Financial Health of Workers in Low-wage Jobs

By Beth Brockland, Tanya Ladha

-

Category:

-

Tags:

Why and How to Invest in the Financial Health of Workers in Low-wage Jobs

The focus on low-wage work and its impact on the well-being of workers across the U.S. is growing. However, relatively little is known about the financial well-being of workers in low-wage jobs. This study seeks to fill this gap by shedding light on the financial health of people in low-wage jobs and the impact of employment-related factors, such as benefits, on their financial health.

Our findings suggest that investing in the financial health of workers in low-wage jobs – defined as earning up to $17 per hour in hourly wages or up to $35,360 per year in annual wages – can be an effective strategy for employers to ensure a stable and productive workforce.

Key Findings

How Employers Can Improve Worker Financial Health

Our findings suggest numerous actions that employers should take to improve the financial health of their workforce, particularly those who are in low-wage jobs:

- Increase workers’ wages.

- Provide high-quality and affordable insurance coverage.

- Promote retirement savings.

- Offer emergency savings opportunities.

- Provide support for childcare and other caregiving needs.

- Offer stable and predictable scheduling.

In addition to considering these recommendations, it is also important for employers to understand where there are gaps in financial health among segments of the workforce and to advance equity by closing those gaps. To provide help for this journey, this report also directs employers to our Employer FinHealth Toolkit and our recent brief on increasing workforce equity through employee financial health programs. By understanding and addressing worker financial needs, employers can play a powerful role in improving financial resilience for their workers, their businesses, and our economy as a whole.

Examining How Low-wage Work Shapes Worker Well-being

The focus on low-wage work and its impact on the well-being of workers across the U.S. is growing. The pandemic laid bare the essential nature of many low-wage jobs, and as the economy recovers, workers are demanding that these jobs support economic security and well-being for themselves and their families. With the onset of the Great Resignation, employers are more focused than ever on recruiting and retaining talented workers. For many, that includes making investments in wages and benefits that enhance workers’ financial health.

While there is significant research about low-wage work and its relationship to economic mobility over time, relatively little is known about the financial well-being of workers in low-wage jobs in the present. This study seeks to fill this gap by shedding new light on the financial health of people who work in low-wage jobs and the impact of employment-related factors, such as benefits, on their well-being. Our findings suggest investing in the financial health of this segment of workers can be an effective strategy for employers to ensure a stable and productive workforce. To that end, we also offer recommendations of numerous actions that employers can take to improve the financial health of workers in low-wage jobs.

Methodology

The Financial Health Network conducted a survey of people who work in low-wage jobs. The survey was administered in December 2021 by SSRS, a full-service survey and market research firm. For the purposes of this survey, we defined workers in low-wage jobs as people earning up to $17 per hour in hourly wages, or up to $35,360 per year in annual wages (the equivalent of full-time work for 52 weeks at $17 per hour) from their main job. This threshold is based on the Brookings Institution’s research, which used Census Bureau data to set a low-wage threshold of $16.03 at the national level in 2019.1 We updated Brookings’ threshold to reflect the latest Census data at the time of this study.

The survey sample includes 1,738 respondents ages 18-64, with oversamples for Black and Latinx respondents. We chose to focus on Black and Latinx workers in particular because they are overrepresented in low-wage jobs relative to their share of the overall workforce, and because of the legacy of historic racism and discrimination and ongoing structural barriers to financial health that these communities face. For more on how we calculated the race and ethnicity variable in this survey, please see Appendix II.

The majority of workers in our sample (84%) report working only one job, suggesting that most of these workers rely on traditional employment and not other forms of employment, such as temporary or gig work, for their main source of income. For more on the demographic and employment characteristics of our sample, please see Appendix I.

The sample was drawn from two nationally representative address-based samples, the SSRS Opinion Panel and Ipsos’ KnowledgePanel. Data were weighted using the 2021 Current Population Survey and the 2019 American Community Survey to represent the U.S. adult population ages 18-64 who earn no more than $17 per hour or $35,360 per year. 2 The margin of error for the total sample is +/- 3.3 percentage points at a 95% confidence interval.

While the survey was in the field, the Financial Health Network conducted a small number of qualitative interviews with individuals working low-wage jobs. This report includes several direct quotes from these interviews.

Technical Notes

Percentages throughout this report have been rounded. All comparisons cited in this report are statistically significant at p < 0.05, unless otherwise noted.

This report focused on workers in low-wage jobs. Often, we refer to this group simply as “workers” to simplify the writing and ease the burden on the reader. Unless otherwise noted, “workers” refers to workers in low-wage jobs as defined by the sampling criteria described above.

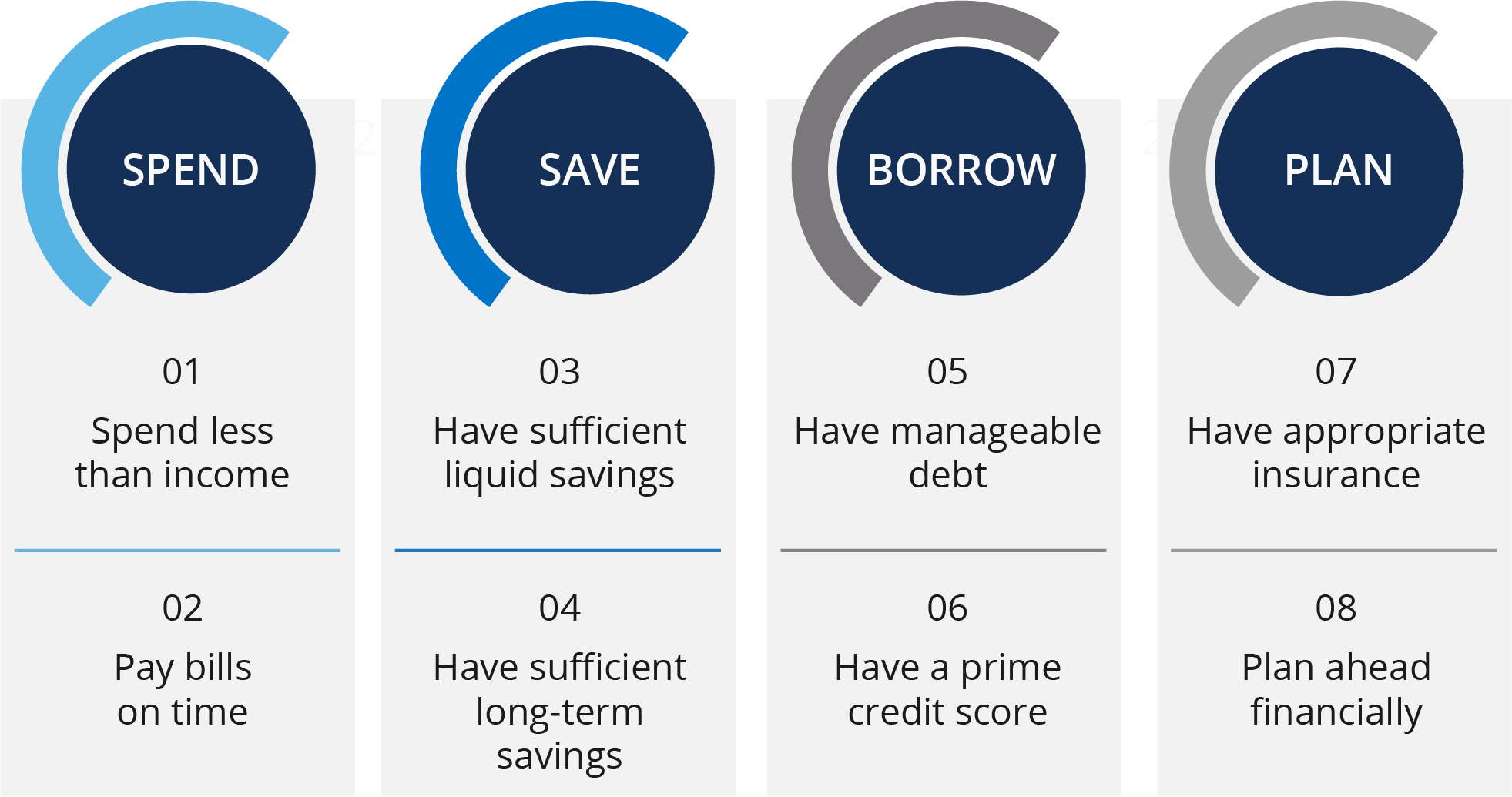

Defining Financial Health

Financial health is a composite framework that considers the totality of people’s financial lives: whether they are spending, saving, borrowing, and planning in ways that will enable them to be resilient and pursue opportunities. Financial health provides researchers with a useful lens through which to explore the financial lives of people in America because it pulls together the multiple strands of an individual’s financial life into a coherent whole.

Calculating FinHealth Scores® and Tiers

The FinHealth Score is a metric based on survey questions that align with the eight indicators of financial health. For every individual who responds to all eight survey questions, we can calculate one aggregate FinHealth Score and four subscores for Spend, Save, Borrow, and Plan. FinHealth Scores range from 0-100 and can be used to categorize respondents into three financial health tiers: Financially Healthy, Financially Coping, or Financially Vulnerable.

People who are considered Financially Healthy are spending, saving, borrowing, and planning in a way that will allow them to be resilient and pursue opportunities over time. People who are considered Financially Coping are struggling with some, but not necessarily all, aspects of their financial lives, as measured by our eight indicators of financial health. People who are Financially Vulnerable are struggling with all, or nearly all, aspects of their financial lives, as measured by our indicators. Visit the FinHealth Score methodology page for more information.

Fewer than 1 in 7 workers in low-wage jobs is Financially Healthy.

An estimated 53 million people in America between the ages of 18 and 64 – or 44% of all workers – work in low-wage jobs. These include many of the jobs considered “essential” during the COVID-19 pandemic, particularly in the retail and healthcare sectors. Race, ethnicity, and gender play an important role, with Black workers, Latinx workers, and women each overrepresented among the low-wage workforce compared with their share of the overall worker population.3

Numerous complex factors limit these workers’ economic mobility, including occupational segregation (which occurs when a demographic group is overrepresented or underrepresented in certain types of jobs), racial and gender discrimination, unequal educational opportunities, and caregiving responsibilities.4,5,6,7 For many, low-wage work itself makes it difficult to advance, with conditions like low pay and erratic scheduling preventing workers from investing time in searching for better jobs, learning new skills, or gaining credentials.8

These same conditions can also make it challenging for workers in low-wage jobs to build and maintain their financial health. In addition to the obvious impact of low wages on workers’ ability to pay bills and save for the future, there is robust research demonstrating a link between variable and unpredictable scheduling – which are prevalent in low-wage jobs – and poorer health and financial outcomes for workers and their families.9

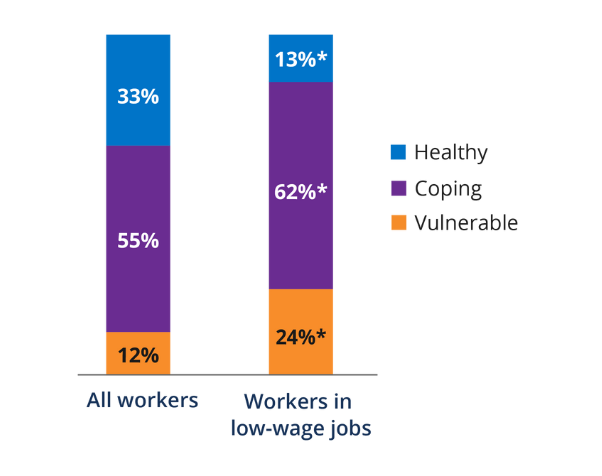

We find that only 13% of workers, or fewer than 1 in 7, are considered Financially Healthy. Financial health is defined as having the ability to spend, save, borrow, and plan in ways that allow people to be resilient and pursue opportunities. Nearly one-fourth of workers in low-wage jobs (24%) are Financially Vulnerable, which means that they are struggling with all, or nearly all, aspects of their financial lives, as measured by our eight indicators of financial health.10

Figure 2: Workers in low-wage jobs are less Financially Healthy than the average worker.

* Statistically significant compared with all workers.

* Statistically significant compared with all workers.

Data for “All workers” comes from the Financial Health Pulse™ survey conducted in April and May of 2021 and represents only employed adults ages 18-64. Percentages are based on the 1,569 respondents who answered all eight financial health indicator questions.

These findings are even more striking given that nearly three-fourths of workers in low-wage jobs (72%) are primary earners for their households.11 These workers rely on their low wages to support their families, and as later sections of this report demonstrate, they often lack access to supportive workplace benefits that can help them manage their financial lives in the present and plan for the future.

(For more about the demographic characteristics of our sample, see Appendix I.)

Figure 3: Nearly three-fourths of workers in

low-wage jobs are primary earners.

“[I] make so little, it’s hard to make ends meet… [If I] miss one day, I won’t be able to pay my bills.”

–Home Healthcare Worker

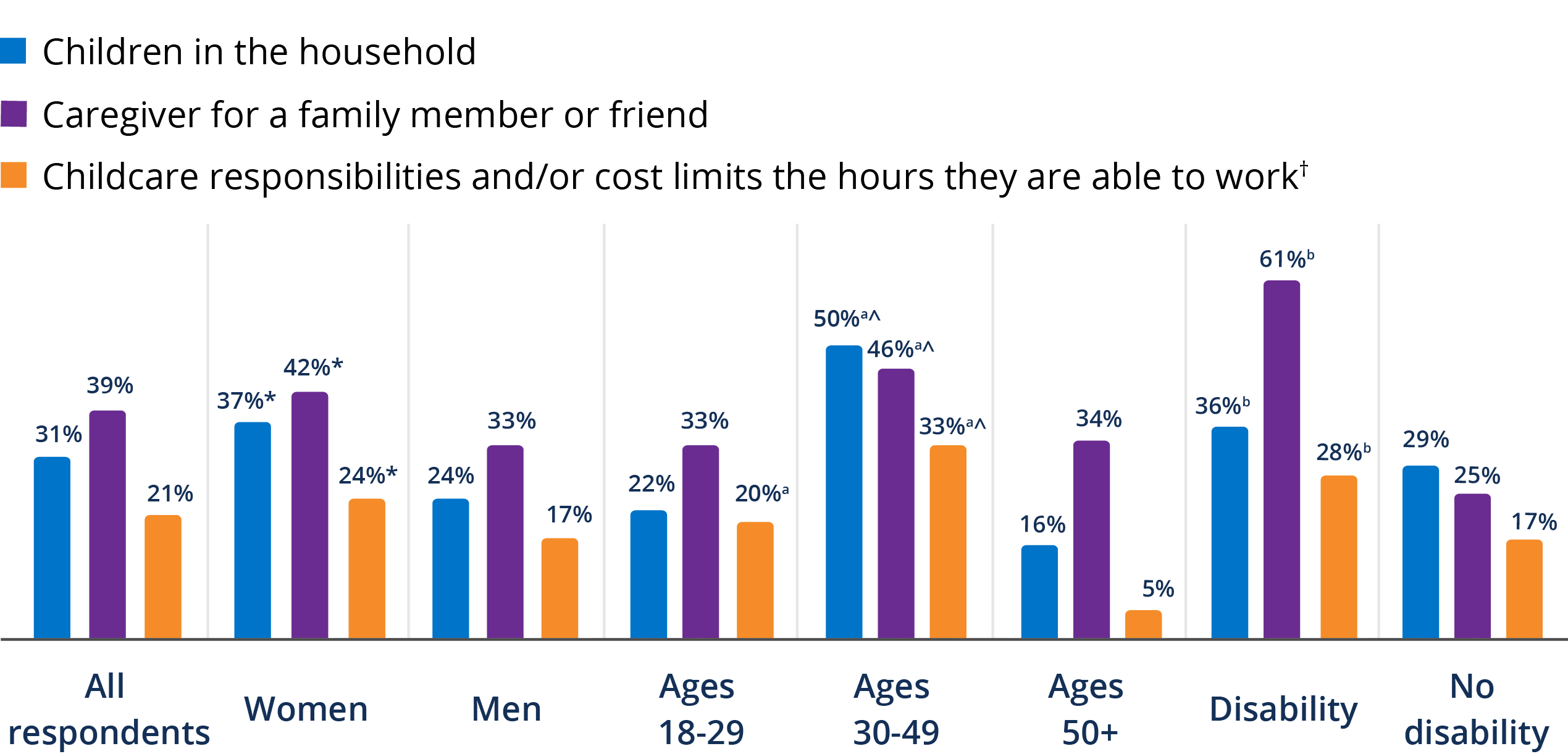

A closer look at the data by financial health tier reveals a more detailed profile of workers in low-wage jobs. We find that workers in low-wage jobs who are Financially Vulnerable are more likely than those who are Coping or Healthy to be women, to be between 30 and 49 years old, to have someone in their household with a disability, or to be parents or caregivers.12 These characteristics are often overlapping and mutually reinforcing, contributing to lower financial health for those who fall into more than one of these groups. For example, women, workers ages 30-49, and those who have someone in their household with a disability are more likely than others to have caregiving responsibilities and to report that those responsibilities limit how much they can work.

Somewhat surprisingly, our survey did not find a strong relationship between race and ethnicity and financial health for workers in low-wage jobs.13 While workers of color – particularly Black and Latinx workers – are overrepresented in low-wage jobs relative to their share of the overall workforce, we find that among low-wage workers, financial health outcomes are remarkably similar regardless of race or ethnicity.14

Table 1: Workers in low-wage jobs who are Financially Vulnerable are more likely than those who are Coping or Healthy to be women, ages 30-49, have someone in their household with a disability, or to be parents or caregivers.

| All respondents | Healthy (13%) | Coping (62%) | Vulnerable (24%) | |

|---|---|---|---|---|

| Gender | ||||

| Male | 43% | 54% | 45%* | 34%*^ |

| Female | 55% | 44% | 55%* | 66%*^ |

| Race and ethnicity | ||||

| Black | 14% | 16% | 14% | 14% |

| Latinx | 19% | 13% | 20% | 16% |

| White | 53% | 56% | 53% | 57% |

| Age | ||||

| 18-29 | 36% | 34% | 38%* | 29%^ |

| 30-49 | 39% | 28% | 37% | 50%*^ |

| 50-64 | 25% | 38% | 25%* | 21%* |

| Children in the household | ||||

| Children | 31% | 20% | 29%* | 41%*^ |

| No Children | 66% | 78% | 67%* | 58%*^ |

| Household member with a disability 15 | ||||

| Disability | 39% | 15% | 37%* | 56%*^ |

| No disability | 57% | 83% | 60%* | 41%*^ |

| Caregiver for a family member or friend16 | ||||

| Caregiver | 39% | 23% | 39%* | 47%*^ |

| Not a caregiver | 55% | 75% | 54%* | 48%* |

* Statistically significant compared with Financially Healthy.

^ Statistically significant compared with Financially Coping.

Note: Percentages may not equal 100% due to respondents who selected “I don’t know” or non-responses. For more about the demographic characteristics of our sample, see Appendix I.

Figure 4: Workers with characteristics highly correlated with being

Financially Vulnerable are also more likely to have caregiving responsibilities.

† Percentages represent those who answered “somewhat” or “severely” limits.

* Statistically significant compared with men.

a Statistically significant compared with ages 50+.

^ Statistically significant compared with ages 18-29.

b Statistically significant compared with people without a disability in the household.

Workers in Low-wage Jobs Struggle With Savings, Adequate Insurance Coverage, and Paying for Essentials

Taking a closer look at the eight indicators of financial health, we see that workers in low-wage jobs struggle to varying degrees in all aspects of financial health. However, their lowest scores relate to having sufficient short-term savings to weather an emergency (Indicator 3), having sufficient long-term savings to meet financial goals (Indicator 4), and confidence in their insurance coverage (Indicator 7). For these workers, financial instability can lead to hardships such as worrying about not having enough food or needing to cut back on basic expenses.

Table 2: Workers in low-wage jobs struggle with many aspects of their financial health.

| Financial Health Indicator | Workers in low-wage jobs | All workers |

|---|---|---|

| 1. Spend is less than or equal to income | 67%* | 86% |

| 2. Pay all bills on time | 51%* | 72% |

| 3. At least 3 months of liquid savings | 40%* | 60% |

| 4. Are confident they are on track to meet long-term financial goals | 30%* | 44% |

| 5. Manageable amount of debt or no debt | 54%* | 73% |

| 6. Prime credit score | 51%* | 74% |

| 7. Are confident their insurance policies will cover them in an emergency | 36%* | 60% |

| 8. Agree with the statement: “My household plans ahead financially” | 50%* | 65% |

* Statistically significant compared with all workers.

Data for “All workers” comes from the Financial Health Pulse survey conducted in April and May of 2021 and represents only employed adults ages 18-64.

When asked about several potential sources of financial stress, the survey found that insufficient savings and the high cost of health insurance were the top reasons workers in low-wage jobs are stressed about their finances.

Figure 5: Savings and insurance are top sources of financial stress.

Based on answers to Q45: “How much financial stress does each of the following cause you on a scale from 1 to 4, with 1 being ‘does not cause stress’ and 4 being ‘high amount of stress’?’” Percentages represent those who report a “high” (4) or “moderate” (3) amount of stress.

“I have to shuffle money around, [decide] which bills to pay, when. If I am working full time, even overtime, [I] should earn enough not to do that.”

-Male Home Healthcare Worker

Short- and Long-Term Savings

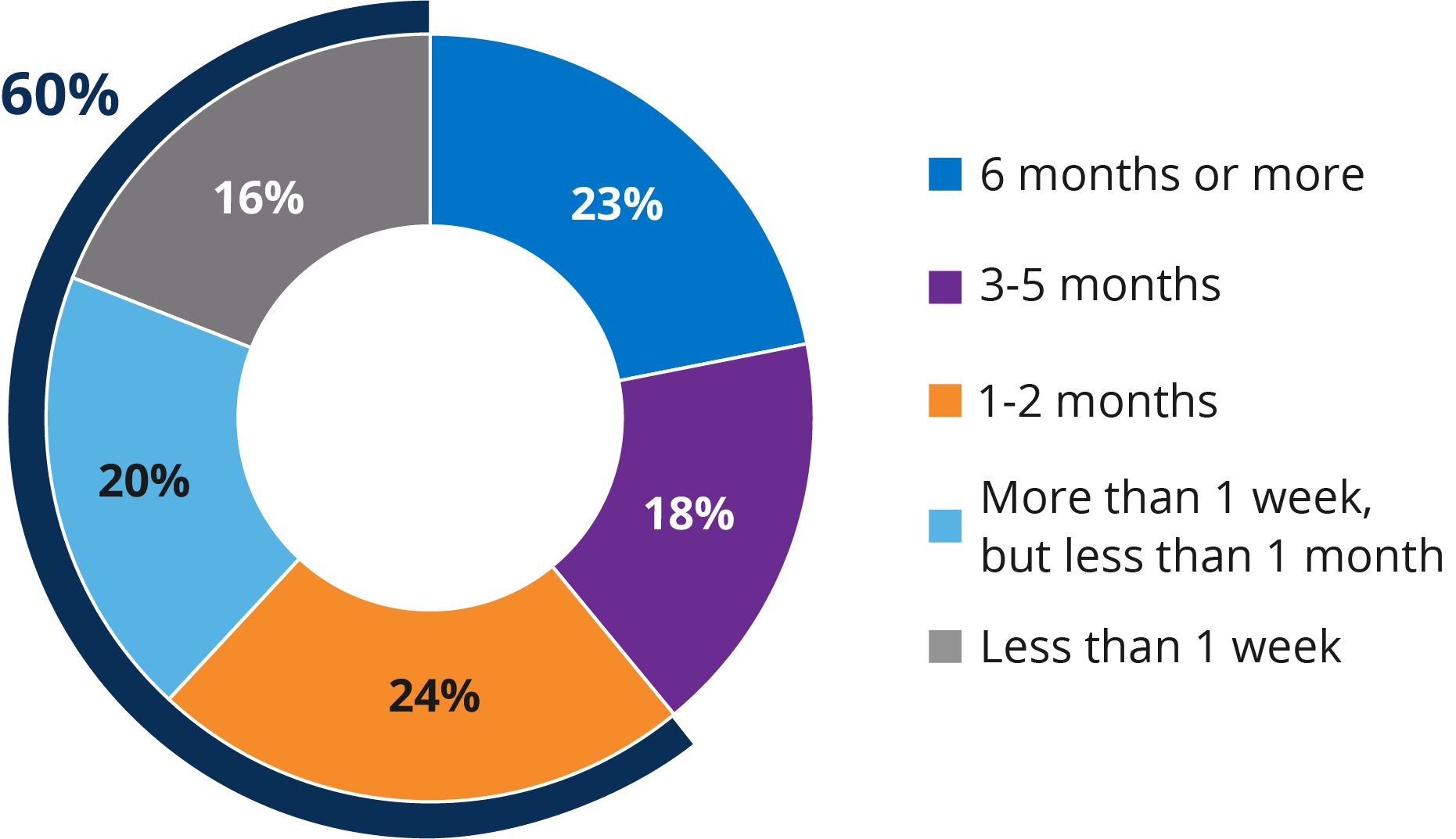

Many workers in low-wage jobs lack a savings cushion they can draw upon in an emergency. This leaves them vulnerable to financial shocks, such as unexpected spikes in expenses or a sudden loss of income.17 More than a third of workers in our sample (36%) would be unable to cover one month of living expenses with the funds they have in savings; 60% would be unable to cover three months of expenses.

Figure 6: Sixty percent of workers in low-wage jobs cannot cover three months of expenses with short-term savings.

Based on answers to Q35: “At your current level of spending, how long could you and your household afford to cover expenses, if you had to live only off the money you have readily available, without withdrawing money from retirement accounts or borrowing from friends/family or credit card?”

At the same time, nearly three-fourths of workers in low-wage jobs (70%) report that they are not confident their households are doing enough to meet their long-term goals, such as saving for education or putting money away for retirement. Further, when asked how much they have saved for retirement, 40% of workers report having zero dollars saved and 73% report having $10,000 or less. For those workers who are closest to retirement, the figures are similarly alarming: Nearly two-thirds of workers ages 50+ (63%) have $10,000 or less in retirement savings. These workers face the risk of significant hardship in their later years and may need to delay retirement or rely on financial support from others, often adult children, to supplement their benefits from Social Security.18

Figure 7: Workers in low-wage jobs aren’t confident they will reach long-term financial goals.

Based on answers to Q37: “Thinking about your household’s longer-term financial goals, such as saving for a vacation, starting a business, buying or paying off a home, saving for education, putting money away for retirement, or making retirement funds last… How confident are you that your household is currently doing what is needed to meet your longer-term goals?”

Figure 8: Workers in low-wage jobs are unprepared for retirement.

Based on answers to Q38: “Please estimate the total value your household currently has set aside for retirement in 401(k)s, IRAs, or other retirement accounts. Do NOT include your house, business assets, investment real estate, or savings likely to be used for some other purpose, such as educating your children or supporting your parents. Your best guess will do.” For respondents ages 50+, n = 462.

“One of my biggest concerns is not having enough for retirement. What happens if I can’t work?… A friend taught [me] that I should be contributing more [to my retirement plan], so I just started recently [after working with the company for 20 years].”

-Female home healthcare worker

Employers play an important role in workers’ ability to save and prepare for retirement in the United States, yet too few workers in low-wage jobs have access to retirement accounts via their employers. Nearly one-third of workers in our survey (32%) report that their employer does not offer any kind of employer-sponsored retirement plan, and 20% say they don’t know if their employer offers one. Among low-wage workers, those who work part-time, are employed by small businesses, and are on the lower end of the wage spectrum are even less likely to say that their employer offers a retirement plan.

Figure 9: Nearly one-third of workers in low-wage jobs say their employer does not offer a retirement plan of any kind.

Based on answers to Q11: “Does your employer offer any of the following retirement plans (such as a 401k, 403b, and/or a pension)? Select all that apply.”

Table 3: Part-time workers, workers for small businesses, and lower-earning workers are less likely to say that their employer offers a retirement plan.

| Full vs. part-time | Part-time (0-29 hours) | 34% |

| Full-time (30+ hours) | 54% | |

| Size of employer | < 50 employees | 33% |

| 50-499 employees | 61%^ | |

| 500+ employees | 62%^ | |

| Annual wages | < $20,000 | 42%a |

| Between $20,000 and $30,000 | 51%a | |

| Between $30,000 and $35,360 | 62% |

* Statistically significant compared with part-time workers.

^ Statistically significant compared with workers who work for employers with < 50 employees.

a Statistically significant compared with workers who have $30,000 to $35,360 in annual wages.

For more about the demographic characteristics of our sample, see Appendix I.

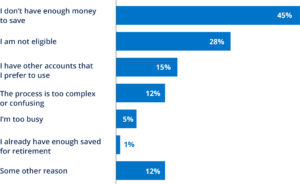

Yet even among those who report that their employer offers a retirement plan, only slightly more than half (55%) report being enrolled in it. The top reasons that workers report not enrolling in their plan are that they don’t have enough money to save and that they are ineligible.

Figure 10: Many workers who report that their employer offers a retirement plan are not enrolled.

Based on answers to Q12: “Are you enrolled in your employer’s retirement plan?”

Note: Asked only of respondents who reported that their employer offers a 401(k), pension, or 403(b) plan (n = 898).

Figure 11: Many workers don’t enroll in employer-provided retirement plans because they either don’t have enough to save or are ineligible.

“I don’t have any kind of retirement plan. I work full time and just got benefits after a full year. All other jobs I’ve had, I got benefits right away for full-time work.”

— Male home healthcare worker

Insurance Coverage

Having adequate insurance is critical to one’s ability to weather major events like a catastrophic illness or natural disaster, or even more minor events like a car accident, without damaging financial consequences. Yet, nearly two-thirds of workers in low-wage jobs (65%) either lack confidence that their household’s insurance coverage will support them in an emergency or have no insurance at all.

Figure 12: Workers in low-wage jobs lack confidence that their insurance will cover them in an emergency.

Based on answers to Q42: “Thinking about all of the types of personal and household insurance you and others in your household have (such as life insurance, health insurance, homeowners or renters insurance, etc.), how confident are you that those insurance policies will provide enough support in case of an emergency?”

Note: Percentages do not equal 100 due to rounding.

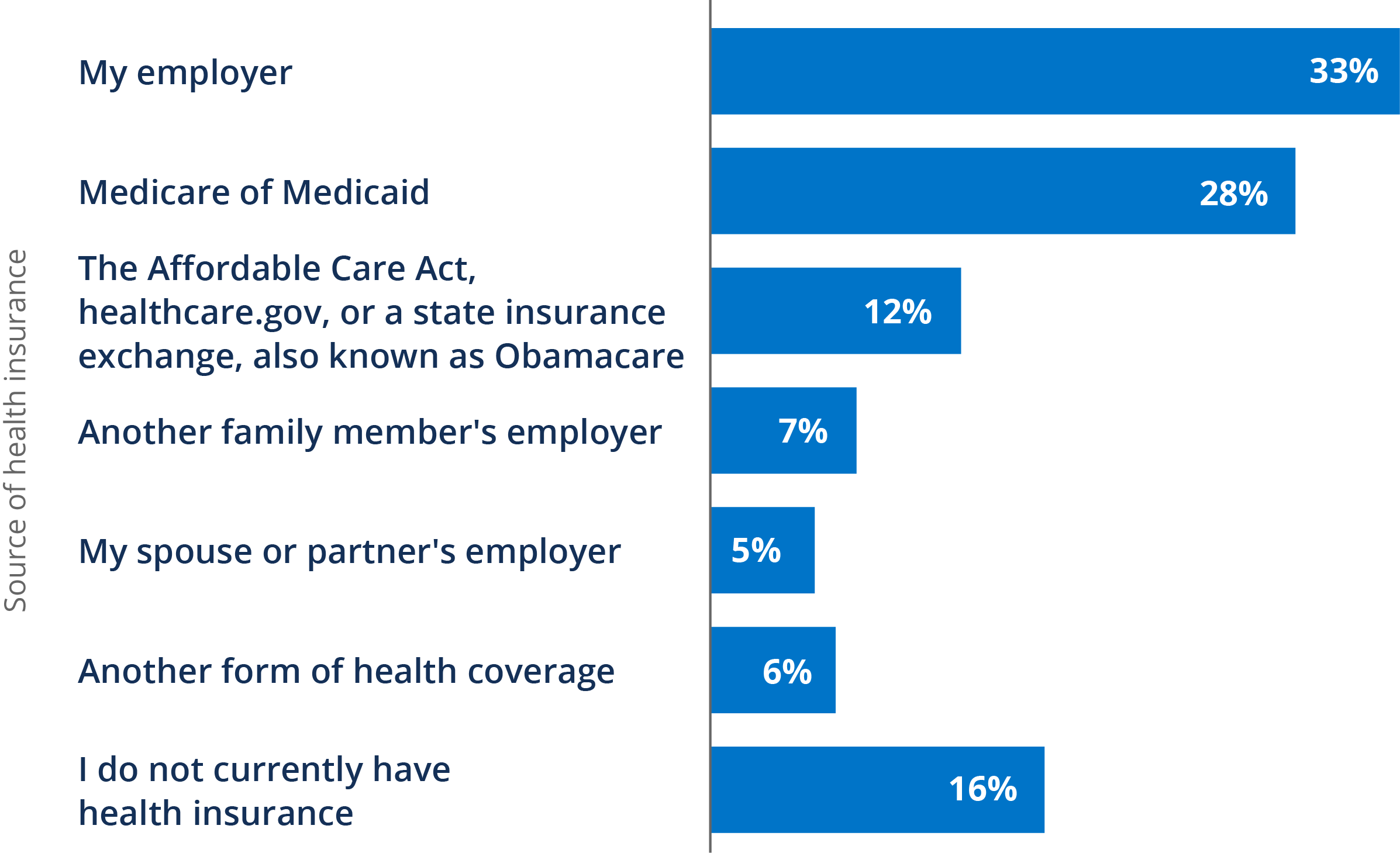

Health insurance in particular is an important bulwark against financial strain, as medical bills are the leading cause of bankruptcy in the United States.19 As with retirement savings, employers are the primary channel through which most American workers obtain health insurance coverage.20 Yet for many workers in low-wage jobs, the high cost of coverage can be a barrier to enrolling in insurance or using its benefits once enrolled – if they are eligible at all.

In our study, only one-third of workers in low-wage jobs (33%) report receiving health insurance coverage through their employers, and among those who do not, more than half (52%) say that they are not eligible for insurance from their employers. This could be either because the employer does not offer insurance at all or because the respondent does not meet the employer’s eligibility criteria. Of those workers who say they are eligible but still do not participate in their employer’s health insurance plan, nearly half (48%) say that it is because it is too expensive or the deductibles and copays are too high.

Figure 13: Only one-third of workers in low-wage jobs receive health insurance coverage through their employers.

Based on answers to Q16: “Do you currently have health insurance or health coverage of any of the following types? Select all that apply.” Note: Respondents may have more than one of these types of insurance.

Figure 14: More than half of those not receiving health insurance from their employer say they are not eligible for it.

Based on answers to Q17: “Are you eligible for health insurance through your employer?”

Note: Asked only of those who have health insurance from someone other than their employer or does not have health insurance (n = 1,096). Percentages do not equal 100 due to rounding.

Figure 15: Nearly half of workers in low-wage jobs who are eligible for employer-provided insurance but don’t participate say it is because of the high cost.

Based on answers to Q18: “You indicated that you are eligible for health insurance from your employer but are not currently enrolled. Please indicate the reason(s) you are not enrolled. Select all that apply.”

Note: Asked only of respondents who reported that they are eligible for health insurance coverage through their employer but do not participate (n = 321).

“[My employer] offers health insurance and I work enough hours to qualify, but I can’t afford it. I would like to enroll, but I can’t.”

— Female retail worker

The high cost of health coverage can create significant hardship for workers in low-wage jobs, even for those who have access to health insurance through their employers. More than one-third of workers with employer-sponsored health insurance (36%) report avoiding getting healthcare or skipping medication in the past 12 months. The most frequently cited reasons are that the insurance copay or deductible is unaffordable.

Figure 16: Many workers with employer-provided coverage who avoid healthcare or skip medication do so because of unaffordable costs.

Based on answers to Q19: “In the past 12 months, did you avoid getting healthcare, or delay/skip medication you thought you needed for any of the following reasons? Select all that apply.”

Note: Percentages in the table are only among the 36% of workers with employer-sponsored health insurance who chose an answer other than “Doesn’t apply to me/I did not avoid getting needed care” (n = 207).

Financial Hardship

Low-wage work is associated with significant financial hardship for workers and their families. Roughly one-third of workers reported having trouble paying their rent or mortgage (31%), struggling to pay medical bills (32%), or worrying about running out of food (37%) in the 12 months before the survey. When it comes to medical bills in particular, many report taking actions such as reducing spending on basic needs, skipping other monthly payments, drawing down savings, or taking on more debt to cope with unmanageable medical expenses. These can all have significant long-term impacts on workers’ financial health, making it harder to manage day-to-day expenses and plan for the future.

Table 4: Workers in low-wage jobs worry about being unable to pay bills or running out of food.

| Worried about our food running out before getting money to buy more | 37% |

| Someone in household had trouble paying medical bills | 32% |

| Had trouble paying our rent/mortgage | 31% |

Based on answers to Q48: “In the past 12 months, would you say this applied to you often, sometimes, rarely or never?” Percentages represent those who answered “often” or “sometimes.”

“[I] got injured on the job three months in, [and had] no health insurance. I had workers’ comp insurance through my job, but I did have to pay medications out of pocket. I wasn’t working during that time, so I had to use my savings to recover just to get back to work.”

— Male home healthcare worker

There are other indications that workers in low-wage jobs are struggling financially. Nearly one-third of workers (31%) report that someone in their household has received food stamps in the prior year. The same percentage (31%) reports that they currently have past-due medical bills. Medical bills are the leading cause of bankruptcy in the United States, and people of color and those with disabilities are among those most likely to experience medical debt and its adverse complications. 21 A smaller but still sizable proportion of workers (12%) says they have outstanding payday loans – which is particularly striking given that only 3% of the total U.S. population reports having taken a payday loan in the entire prior year.22

Table 5: Many workers in low-wage jobs rely on food stamps, have unpaid medical debt, and use payday loans.

| Received food stamps in the prior 12 months | 31% |

| Has past-due medical bills | 31% |

| Has payday loans | 12% |

Based on the answers to Q44 (“In the past 12 months, did you or anyone in your family receive any of the following public benefits? Please include benefits received by you, your spouse or partner (if applicable) and any of your children or stepchildren under 19 who are living with you.”) and Q40 (“Do you or anyone in your household currently have any of the following types of debt?”).

Workers in Low-wage Jobs Who Believe Their Employers Help Them Improve Their Financial Health Are More Satisfied and Committed to Their Employers

There are a variety of actions that employers can take – and that many already are taking – to improve the financial health of their workers, which we discuss in more detail below. These include providing wages that allow workers to cover their expenses and save for the future, benefits that help workers meet their financial goals and provide protection against risk, and scheduling that offers stability for workers and their families.

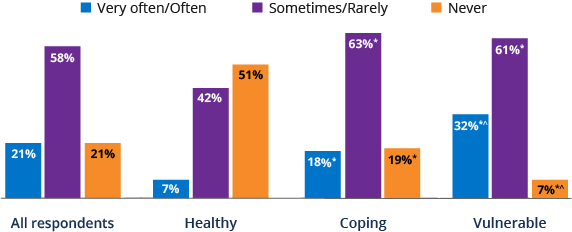

Investing in their workers’ well-being is in employers’ interest as well. Nearly one-fourth of workers in low-wage jobs (21%) – and almost one-third of those who are Financially Vulnerable (32%) – say that their financial stress negatively impacts their performance at work. Workers in low-wage jobs report spending an average of 1.3 hours per week dealing with personal finance-related issues when they are at work, adding up to 66 hours of lost productivity each year due to financial stress.

Figure 17: Workers in low-wage jobs report that financial stress frequently impacts their work performance negatively.

Based on answers to Q46: “In the past 12 months, how often would you say financial stress has negatively impacted your performance at work?”

* Statistically significant compared with Financially Healthy.

^ Statistically significant compared with Financially Coping.

Table 6: Workers in low-wage jobs spend significant time at work each week dealing with personal finance issues.

| All respondents | Healthy | Coping | Vulnerable |

|---|---|---|---|

| 1.3 hours | 0.5 hours | 1.2 hours* | 1.9 hours*^ |

Based on answers to Q47: “Approximately how many hours per week on average do you spend at work dealing with personal finance-related issues (for example contacting creditors, managing bank accounts)?”

* Statistically significant compared with Financially Healthy.

^ Statistically significant compared with Financially Coping.

Equally important, especially during the Great Resignation, is the impact of investing in workers’ well-being on their job satisfaction and loyalty to the company. Workers in low-wage jobs who say that their employers help them improve their financial health are significantly more likely to recommend the company to friends or family – a common measure of employee satisfaction – and are less likely to say that they will look for a job in the coming year.

Figure 18: Workers in low-wage jobs who say their employer helps them improve their

financial health are more satisfied and committed to their employer.

* Statistically significant compared with “Disagree.”

Percentage of workers who believe their employer supports their financial health are based on answers to Q51: “Still thinking about your main job, to what extent do you agree or disagree with this statement: “My employer helps me improve my financial health.” Percentages indicate those who answered “Agree strongly/somewhat” or “Disagree strongly/somewhat.”

Percentage of workers who would recommend their employer are based on answers to Q27: “Still thinking about your main job, on a scale of 0-10, how likely is it that you would recommend your employer to a friend, family, or colleague? Please use a scale of 0 to 10, where 0 is ‘Not At All Likely’ and 10 is ‘Extremely Likely.’” Percentages represent those who answered 9 or 10, whom the Employee Net Promoter Score (eNPS) methodology considers to be “promoters.”

Percentage of people who are likely to stay with their employer are based on answers to Q30: “How likely are you to try to find a job with another employer within the next 12 months?” Q30 was asked only of those who report that they are not planning on retiring or stopping work in the next 12 months (n = 1,617).

“If you want people to be proud of where they work, you’d think they’d invest in long-term engagement, like retirement. It doesn’t incentivize people to stay long term.”

— Male home healthcare worker

How Employers Can Improve Worker Financial Health

Employers have an important role to play in improving the financial health of their workforce, particularly those who are in low-wage jobs. The findings of this survey suggest several actions that can have a meaningful impact on worker well-being.

1. Increase Workers’ Wages

Wages are a critical input to financial health, and most low-wage jobs do not provide enough for workers to meet their daily expenses, let alone set aside money for the future. Our findings show that many workers in low-wage jobs rely on their wages to support their families, and many are struggling financially as a result. Companies can use tools like MIT’s Living Wage Calculator or partner with organizations like the Good Jobs Institute or Living Wage For US to assess what percentage of their workforce is making less than a living wage, and adjust wages accordingly. Hershey conducts an annual living wage assessment for all of its global full-time employees and is committed to adjusting any wages that fall below a living wage.23

2. Provide High-quality and Affordable Insurance Coverage

Many workers in low-wage jobs do not have health insurance through their employer, either because their employer does not offer it or they do not qualify. Moreover, our findings suggest that even when they do have employer-provided insurance, many workers in low-wage jobs go without needed care because their deductibles and copays are too high. Employers can help their workers remain healthy while protecting them from the financial hardship associated with medical debt by ensuring that plans are affordable.24 Companies should also make sure that all employees, including hourly, part-time, and temporary employees, have access to quality health coverage. Chipotle provides all crew members (hourly restaurant staff) with basic preventative health care coverage, a dental PPO, and a vision PPO.25

3. Promote Retirement Savings

Workers in low-wage jobs lack adequate retirement savings, putting them and their families at risk for hardship as they age. Providing all workers with the ability to save by offering a 401(k) or other retirement plan is a critical first step. Yet our findings show that even some workers who have access to a retirement plan at work do not use it because they cannot afford to save, thus reinforcing the need for wage increases and other benefits that can support workers’ financial health. Target recently announced a new starting wage range from $15 to $24 and reduced waiting periods for access to the company’s 401(k) plan.26 Employer contributions to 401(k) plans – especially when designed to incentivize small-dollar contributions – can also provide a big boost to the retirement savings of workers in low-wage jobs.27

4. Offer Emergency Savings Opportunities

Short-term savings can provide a critical buffer to help workers weather financial shocks without taking on debt or withdrawing from retirement savings. However, many workers in low-wage jobs lack this critical savings cushion. There are many ways that employers can help their workers build up emergency savings, including offering split direct deposit and allowing employees to make after-tax contributions to a separate “rainy day” account within or outside of existing 401(k) programs. UPS, with support from the collaboration between Commonwealth and Voya Financial as part of BlackRock’s Emergency Savings Initiative, is offering an in-plan emergency savings option to its 90,000 U.S. based nonunion employees, providing them with a way to set aside after-tax savings automatically as part of their 401(k) plan administered by Voya.28

5. Provide Support for Childcare and Other Caregiving Needs

Our findings suggest that caregiving responsibilities have a significant impact on the financial well-being of workers in low-wage jobs. Employers have an opportunity to ease this burden for their workforce by providing benefits that support the needs of caregivers. This includes providing paid time off for medical and caregiving purposes, as well as offering subsidies to help workers pay for childcare, eldercare, disability-related equipment and services, and related needs.29 Levi Strauss & Co. provides all of its U.S. corporate and benefits-eligible retail employees up to eight weeks of paid time off annually to care for an ill spouse, domestic partner, parent or stepparent, child or stepchild up to 18 years of age.30

6. Offer Stable and Predictable Scheduling

Many workers in low-wage jobs face unstable and unpredictable schedules, with little or no advance notice of shifts, requirements to be “on call,” and last-minute shift cancellations without compensation. While scheduling was not a focus of this report, ample research by others has demonstrated the harmful effect that this scheduling instability can have on workers’ economic security, psychological well-being, physical health, and family life.31 Companies should ensure that their scheduling practices provide stability for their hourly workforce. Costco provides its employees with schedules two weeks in advance and guarantees a minimum of 24 hours per week for part-time workers.32,33

Taking steps like these to address workers’ financial needs can have an impact that extends far beyond the individual workers. By taking a more active role in improving financial resilience for employees, employers also stand to see benefits in terms of both financial and human capital. What’s more, as employers take action in greater numbers to support workers’ financial health, the impacts of those actions stand to ripple outward and positively influence our economy as a whole.

Additional Resources for Employers

In addition to the specific recommendations outlined above, there are many other ways that employers can support the financial well-being of their workforce. These include helping employees pay down debt or build credit, providing emergency grants to help them cope with unexpected expenses, offering coaching services that provide more hands-on guidance, and helping them build wealth through stock ownership. The following resources published by the Financial Health Network provide additional guidance and employer examples:

- Employer FinHealth Toolkit: Our comprehensive guide to building better employee financial health strategies.

- Guide to Employee Financial Health Solutions: A supplement to our Toolkit, providing an overview of potential solutions to address specific health challenges.

- Using Data and Design to Increase Equity in Employee Financial Health: Our brief outlining how to design and implement an employee financial health program in ways that increase workforce equity.

Acknowledgments

The Financial Health Network thanks several individuals who contributed their time and expertise to this research. Adrian Haro of The Workers Lab provided valuable input on the research design and reviewed drafts of the report. Tanya Wallace-Gobern of the National Black Worker Center, Rohma Khan of One Fair Wage, and Angelina Del Rio Drake of PHI all provided thoughtful feedback on the survey instrument and early findings. Ray Kluender of Harvard Business School also provided helpful input on the survey instrument.

In addition, the authors would like to thank their current and former Financial Health Network colleagues Steve Arves, Matt Bahl, Fawziah Bajwa, Naomi Adams Bata, Thea Garon, Meghan Greene, Rob Levy, Jess McKay, Dan Miller, Jacquelyn Reineke, David Silberman, Chris Vo, and Andrew Warren for their invaluable contributions to this research.

We appreciate Jordon Peugh, Jania Marshall, and their colleagues from SSRS for their collaboration on the design and execution of the survey and on the data analysis.

This research was made possible through the support of the Target Foundation. The findings, interpretations, and conclusions expressed in this piece are those of the Financial Health Network and do not necessarily represent those of our funders or partners.

This report is part of the Financial Health Pulse™ research series. The Financial Health Pulse provides regular updates and actionable insights about financial health in America. The Financial Health Pulse is supported by the Citi Foundation, with additional funding from the Principal Foundation.

Financial Health of Workers in Low-wage Jobs

For definitions, data tables, and full details on methodology, download the PDF version of this report.

Endnotes

- Martha Ross & Nicole Bateman, “Meet the low-wage workforce,” Brookings Institution, 2019.

- Our sampling approach sought to account for the variability of earnings, especially in occupations where tipping is prevalent, such as restaurant work, while not burdening the respondent for whom tips are a significant portion of their earnings with the task of calculating an average hourly wage. Respondents who reported being paid hourly were asked to report their hourly wages not including overtime pay, tips, or commissions. All respondents were then asked to report annual earnings including bonuses, overtime pay, tips, or commissions. Respondents who reported earning more than $35,360 per year, even if their reported hourly wage was $17 or less, were excluded from the survey.

- Martha Ross & Nicole Bateman, “Meet the low-wage workforce,” Brookings Institution, November 2019. For the purposes of this study, we defined low-wage workers as people earning up to $17 per hour. See the Methodology section for more details.

- Ibid.

- “Fact sheet: Occupational segregation in the United States,” Washington Center for Equitable Growth, October 2017.

- Karen Schulman, Jasmine Tucker, & Julie Vogtman, “Nearly One in Five Working Mothers of Very Young Children Work in Low-Wage Jobs,” National Women’s Law Center, April 2017.

- Vincent A. Fusaro & H. Luke Shaefer, “How should we define ‘low-wage’ work? An analysis using the Current Population Survey,” U.S Bureau of Labor Statistics, Monthly Labor Review, October 2016.

- Victoria Smith & Brian Halpin, “Low-wage Work Uncertainty often Traps Low-wage Workers,” Center for Poverty Research, UC Davis.

- The Shift Project has published numerous studies demonstrating the link between unstable scheduling and worker and family well-being outcomes.

- See the Methodology section for more details on the approach to calculating the three financial health tiers.

- We define “primary earners” using a combination of two survey questions. In Q31, respondents were asked: “Is your spouse, partner, or another adult in your household currently working for pay or self-employed?” Those who reported that there is another working adult in their household (“Yes” to Q31) were then asked Q32: “Are you the person in your household who typically contributes the most to the household income?” Primary earners are those who do not have another working adult in their household (“No” or “No other adult in the household” to Q31) or who do have another working adult in the household but report contributing the most to household income (“Yes” to Q32).

- This report uses a binary variable for participants’ gender given available data. However, emerging literature indicates that individuals who identify as nonbinary, gender-nonconforming, genderqueer, or another gender face heightened financial health challenges. More research is needed to understand the experiences of workers who identify as a gender other than male or female, particularly those in low-wage jobs.

- This report focuses on Black and Latinx workers in particular because they are overrepresented in low-wage jobs relative to their share of the overall workforce, and because of the legacy of historic racism and discrimination and ongoing structural barriers to financial health that these communities face.

- Martha Ross & Nicole Bateman,“Meet the low-wage workforce,” Brookings Institution, November 2019.

- This survey identifies respondents who have a household member with a disability using a modified version of the six questions used by the U.S. Census Bureau Current Population Survey. Specifically, Q53 asks, “Do you or someone in your household have severe difficulty with any of the following?” Anyone who answered “yes” to any of the following is considered to have a household member with a disability: “Serious difficulty hearing or is deaf”; “Serious difficulty seeing or is blind”; “Concentrating, remembering, or making decisions because of a physical, mental, or emotional condition”; “Walking or climbing stairs”; “Dressing or bathing”; “Doing errands alone such as visiting a doctor’s office or shopping because of a physical, mental, or emotional condition.” Anyone who answered “no” to all of the above is considered not to have a household member with a disability.

- The survey considers respondents to be caregivers if they answer “yes” to Q52: “In the past 12 months, did you spend any time assisting a family member or close friend (for example, a parent, grandparent, wife, husband, adult child, other family member, neighbor or close friend) with their basic personal activities? By that we mean daily activities such as dressing, eating, bathing, paying bills, managing medication, food preparation, grocery shopping, doctor visits, emotional support, driving, and other types of personal assistance. This does not include routine childcare.”

- “How Do Families Cope With Financial Shocks?,” Pew Charitable Trusts, October 2015.

- Barbara A. Butrica & Eric J. Toder, “Are Low-Wage Workers Destined for Low Income at Retirement?,” Urban Institute, Retirement Policy Program, Older Americans’ Economic Security, September 2008.

- Michelle Proser & Uzma Amin, “Preventing Medical Debt: Recommendations for Employers,” Financial Health Network, March 2022.

- “Health Insurance Coverage of the Total Population (CPS),” KFF, 2020.

- Michelle Proser & Uzma Amin, “Preventing Medical Debt: Recommendations for Employers,” Financial Health Network, March 2022.

- Elaine Golden, Hannah Gdalman, Meghan Greene, & Necati Celik, “FinHealth Spend Report 2022,” Financial Health Network, April 2022.

- “Ensuring a Living Wage Across Hershey and Our Supply Chain,” Hershey Company, retrieved May 2022.

- Michelle Proser & Uzma Amin, “Preventing Medical Debt: Recommendations for Employers,” Financial Health Network, 2022.

- “Benefits,” Chipotle, retrieved May 2022.

- “Target to Set New Starting Wage Range and Expand Access to Health Care Benefits to More Team Members,” Target, February 2022.

- Tanya Ladha, “Using Data and Design To Increase Equity in Employee Financial Health,” Financial Health Network, April 2022.

- “A Case Study in Workplace Emergency Savings: How UPS and Voya Designed a Solution Resulting in $10 Million in Savings,” Commonwealth, March 2022.

- Jess McKay, Jessica Mason, & Thea Garon, “Unpaid and Unprotected: How the Lack of Paid Leave for Medical and Caregiving Purposes Impacts Financial Health,” Financial Health Network & National Partnership for Women and Families, September 2021.

- “Levi Strauss & Co. Announces Industry-Leading Paid Family Leave Benefit,” Levi Strauss & Co., BusinessWire, February 2020.

- See The Shift Project for numerous studies demonstrating the link between stable schedules and worker well-being.

- “Tackling Unstable and Unpredictable Work Schedules: A Policy Brief on Guaranteed Minimum Hours and Reporting Pay Policies,” Center for Law and Social Policy, Retail Action Project, & Women Employed, May 2014.

- “Employees | Costco,” Costco, retrieved May 2022.