Emergency Savings, Combined with Support Networks, Reduced Hardships During the Pandemic

This research was produced by the Financial Health Network in collaboration with BlackRock’s Emergency Savings Initiative. ESI is a cross-sector program with a mission to help people living on low to moderate incomes gain access to and increase usage of proven savings strategies and tools – ultimately helping them establish an important safety net.

People who were not saving for emergencies near the start of the pandemic were three times as likely to turn to friends or family for financial support (15% vs. 5%) as people who were saving.

People who were saving for emergencies and accessed resources from family or friends were associated with a 25% lower risk of hardship.

Turning to Family and Friends as an Emergency Resource

For those who did not have access to emergency savings in 2021, family borrowing served as an alternative source of emergency funds. In our analysis, we found that people who were not saving for emergencies in spring 2020 were 3 times as likely (15% vs. 5%) to have borrowed from family or friends in the past 12 months.

However, the relationship is not a simple one. The analysis also revealed that people who were not saving for emergencies were just as likely as those who were saving to financially support their family members. In fact, 40% of both groups – savers and non-savers – reported providing financial support to family members last year.

Further, many people who don’t have emergency savings fell into both categories – they were supporting family members and also borrowing from family members during the year. More than twice as many people who were not saving for emergencies both borrowed from and supported family, compared with those who were saving (8% vs.3%). This underscores the complex dynamic between saving formally, accessing financial institutions, and tapping family as an emergency resource, suggesting people must often make tricky financial trade-offs.

Family Borrowing Could Reduce Immediate Hardship, but Not Stress

Financial support from family can be a crucial lifeline to reduce the worst effects of emergencies or financial instability, and might also help people avoid hardship in the first place. In our analysis, we found that respondents who borrowed money from family to cope with the COVID-19 pandemic were 17% less likely to experience hardship between spring 2020 and spring 2021, after controlling for fixed effects and changes in income and expenses. This means that the likelihood of experiencing hardship declined on average from 25% to 21% if they borrowed from family.

However, borrowing from family members was not a silver bullet for those struggling to make it through during COVID-19. Those who borrowed from family members to deal with the effects of COVID-19 were likely to have slightly lower financial health scores than those who didn’t borrow. They also experienced higher financial stress. This means that while borrowing from family members helped people to avoid the worst of a financial emergency, it did not drive a recovery in financial health scores.

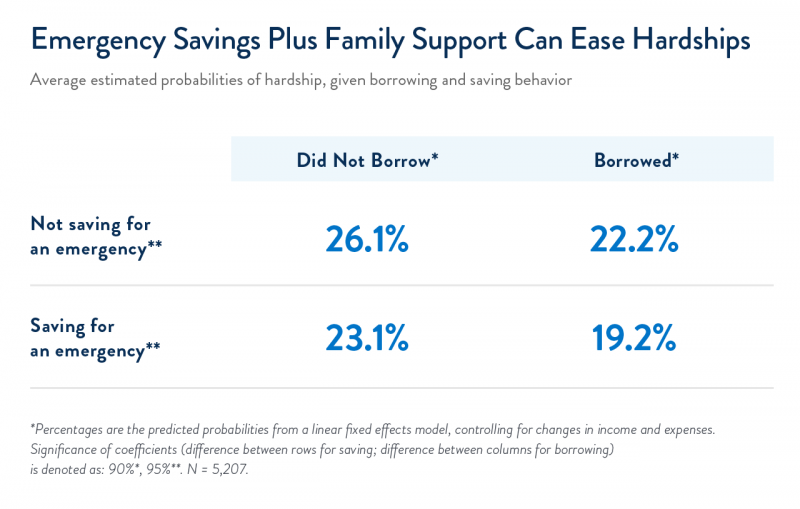

Emergency Savings Plus Family Support Can Act as Two Lines of Defense in Weathering Shocks

Having access to both emergency savings and financial support from family members can provide multiple layers of security in case of a financial shock. Someone who is saving for an emergency and is able to borrow from family members is 7 percentage points less likely to experience financial hardship than someone who is neither saving nor able to borrow.

Supporting Emergency Savings And Family Borrowing Can Strengthen Safety Nets

Understanding the pathways of mutual support among family and friends is vital to supporting traditionally underserved communities. However, financial support between households can only do so much to avoid the worst impacts of financial shocks.

Helping people balance their own emergency savings behavior and financial interactions with family or friends can create a strong safety net for families as they face future challenges. Two ways that financial institutions can support families in this balancing exercise are to increase access to emergency savings for individuals and families, and to reduce barriers to family giving and borrowing. These solutions can work together to better prepare families for emergencies like the pandemic.

Methodology Notes

Data in this report come from the Financial Health Pulse Survey Q2 2020 and Q2 2021 waves (April – June 2020 and April – May 2021) . These surveys were both fielded to USC’s nationally representative Understanding America Panel (UAS), allowing us to assess the responses of individuals who participated in both and change over time. The final sample included in this analysis was 5,254 individuals over 18 years old. In this analysis, we define “borrowing” as people asking for help to cope with the effects of the pandemic or the costs of medical care, and “giving” as giving to friends and family from their stimulus payment, to provide assistance, or as remittances abroad. We consider people to have been saving in 2020 if they answered that they were “currently saving for an emergency” during the 2020 survey. All models were run as fixed effects (OLS) regressions using a balanced panel across the two survey waves, controlling for changes in income, expenses, and family structure. Financial health was measured according to the Financial Health Network’s FinHealth Score® methodology.

BlackRock’s Emergency Savings Initiative

BlackRock announced a $50 million philanthropic commitment to help millions of people living on low to moderate incomes gain access to and increase usage of proven savings strategies and tools – ultimately helping them establish an important safety net. The size and scale of the savings problem requires the knowledge and expertise of established industry experts that are recognized leaders in savings research and interventions on an individual and corporate level. Led by its Social Impact team, BlackRock is partnering with innovative industry experts Common Cents Lab, Commonwealth, and the Financial Health Network to give the initiative a comprehensive and multilayered approach to address the savings crisis.

![]()