Workplace Financial Health Innovation: Rolling Out an Earned Wage Access Program for Your Employees

Employers, benefits platforms, regulators, and employees are paying more attention to earned wage access (EWA) products for their potential to improve employee financial health. Employers can maximize the positive outcomes of EWA products by minimizing associated fees, explaining the program mechanics to employees, and providing a complementary suite of financial resources.

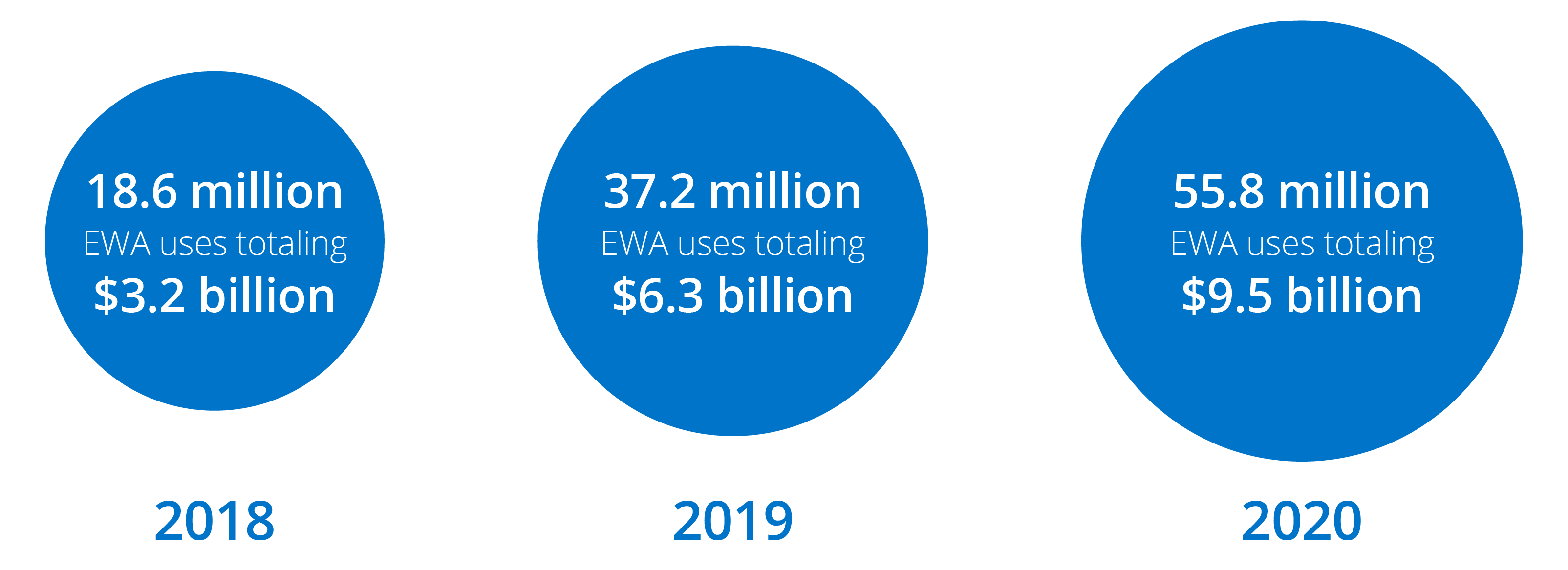

EWA Product Usage, 2018-20

EWA emerged as a financial product after the 2008 financial crisis. While fintech startups were first-to-market, payroll providers, employee benefits providers, and gig platforms have since started to incorporate the service and even launch their own versions.

Source: “Employer-Based Loans and Early Pay: Disruption Reaching Scale,” Aite-Novarica Group, 2019

Funding Access to Wages

Employees’ access to wages are usually funded through the EWA vendor – typically through capital on their balance sheet or use of a debt facility. Vendors use a payroll integration (if they do not already manage payroll) or secure timesheet data to verify the earnings that can be accessed through a user-facing application.

Disbursement

Employees can receive access to their wages in one of several ways: funds are sent to an employees’ linked direct deposit account through their employer, to a bank account the employee has set up with the EWA vendor, or to a prepaid or payroll card. Most EWA companies allow users to access 50%-100% of earned wages at a given time. Rules around accesses per pay period or per month and ability to take consecutive accesses vary by provider and by employer.

Payment to EWA Vendor

Wages accessed prior to payday are typically recouped from the users’ very next paycheck, usually meaning a repayment period of less than two weeks. EWA providers have at least a 97% recoupment rate; for those who may have difficulty repaying, some offer referrals to local resources to provide support.

Timing of Payments

Accesses are sent to an employee’s external bank account via direct deposit typically the next business day. Transfers to externally linked debit or prepaid cards can take up to 48 hours. Transfers can be made instant for a $1-$5 fee, depending on the vendor. Conversely, transfers can be instant and often are free for bank accounts or cards offered by EWA vendors.⁵

The Financial Solutions Lab (FSL) was established in 2014 to cultivate, support, and scale innovative ideas that help improve financial health. FSL focuses on solutions addressing acute and persistent financial health challenges faced by low- to moderate-income individuals, Black and Latinx communities, and other underserved consumers.

The Financial Health Network manages the Financial Solutions Lab in collaboration with founding partner JPMorgan Chase and with support from Prudential Financial.

The views and opinions expressed in the report are those of the authors and do not necessarily reflect the views and opinions of JPMorgan Chase & Co., Prudential Financial, or their affiliates.

Written by

-

Arjun KaushalSenior Associate, Innovation

Arjun KaushalSenior Associate, Innovation -

Vice President, Client Success and Business DevelopmentFinancial Health Network

Vice President, Client Success and Business DevelopmentFinancial Health Network -

Megan SkaggsAssociate, Innovation

Megan SkaggsAssociate, Innovation

Workplace Financial Health Innovation: Rolling Out an Earned Wage Access Program for Your Employees

Explore the trends. Discover new insights. Build stronger strategies.