Once Financially Unhealthy, Always Financially Unhealthy?

A five-year analysis of Financial Health Pulse® research shows two critical ways that Americans struggle with financial health.

Key Findings

1. More than 4 out of 5 Americans were Financially Unhealthy for at least one year.

More than four-fifths (83%) of individuals were Financially Unhealthy at least once between 2018 and 2022 (see Figure 1). This is more than the 66% to 72% of Americans reported in annual estimates, suggesting that year-to-year reports of financial health do not fully capture how widespread and commonplace of an experience it is to be Financially Unhealthy.

Figure 1. Percentage of people who remained Financially Healthy versus people with Financially Unhealthy periods (2018-2022.)

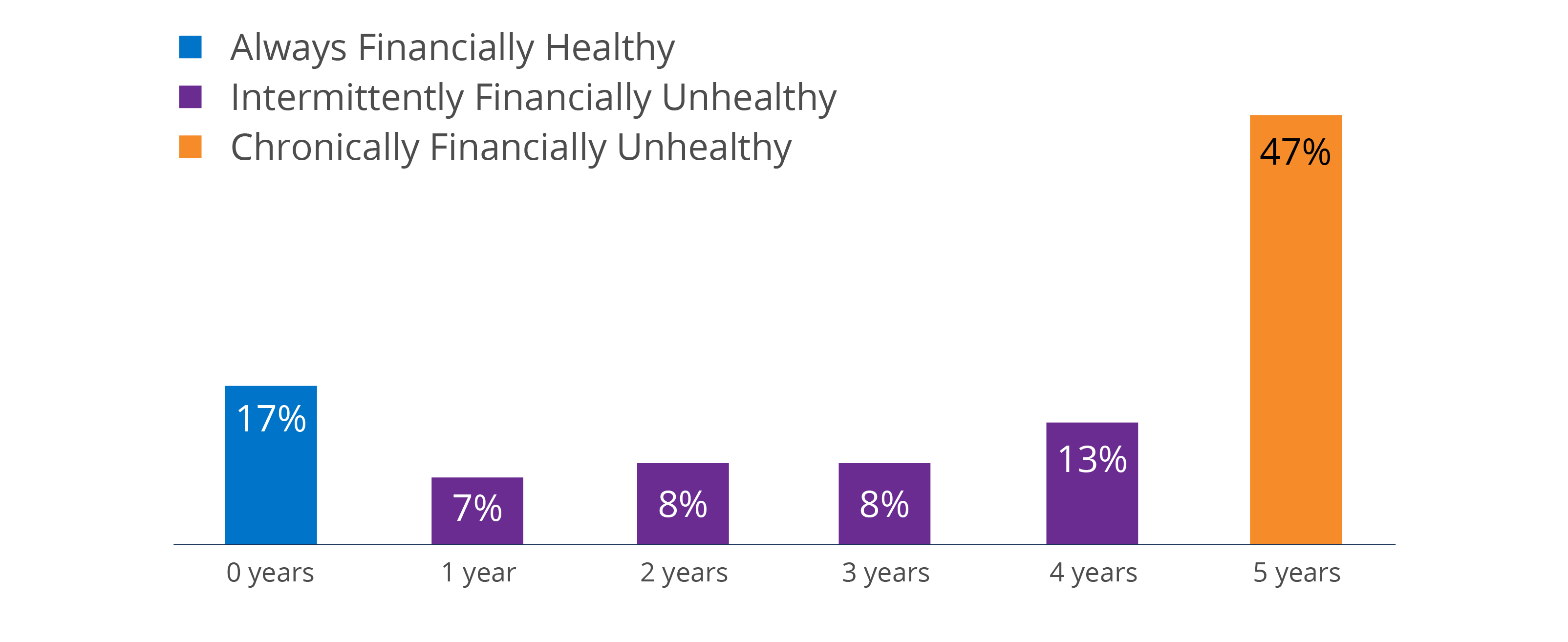

2. Being Financially Unhealthy is a temporary issue for some, but a chronic challenge for many others.

More than one-third of Americans (36%) were Financially Unhealthy for one to four years, meaning that they were Financially Unhealthy in some years but not others. In contrast, nearly half (47%) were Financially Unhealthy for at least five years (see Figure 2).11 This suggests that being Financially Unhealthy is experienced in two distinct ways: For one group, being Financially Unhealthy was a chronic situation lasting for at least five years; for another, it was intermittent – part of a cycle between being Financially Healthy and Unhealthy.12

Figure 2. Number of years people were Financially Unhealthy.

3. Certain demographic groups more frequently reported being chronically Financially Unhealthy, but this was not the case for being intermittently Financially Unhealthy.

Across race and ethnicity, household income, gender, education, and ability, there were larger and more significant disparities in being chronically Financially Unhealthy than in being intermittently Financially Unhealthy.13

Black and Latinx people (63% and 54%, respectively) more frequently faced chronic financial health challenges than White people (44%), although they were as frequently intermittently Financially Unhealthy as White people (see Figure 3). On the other hand, Asian people (21%) were less frequently intermittently Financially Unhealthy than White people (37%). The percentage of Asian people who were chronically Financially Unhealthy (54%) was also larger than the percentage of White people (44%), but this was not a statistically significant difference, largely due to the small sample size of chronically Financially Unhealthy Asian people.

About two-thirds of those with household incomes of $100,000 or more (66%) were either chronically or intermittently Financially Unhealthy. They were less frequently Financially Unhealthy on a chronic basis than people in any other income group. However, they were more frequently Financially Unhealthy on an intermittent basis than those with less than $30,000 in household income or those in the $30,000 to $59,999 income bracket.

More than half of women (55%) were chronically Financially Unhealthy, compared with 40% of men, but they were intermittently Financially Unhealthy as frequently as men (34% vs. 36%).14 Similarly, those without a bachelor’s degree (60%) were chronically Financially Unhealthy more frequently than those who held a bachelor’s degree (35%), but they were intermittently Financially Unhealthy as frequently. People with disabilities more frequently lacked financial health on a chronic basis (57%) than people without disabilities (44%), but there was little difference in the proportion of respondents who were intermittently Financially Unhealthy.

With respect to LGBTQIA+ status, we observe no differences in being either chronically or intermittently Financially Unhealthy. However, LGBTQIA+ people were less frequently Financially Healthy in all five years.

This suggests that members of certain demographic groups – those who are Black or Latinx; those with household incomes below $100,000; women; those without a bachelor’s degree; and those with a disability – are at a greater risk of being chronically Financially Unhealthy than their counterparts in other racial, income, gender, or education groups. In contrast, with a few exceptions, the risk of being intermittently Financially Unhealthy does not vary across demographic segments.

Figure 3. Financial health history by race and ethnicity, household income, gender, education, ability, and LGBTQIA+ status.

* Statistically significant difference relative to the reference category (p < 0.05); robust standard errors. † Reference category.

4. Specific life events are closely related to being chronically Financially Unhealthy.

While our data do not allow us to establish direct causality, this section endeavors to better understand life events that may be related to a chronic lapse in financial health. People who experienced some life events – such as being a homeowner, having a savings account, always being married or living with a partner, and having a retirement account – were less frequently Financially Unhealthy on a chronic basis (see Figure 4).

People who had other experiences – such as unemployment, having a major medical expense, providing a lower self-assessed physical and mental health rating, and having different types of debt – were associated with higher incidence of chronic financial challenges.15 In the case of credit card debt, those who had some years with debt were chronically Financially Unhealthy more often than those who never reported holding these types of debt. Those who reported auto loans or student loans every year were more often chronically Financially Unhealthy.16

Figure 4. Percentage of people who are chronically Financially Unhealthy, by life events experienced.

* Statistically significant difference relative to the reference category (p < 0.05); robust standard errors. † Reference category.

5. Similarly, certain life events are strongly associated with intermittent lack of financial health.

While the previous section considered how certain life events were related to a chronic lack of financial health, this section investigates whether similar life events are related to being intermittently Financially Unhealthy by focusing on people whose financial health changed between 2018 and 2022. Figure 5 displays the relationship between experiencing a certain life event and becoming Financially Unhealthy in the same year; the figure reflects these relationships among those who were intermittently Financially Unhealthy between 2018 and 2022 because this is the only group who experienced changes in their financial health. We present the results as a percentage change in the odds of becoming Financially Unhealthy when a life event is experienced. In Figure 5, values to the right of the center line can be interpreted as an increase in the odds of becoming Financially Unhealthy, and values to the left can be interpreted as a decrease in the odds of becoming Financially Unhealthy.

Some changes in people’s life circumstances were related to becoming Financially Unhealthy in the same year. Losing a job, for instance, is associated with more than a twofold (116%) increase in the odds of becoming Financially Unhealthy. A reduction in people’s self-assessed health is associated with a 69% increase in the odds of becoming Financially Unhealthy. Similarly, experiencing a major medical expense is associated with a 39% increase in the odds of becoming Financially Unhealthy.

On the other hand, some life events are associated with a reduced risk of becoming Financially Unhealthy. For instance, an increase in household income from less than $30,000 to an income of $30,000 or more coincides with reduced odds of becoming Financially Unhealthy by nearly half. Becoming a homeowner is also linked to a 37% reduction in the odds of becoming Financially Unhealthy. Moreover, paying off a mortgage, student loan debt, and credit card debt are associated with reduced odds of becoming Financially Unhealthy by 38%, 45%, and 46%, respectively. Finally, opening a savings account is associated with a 34% reduction in the odds of becoming Financially Unhealthy.

Figure 5. The percentage change in odds of becoming intermittently Financially Unhealthy

by life event experienced.

* Statistically significant difference relative to not experiencing the event (p < 0.05). Notes: Results are from a logistic regression with individual and time fixed effects. Household income was simplified into two categories to preserve cell sizes.