The Financial Health and Material Hardships of Rural America

Financial insecurity and healthcare shortages weigh heavily on rural communities, a new Financial Health Pulse® analysis finds.

Rural Households Show Lower Financial Health, Savings, and Credit Access

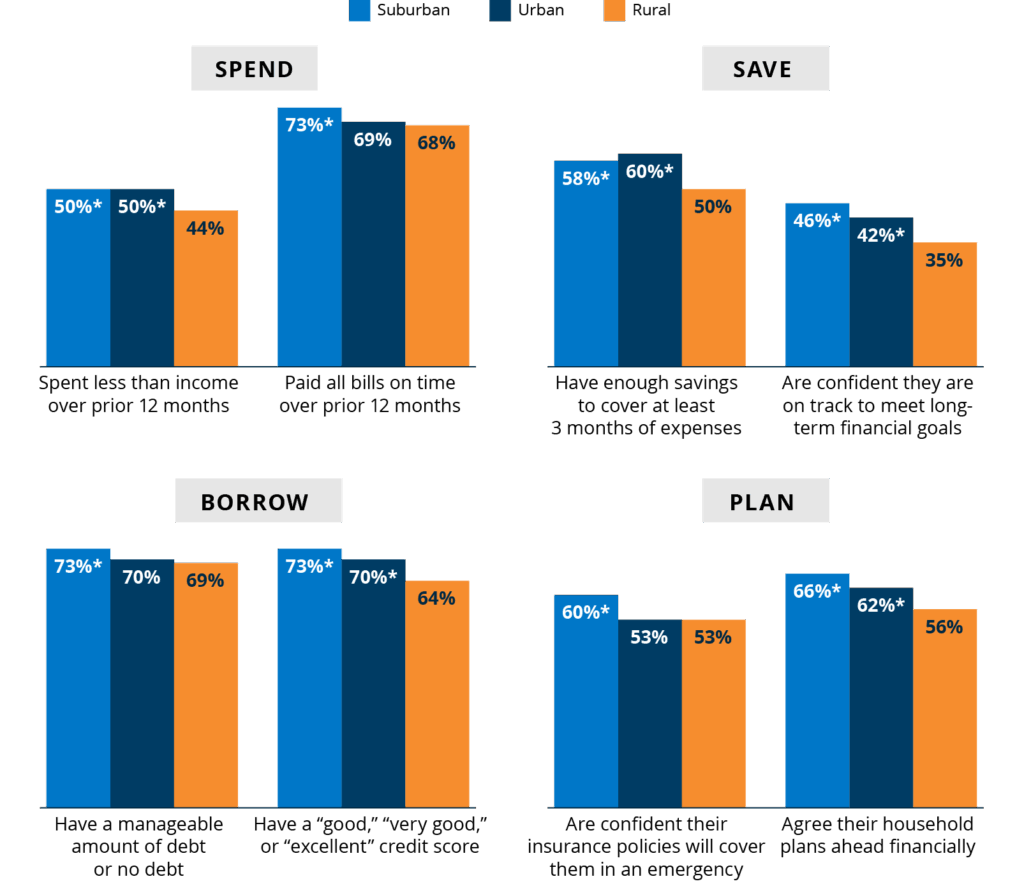

Only 25% of rural households are Financially Healthy, compared with 31% of urban households and 34% of suburban households.14 Rural households fare worse than both urban and suburban households on five of eight financial health indicators: spending relative to income, liquid savings levels, confidence in long-term financial goals, credit scores, and planning ahead financially (Figure 1). While rural and urban households report similar results on the remaining three indicators, rural households fare worse than their suburban counterparts across all eight indicators.

For example, only 50% of rural households report having enough savings to cover at least three months of living expenses, compared with 60% of urban households and 58% of suburban households. This gap is striking considering the lower average cost of living in rural areas, implying that many rural households remain vulnerable to income or expense shocks. Rural households also have lower credit scores than both urban and suburban households, suggesting they struggle to borrow affordably.

Figure 1. Rural households face financial health challenges, especially with saving and access to credit.

Financial health indicators, by urbanicity.

Notes: Data from 2025 Financial Health Pulse survey.

* Statistically significant relative to rural households (at p < 0.05)

Rural and urban households also report lower levels of confidence in their household’s insurance coverage than suburban households. Fifty-three percent of both rural and urban households are at least moderately confident their household’s insurance policies will cover them in an emergency, compared with 60% of suburban households (Figure 1). Part of this gap may be related to differences in health insurance coverage. About 11% of rural households report lacking health insurance, compared with 9% of suburban households and 10% of urban households.

Beyond insurance coverage and quality, a lack of proximity to healthcare services may also contribute to rural households’ lack of confidence in their insurance coverage. Between 2017 and 2024, 62 rural hospitals closed and only 10 opened.15 In August 2025, the Center for Healthcare Quality and Payment Reform estimated that 300 additional rural hospitals were at immediate risk of closing.16 Rural households face longer travel times to the hospitals that remain, where fewer services are offered.17

Material Hardships: Linking Financial and Physical Health Challenges

Financial health disparities, coupled with limited access to healthcare and other essential resources, can leave rural households more vulnerable to material hardships. Material hardships are examples of a household’s inability to meet its basic needs, including housing, utilities, food, and healthcare.

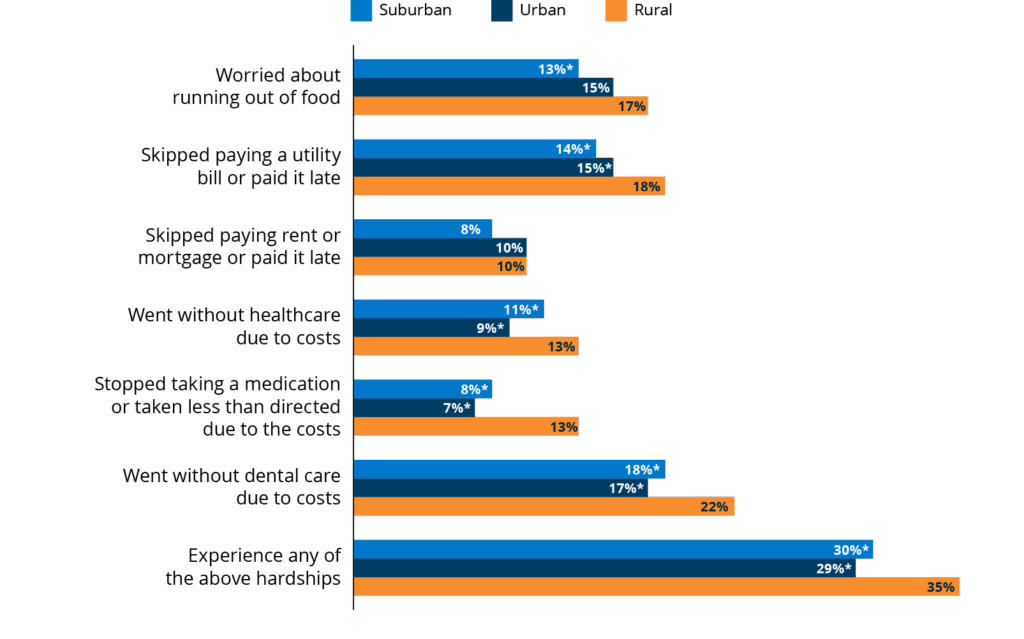

For example, rural households are more likely to report experiencing food insecurity over the past 12 months than suburban households. They are also more likely to skip or delay paying utility bills, forgo healthcare or dental care, and stop taking medication due to costs than both their urban and suburban counterparts (Figure 2).18 Overall, 35% of rural households experienced one or more material hardships in the past year, compared with 30% of suburban and 29% of urban households.

Figure 2. Rural households are more likely to report material hardships than urban or suburban households.

Percentage reporting material hardships in the past 12 months, by urbanicity.

Notes: Data from 2025 Financial Health Pulse survey.

* Statistically significant relative to rural households (at p < 0.05)

Hardships, especially those related to nutrition and skipped healthcare, can lead to worse physical health outcomes. Pulse data show 27% of people in rural areas report fair or poor overall health, compared with 20% of suburban and urban individuals.19 They are also more likely to have a disability themselves or live with someone with a disability (40% vs. 32% vs. 27%).20 Disabilities and health challenges can be expensive to manage, leading to a vicious cycle of health challenges exacerbating financial troubles and vice versa.

Altogether, these findings underscore the compounding impacts of financial strain and limited access to critical health infrastructure in rural communities.21

Acknowledgements

The Financial Health Pulse is supported by the Principal Foundation. The findings, interpretations, and conclusions expressed in this piece are those of the Financial Health Network and do not necessarily represent those of our funders or partners.

![]()