New analysis of 2020 Financial Health Pulse® data by BlackRock’s Emergency Savings Initiative shows that low- to moderate-income (LMI) frontline workers are less likely to be Financially Healthy than non-frontline workers, a reality that was likely exacerbated by the COVID-19 pandemic. To cope with the financial effects of the pandemic, LMI workers were more likely to draw down their savings and worry about depleting their savings.

Brief

On the Front Lines: How LMI Workers Coped During the COVID-19 Pandemic

Key Finding: Low- to moderate-income (LMI) frontline workers are less likely to be Financially Healthy than non-frontline LMI workers.

The Pandemic Likely Exacerbated Financial Challenges for LMI Frontline Workers

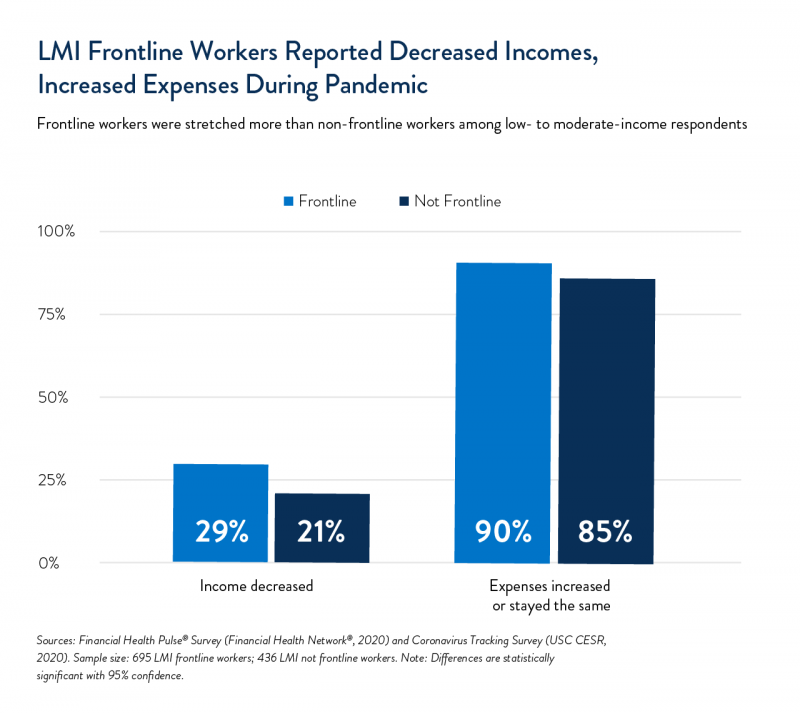

Although we are unable to analyze pre-pandemic comparisons of financial health between LMI frontline and non-frontline workers, we hypothesize that the pandemic may have exacerbated financial health disparities between these groups. During the pandemic, LMI frontline workers were more likely to say their income decreased and their expenses increased or stayed the same. Among LMI frontline workers, 29% reported that their incomes had fallen and 90% reported that their expenses had either increased or stayed the same, compared with 21% and 85% of non-LMI frontline workers, respectively.

Compared with LMI non-frontline workers, LMI frontline workers were more likely to be directly impacted by COVID-19 in their homes and workplaces, affecting both their incomes and expenses. Considering income first, LMI frontline workers were five times more likely (5%) than other LMI workers (1%) to report having someone in their household test positive for COVID-19 at the time of the survey. Beyond the health and emotional well-being effects of this difference, a positive COVID-19 case in the home may have prevented frontline workers from attending work, thus decreasing their income. Further, business closures during the pandemic – caused by frequent policy changes or staff members contracting COVID-19 – led to widespread disruptions in hours and wages for many LMI frontline workers.

Child care challenges during the pandemic also may have affected LMI frontline workers’ income and expenses. LMI frontline workers were more likely to have their work interrupted due to child care responsibilities than other LMI workers. Six percent of LMI frontline workers reported not being able to attend work due to child care and other responsibilities, compared with 1% of LMI non-frontline workers. This time off may have resulted in decreased income, just as child care expenses increased due to school closures and restricted social interactions with family members, who may have provided free child care pre-pandemic.

LMI Frontline Workers Ran Down Their Savings

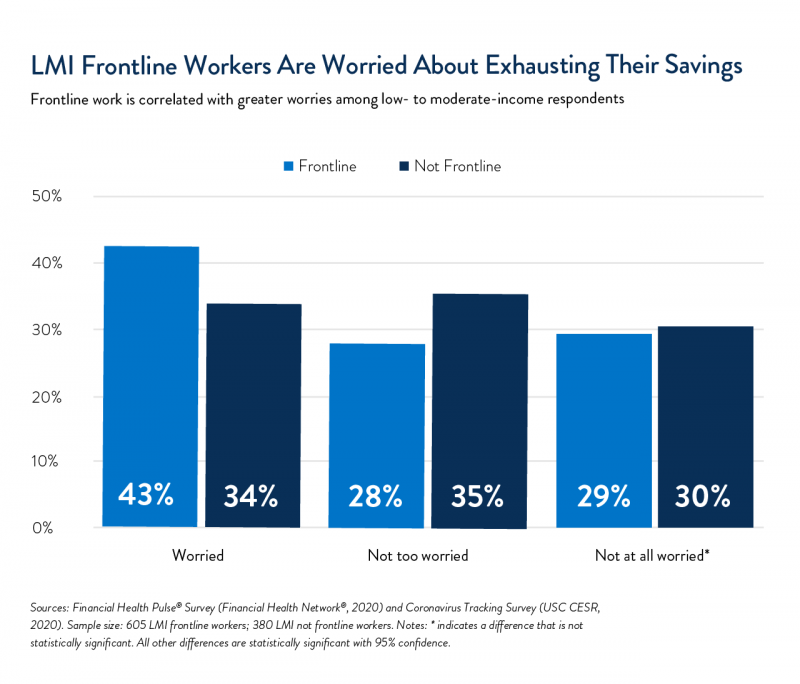

To cope with the financial effects of the pandemic, 29% of LMI frontline workers said they spent down their savings, compared with 23% of other LMI workers. This significant impact reduced the buffer workers had to protect themselves and their households from further emergencies. LMI workers were also more worried about the future: 43% of LMI frontline workers were “worried” or “very worried” that they would exhaust their savings, compared with 34% of LMI non-frontline workers. Despite these challenges, LMI frontline workers are doing their best to save at a similar rate (51%) to their non-frontline counterparts (52%), putting aside money for emergencies.

This emergency savings analysis was completed in partnership with Blackrock’s Emergency Savings Initiative

![]()