Pulse Points: Financial Health Differences Among Entrepreneurs

More people across the U.S. are starting businesses than ever before. What is the relationship between entrepreneurship and financial health?

Entrepreneur households are less likely to be Black, single, or retirement age.

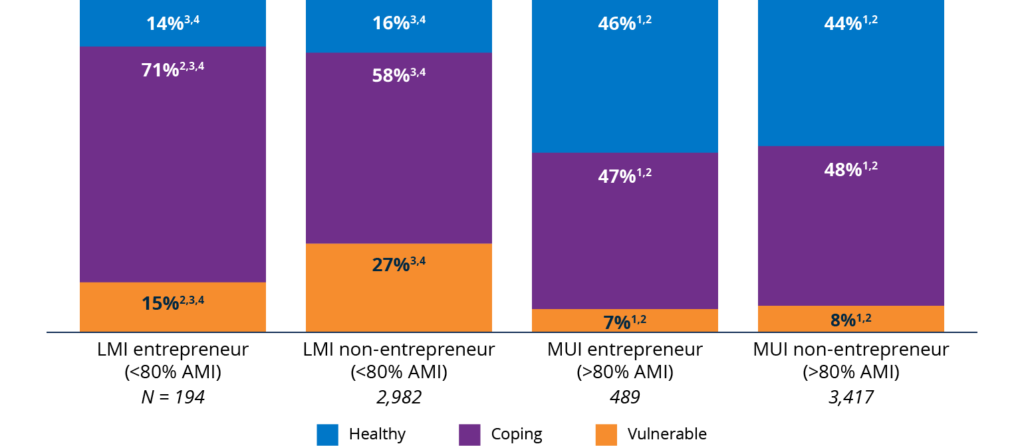

LMI entrepreneurs are far less Financially Healthy than MUI entrepreneurs.

Both LMI and MUI entrepreneurs have complex finances, often with volatile incomes from multiple sources.

LMI non-entrepreneurs are struggling even more than LMI entrepreneurs.

Data Spotlight

LMI entrepreneurs are financially healthier than LMI non-entrepreneurs, but still lag behind MUI households.

Percentage in each financial health tier, by entrepreneur status and income.

Note: Financial Health Pulse Survey 2024 data. Percentage points may not sum to 100% due to rounding. AMI is defined as the median household income for that household’s Metropolitan Statistical Area (MSA) or county. Percentage points may not sum to 100% due to rounding.

1 Statistically significant compared to LMI entrepreneur households at p<0.05.

2 Statistically significant compared to LMI non-entrepreneur households at p<0.05.

3 Statistically significant compared to MUI entrepreneur households at p<0.05.

4 Statistically significant compared to MUI non-entrepreneur households at p<0.05.

Our Funder

The Financial Health Pulse is supported by the Principal Foundation. The findings, interpretations, and conclusions expressed in this piece are those of the Financial Health Network and do not necessarily represent those of our funders or partners.

![]()

Pulse Points: Financial Health Differences Among Entrepreneurs

Explore the trends. Discover new insights. Build stronger strategies.