Who Trusts Financial Institutions?

New Financial Health Pulse® data show that trust in financial institutions is uneven, with substantial racial and ethnic disparities across key dimensions of banking.

How Much Do People Trust Financial Institutions?

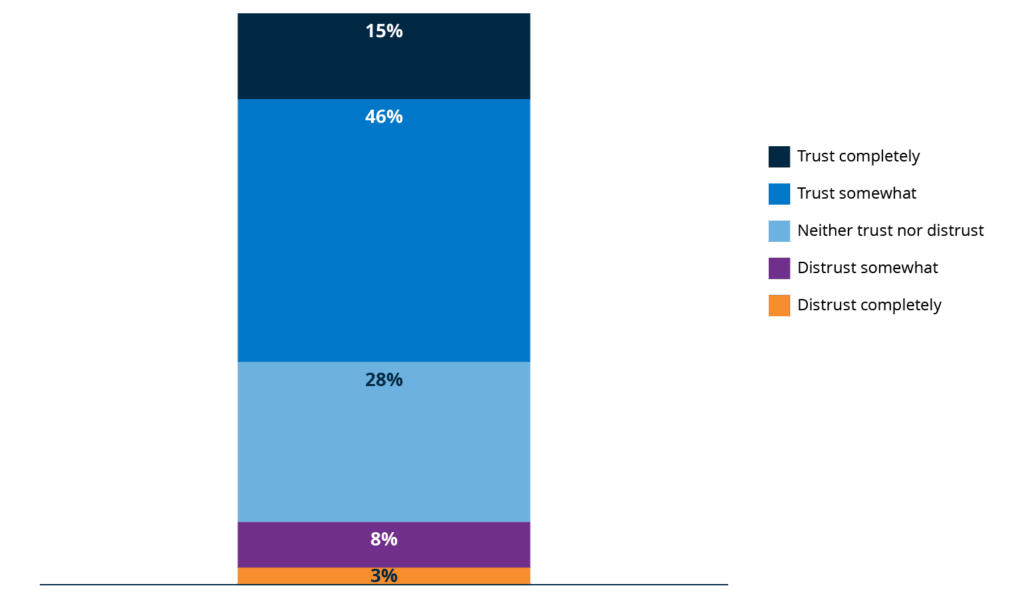

In the 2025 Financial Health Pulse survey, a slight majority of Americans (61%) reported that they trust financial institutions “somewhat” or “completely” (Figure 1).6 Nearly 4 in 10 Americans feel uncertain, hesitant, or outright skeptical: 28% reported neither trusting nor distrusting financial institutions, and 11% reported distrusting them somewhat or completely.

While we cannot directly compare trust in financial institutions to other public institutions using our data, national polling has estimated that public confidence in banks stands at levels near that of other polarizing institutions, such as the U.S. presidency, the Supreme Court, and the medical system.7

Figure 1. A majority of Americans trust financial institutions, but uncertainty remains widespread.

Percentage of U.S. households, by self-reported level of trust in financial institutions.

Notes: 2025 Financial Health Pulse survey data. N = 7,423.

In response to the question: “In general, how much do you personally trust financial institutions such as banks or credit unions?”

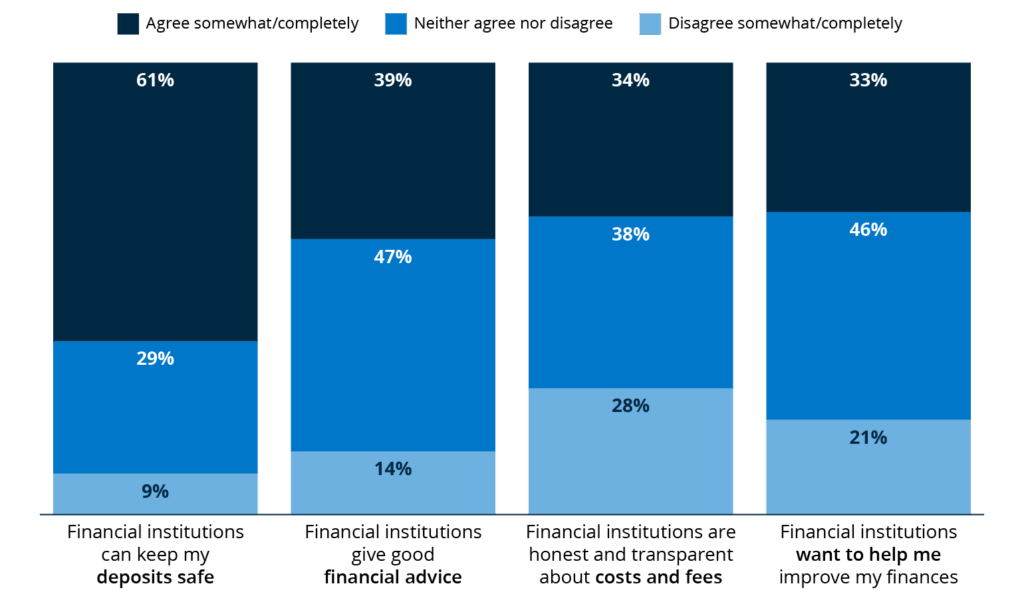

When people say they trust financial institutions, what exactly are they placing their trust in? To answer this question, we asked respondents to rate their level of confidence in financial institutions’ ability to serve their needs across four core dimensions: keeping deposits safe, giving good financial advice, being honest and transparent about costs and fees, and demonstrating interest in improving customers’ financial health.

Deposit safety emerged as the most trusted component, with a majority of consumers (61%) agreeing that financial institutions keep their deposits safe (Figure 2). Still, nearly 4 in 10 consumers expressed doubts about their financial institutions’ ability to protect their deposits. This is a striking finding, given that deposit security is a core function of banks and credit unions.

Confidence declined further across other dimensions of trust. Only 39% of respondents agreed that financial institutions provided good financial advice, 34% agreed that they were transparent about costs and fees, and just 33% agreed that banks genuinely wanted to improve their financial health (Figure 2). Over a quarter of consumers (28%) outright disagreed that financial institutions were honest and transparent about costs and fees.

Overall, these findings suggest that many consumers question not only the fairness and transparency of financial institutions, but also their intentions and ability to support financial well-being—all of which are key to sustaining deeper trust.

Figure 2. Trust in financial advice, transparency, and support for financial health lags behind trust in deposit security.

Percentage of U.S. households who agree, neither agree nor disagree, or disagree with the following statements about dimensions of trust.

Notes: 2025 Financial Health Pulse survey data. N = 7,423. Responses to the question: “To what extent do you agree or disagree with each of the following statements about financial institutions, like banks and credit unions?”

Racial and Ethnic Disparities in Trust

Institutional trust is shaped by people’s lived experiences and backgrounds. In the United States, some of the most pronounced disparities in institutional trust appear along racial and ethnic lines. Prior research consistently shows that Black and Latine households report lower levels of trust across a wide range of institutions, driven by long-standing exclusionary and discriminatory practices.

In education, studies show that student awareness of racial bias, such as perceptions of discriminatory or unfair treatment, predicts loss of trust in schools.8 In policing, widespread beliefs that the criminal justice system disadvantages Black Americans—combined with personal and vicarious experiences of discrimination, racial profiling, and unequal treatment from law enforcement—weaken trust in police and related public institutions.9,10,11,12 In health care, delayed diagnoses, inadequate treatment, and medical bias have similarly contributed to diminished trust in public health systems.13 Together, these patterns demonstrate how structural racism shapes institutional distrust across multiple domains.

Banking is no exception to this history. Black Americans, in particular, have long faced structural barriers to safe and affordable financial services, including exclusion from mainstream financial institutions, redlining that denied access to fair mortgages and credit in Black neighborhoods, and disproportionate exposure to predatory lending.14,15 Research has also shown that Black and Latine households are significantly more likely to be unbanked or underbanked in the U.S.16 Despite this well-documented history, there is little research measuring racial and ethnic disparities in trust in financial institutions in the U.S.

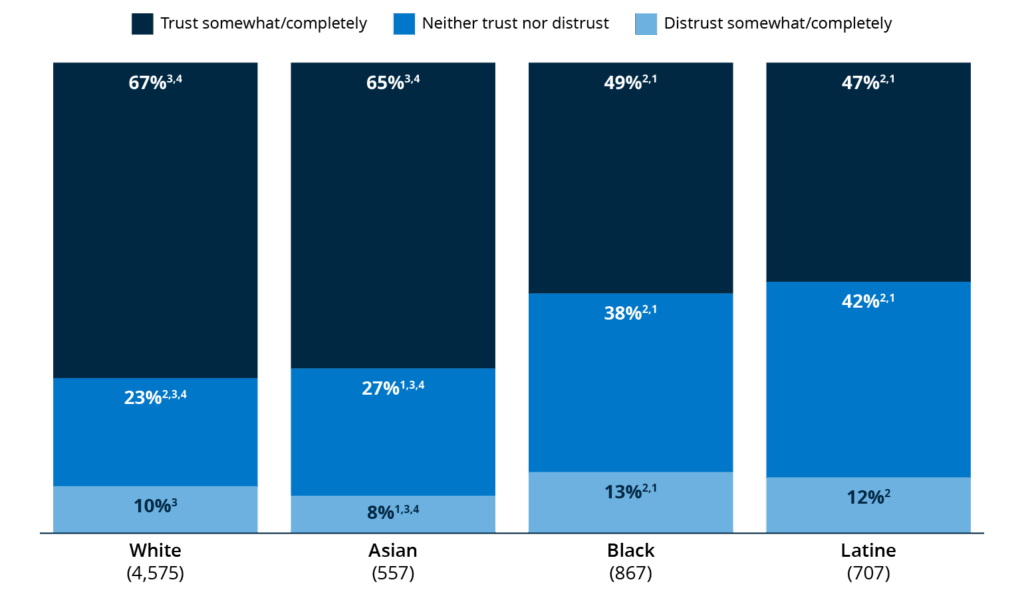

Our findings show that the relatively low levels of trust in the general population were substantially lower for Black and Latine households. Around two-thirds of Asian and white consumers reported trusting financial institutions somewhat or completely, compared with only around half of Black and Latine consumers (Figure 3).

Gaps in outright distrust were smaller, but still meaningful: 13% of Black consumers and 12% of Latine consumers reported distrusting financial institutions somewhat or completely, compared with 10% of white and 8% of Asian consumers. Further analysis shows that these disparities narrowed when controlling for income, but remained statistically significant.

Black and Latine consumers were also more likely to feel uncertain, conflicted, or apathetic about financial institutions, reflected in higher rates of reporting neither trust nor distrust. This indicates a more cautious or hesitant stance towards financial institutions in Black and Latine communities.

Figure 3. White and Asian consumers trust financial institutions more than Black and Latine consumers.

Levels of trust in financial institutions generally, by race and ethnicity.

Notes: 2025 Financial Health Pulse survey data. Other racial and ethnic identities were excluded due to sample size restrictions.

1 Statistically significant relative to white at p < .05

2 Statistically significant relative to Asian at p < .05

3 Statistically significant relative to Black at p < .05

4 Statistically significant relative to Latine at p < .05

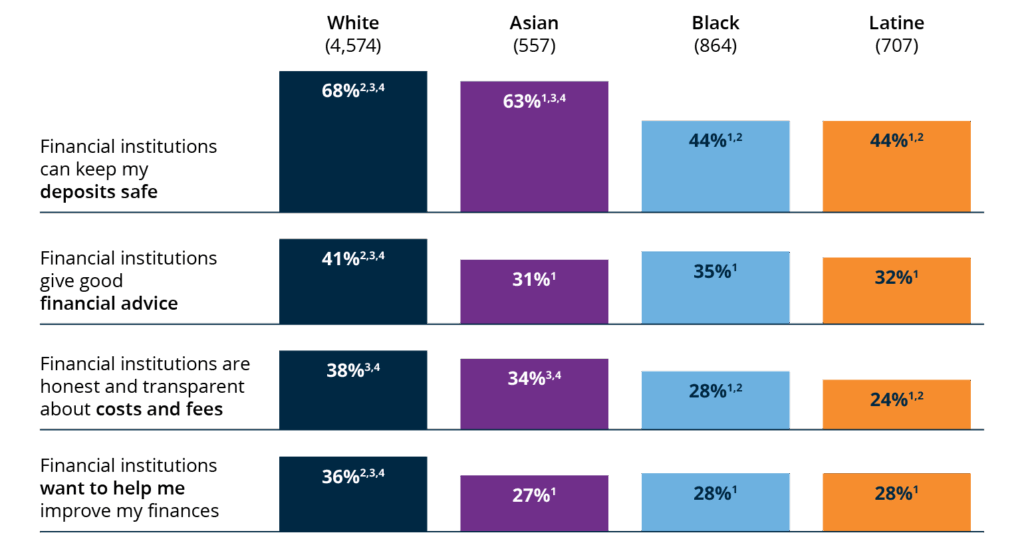

Racial and ethnic disparities persist across core banking functions, with Black and Latine households less likely than white households to agree that financial institutions serve their interests on all four dimensions of trust asked about in the Pulse survey. Notably, less than half of Black and Latine households agreed that financial institutions can keep their deposits safe (Figure 4). Even lower shares agreed that financial institutions provide good advice, are transparent, or want to help them improve their finances. These sentiments highlight deeper uncertainty among Black and Latine households about whether financial institutions can deliver on some of their most basic responsibilities.

Differences between Asian and white households were slightly more nuanced. While Asian and white consumers reported similar levels of trust in financial institutions’ ability to keep their deposits safe and in cost and fee transparency, Asian consumers were still less likely than white consumers to agree that financial institutions give good advice or that financial institutions want to improve their financial health. On these measures, Asian consumers’ trust levels were closer to those reported by Black and Latine households, indicating similar doubts about financial institutions’ intentions to help them improve their financial lives. Together, these results suggest that racial and ethnic differences in levels of trust vary widely, depending on the specific dimension of financial services.

Figure 4. Less than half of Black and Latine households agree that financial institutions can keep their deposits safe.

Percentage of households who agree “somewhat” or “completely” with the following statements about financial institutions, by race and ethnicity.

Notes: 2025 Financial Health Pulse survey data.

1 Statistically significant relative to white at p < .05

2 Statistically significant relative to Asian at p < .05

3 Statistically significant relative to Black at p < .05

4 Statistically significant relative to Latine at p < .05

Acknowledgements

The Financial Health Pulse is supported by the Principal Foundation. The findings, interpretations, and conclusions expressed in this piece are those of the Financial Health Network and do not necessarily represent those of our funders or partners.

![]()

Written by

-

Associate, ResearchFinancial Health Network

Associate, ResearchFinancial Health Network -

Manager, ResearchFinancial Health Network

Manager, ResearchFinancial Health Network