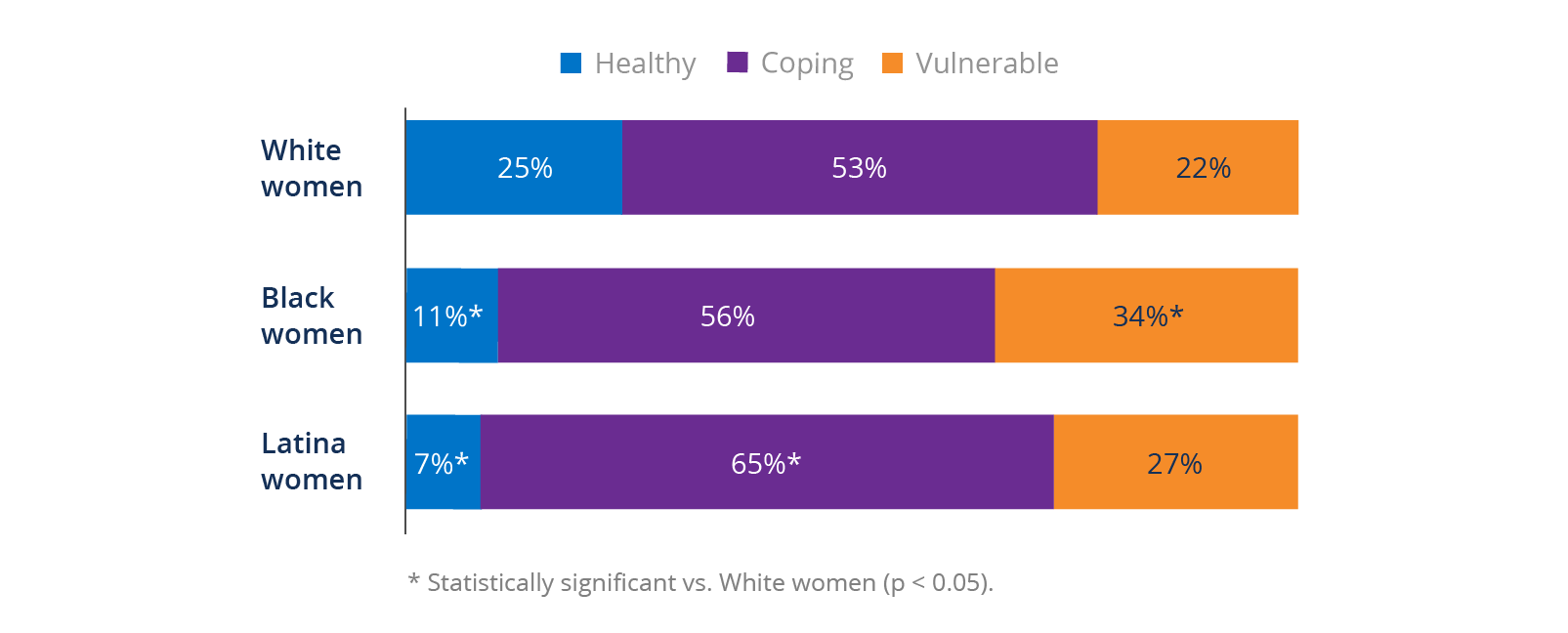

By Race and Ethnicity

Our data show a chasm among women by race and ethnicity: Only 11% of Black women and 7% of Latina women are considered Financially Healthy, versus 25% of White women.17

Figure 2: White women are far more likely to be considered Financially Healthy.

Financial health by race and ethnicity.

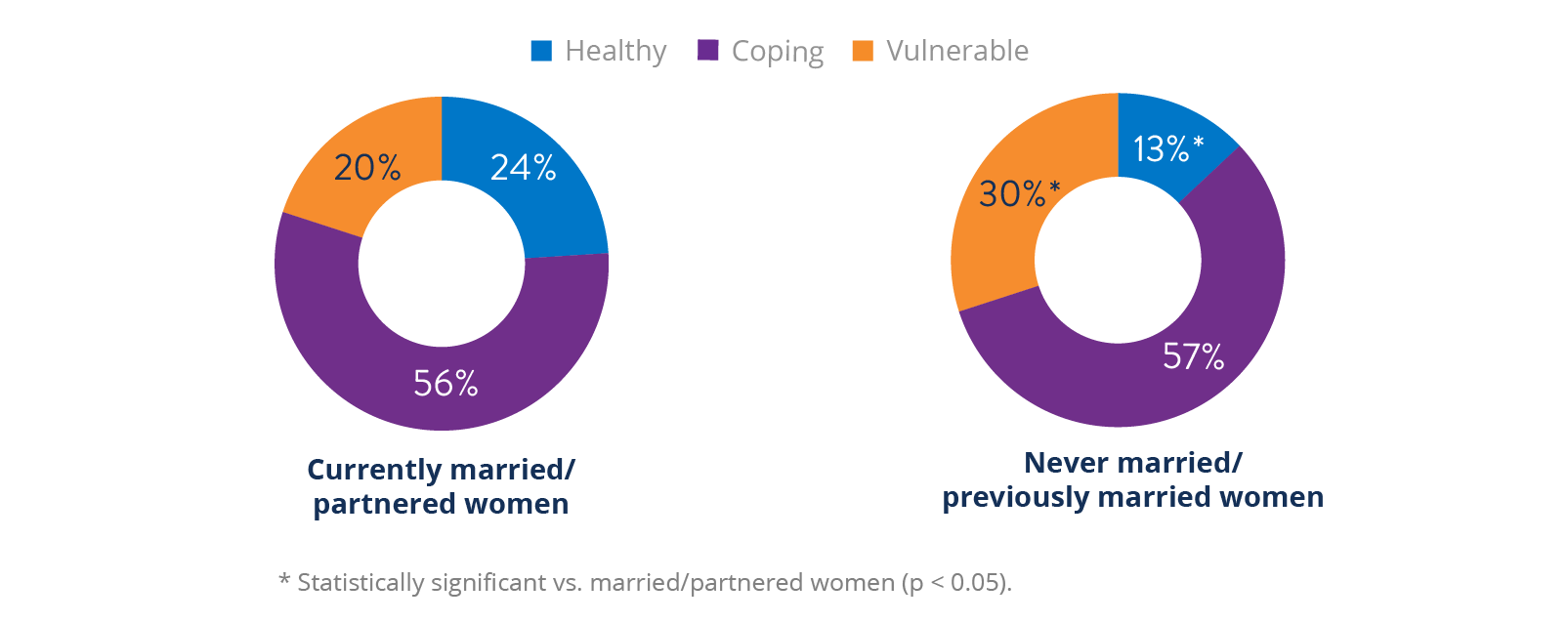

By Marital Status

Figure 3: Women who are married or in partnerships are more likely to be Financially Healthy than those who are not.

Financial health by marital status.

Parenting

Among women, those without children under 18 are far more likely to be Financially Healthy than those with children (25% versus 13%). Even after controlling for marital status, race, age, and household income, women who have children are still 5 percentage points less likely to be considered Financially Healthy than women who do not.

Fatherhood is also associated with lower financial health, but due to a confluence of factors including income, fathers are still more likely to be Financially Healthy than mothers (20% versus 13%). Women remain far more likely to take primary responsibility for child care – regardless of employment status – and are far more likely to take time away from work or adjust their hours or careers. The Institute for Women’s Policy Research has found that 43% of working women will experience at least one year without any earnings, nearly twice the rate of men.31 Furthermore, nearly 80% of single-parent households are headed by mothers.32

In our study, 70% of mothers with children under 18 reported reducing their hours, taking on additional hours, quitting a job, taking a leave of absence, or switching to a less demanding job at some point because of their parenting responsibilities. By contrast, the same is true for only 55% of men with children. (See Table 3.) In particular, mothers are more than twice as likely to report quitting a job, twice as likely to take an unpaid leave of absence, and 1.5 times as likely to report having reduced their hours than fathers.

Table 3: 70% of mothers report making a career change as a result of becoming a parent.

Responses to the question, “Have you ever done any of the following as a result of becoming a parent?”

| Responses | Women | Men |

|---|---|---|

| Quit a job | 32%* | 15% |

| Reduced my hours | 30%* | 20% |

| Took a paid leave of absence for maternity leave or other parental leave | 28% | 22% |

| Took an unpaid leave of absence from my employer | 20%* | 10% |

| Switched to a less demanding job | 19% | 18% |

| Took on additional hours to pay for the cost of child care | 12% | 17% |

| Took a paid leave of absence from my employer for some other reason | 8% | 6% |

| Other | 2% | 2% |

| Any of the above | 70%* | 55% |

* Statistically significant vs. men (p < 0.05).

This question was asked to those who reported that they are a parent or guardian to a child under the age of 18. (For women, n = 820; for men, n = 336.)

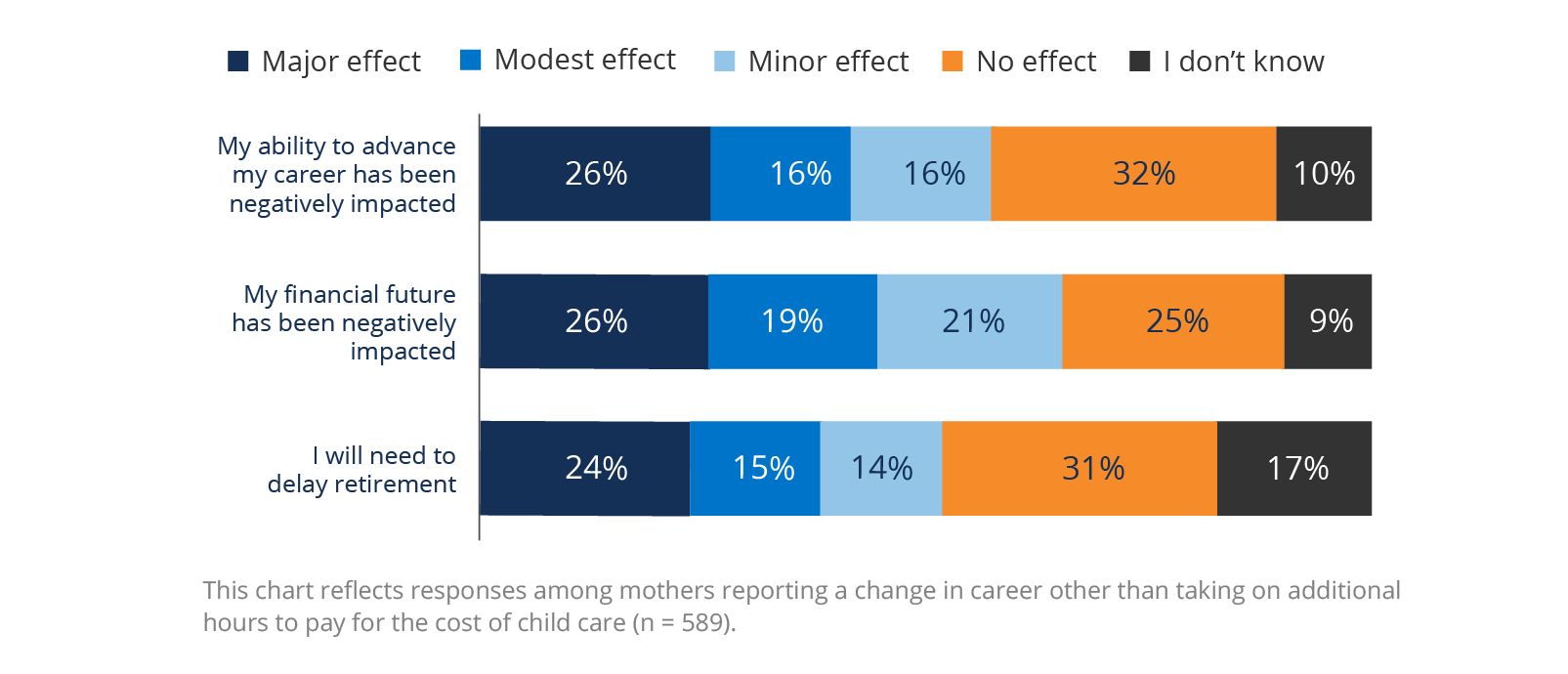

Whether permanent or temporary, many of these job shifts can have longer-term implications for financial health. Of mothers who had made a change in work status other than increasing their hours, 41% said it had at least a modest negative impact on their career advancement, 45% said their financial future had been negatively impacted, and 38% said they would need to delay retirement.33 (See Figure 4.)

Figure 4: Many mothers who have taken leave or adjusted their careers report financial impacts.

Responses to the question, “Please indicate whether this change/these changes affected you in any of the following ways.”

Stories from Everyday Women

To better understand the issues we uncovered throughout our research, we spoke with women across the country about their financial lives. This is what they told us.

Policy Needs

1. Closing the wage gap and assuring living wages

Our existing laws are not fully protecting women from unequal pay or discrimination, and too many women, particularly women of color, do not earn a livable wage, despite full-time labor.

Many organizations have worked tirelessly to bring attention to this issue. The following groups are just a few of those that have outlined policies to address gender inequities in pay:

- Equal Rights Advocates

- Institute for Women’s Policy Research

- National Domestic Workers Alliance

- National Partnership for Women and Families

- National Women’s Law Center

2. Building a care infrastructure

Perhaps more than any other moment in time, the COVID-19 pandemic has revealed the critical need for a more robust care infrastructure, including more affordable child care and elder care, paid leave, and fair pay for care workers.62 Care Can’t Wait, a consortium of more than a dozen leading organizations, has aligned on care as a critical element of our economy and an essential component for continued pandemic recovery and economic growth.

3. Expanding retirement plan availability and portability

Numerous states are introducing programs to make workplace retirement plans available to workers who don’t currently have access.63, 64 Such programs could provide a vehicle for long-term saving to those who are currently excluded. The Center for Retirement Research tracks uptake of such programs at the state and federal level.

4. Rethinking Social Security

Social Security benefits are based on a person’s 35 highest earning years; women receive Social Security benefits that are, on average, 80 percent of those men receive, with mothers receiving even less.65 Some researchers have called for adjustments to Social Security policy, such as adjusting the spousal benefit or providing a caregiver credit.66 The National Institute for Retirement Security has outlined additional policy recommendations to strengthen women’s financial security in retirement. 67

5. Fostering affordable higher education

The current trajectory of higher education costs is unsustainable and disproportionately burdens women, especially women of color. Advocates including the Student Borrower Protection Center and AAUW have been exploring a range of solutions that would ease burdens on existing borrowers and enable more students to pursue affordable education.

Employer Needs

1. Creating supportive workplaces

Flexible work schedules, salary transparency, and restrictions on requesting salary histories in interviews have all been cited as playing an important role in narrowing the income gap.68, 69 TIME’S UP and ideas42 have compiled a guide to using behavioral practices to promote pay equity.70

Beyond these specific measures, the Financial Health Network has developed an Employer FinHealth Toolkit to support HR professionals in advancing employee financial health more broadly. We are also working with JUST Capital, Good Jobs Institute, and PayPal to make employee financial well-being a C-suite and investor priority.71

2. Expanding benefits

Expansion of availability of benefits to part-time workers could also close the gap in individual retirement plan ownership for women, while expansion of affordable health care options could help women avoid medical debt.72 In consultation with leading providers, the Financial Health Network has detailed a series of actions that employers can take to help employees avoid medical debt.73 WISER (the Women’s Institute for a Secure Economic Retirement) provides tools and resources for women across a range of issues.74

3. Supporting financially struggling employees

For individuals who are grappling with debt or who need to build credit, employers can play an important role via financial coaching or debt management services, programs like emergency savings or emergency grants, or contributions toward student loan repayments.75, 76

4. Ending harassment and supporting survivors

Employers clearly have an essential role to play in creating safe workplaces, including assessing for risk factors associated with harassment, enacting comprehensive anti-harassment policies, and holding employees who commit harm accountable.

Ensuring paid leave, including paid survivor leave, can be an important step to support employees who are subjected to harassment. FreeFrom, a national organization that advocates for survivors of intimate partner violence, has designed a template for a paid survivor leave policy

5. Leveraging behavioral lessons

Employers can apply behavioral insights to the design of their financial benefits, such as auto-enrollment in retirement plans and auto-escalation. The Employer Toolkit’s “Designing for Engagement” section section identifies opportunities for employers to simplify benefits as well as motivate and support employees to make the most of their benefits.

Of course, there is no one “silver bullet” policy or product that would address the financial health gap. Improving the financial health of women requires a systematic and collaborative effort from many stakeholders, but there is no doubt that addressing the gap would benefit us all.

Acknowledgments

This report benefited from the review of numerous experts on women’s economic security, including:

- Melany De La Cruz-Viesca, UCLA Asian American Studies Center;

- Kirkley Doyle, FreeFrom;

- Julie Kashen, The Century Foundation;

- Ana H. Kent, Federal Reserve Bank of St. Louis;

- Heather McCulloch, Aspen Institute and Asset Building Strategies;

- Kate Ryan and Olivia Storz, Institute for Women’s Policy Research.

We also thank numerous other experts who provided invaluable guidance on our research design, including representatives from the Diaper Bank of North Carolina and the National Diaper Bank Network, Futures Without Violence, the Institute for Women’s Policy Research, the National Partnership for Women and Families, the Women’s Institute for a Secure Retirement, and the Urban Institute.

We are grateful for the guidance and support of Jo Christine Miles at the Principal Foundation.

Rob Levy and David Silberman provided essential input into this research initiative, as did Helen Robb and Stephen Arves. We also thank our Financial Health Network colleagues who provided feedback on this draft: Uzma Amin, Beth Brockland, Andrew Dunn, Thea Garon, and Tanya Ladha. Naomi Adams Bata, Fawziah Bajwa, Dan Miller, and Jacquelyn Reineke were also critical in communicating the findings.

SSRS served as our research partner for this initiative. We thank Jordon Peugh, Jania Marshall, Kristen Conrad, Shannon Sesa, and colleagues for their close collaboration on quantitative and qualitative research design and data analysis.

Funding for this research was made possible by the Principal Foundation. The findings, interpretations, and conclusions expressed in this piece are those of the Financial Health Network and do not necessarily represent those of our funders or partners.

![]()

This report is part of the Financial Health Pulse research series. The Financial Health Pulse provides regular updates and actionable insights about financial health in America. The Financial Health Pulse is supported by the Citi Foundation, with additional funding from Principal Foundation.