Unbanked, Underbanked, or Something Else Entirely?

As digital wallets, online banks, and fintech apps become everyday tools, the meaning of financial inclusion is shifting. Are our metrics keeping pace?

The unbanked population may be smaller than commonly estimated, with as many as 1 in 5 unbanked households holding online-only bank accounts.

Widespread use of nonbank financial products challenges traditional distinctions between “mainstream” and “alternative” financial services.

The addition of P2P wallets, BNPL, and cash advance apps substantially changes estimates of the underbanked population.

Differences between “transactional underbanked” and “credit underbanked” households reveal insights for providers to improve financial outcomes.

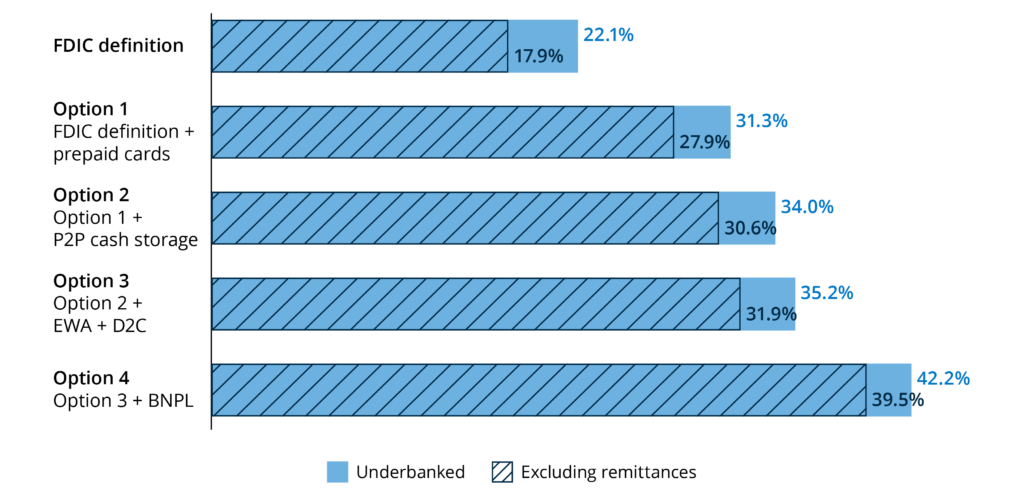

Data Spotlight: How Many Households Are Underbanked?

The size of the underbanked population varies, depending on which products are considered costly or risky.

Share of U.S. households considered underbanked using alternative underbanked definitions.

Notes: FinHealth Spend 2025 survey data. N = 5,096.

Our Supporter

This research is made possible through the financial support of Wells Fargo’s Banking Inclusion Initiative. Launched in 2021, Wells Fargo’s Banking Inclusion Initiative provides easier access to low-cost banking and financial education for underbanked and unbanked communities. An estimated 24.6 million U.S. households are underbanked or unbanked, often resorting to higher-cost, less secure alternatives to manage their money. For more information, please visit: https://www.wellsfargo.com/about/inclusion/banking-inclusion-initiative/.

![]()

Unbanked, Underbanked, or Something Else Entirely?

Explore the trends. Discover new insights. Build stronger strategies.