Understanding the Mental-Financial Health Connection

For the first time, we explore what’s known about the deep relationship between financial and mental health challenges – and what’s left to uncover.

Introduction

The post-COVID period has been marked by widespread economic uncertainty and persistent inflation that strain the finances of many families. Many Americans today are living under severe financial constraints, with 29% reporting that they are unable to pay all their bills on time and 29% reporting unmanageable levels of debt.7 In this volatile time, it is particularly important to understand the impact that such societal and financial uncertainty has on people’s well-being.

As the Financial Health Network works to create a movement that supports financial health for all, understanding the connectivity between financial and mental well-being is critical not only for raising awareness about the issues, but to also point to potential solutions. In this brief, we explore the existing knowledge base around the mental-financial well-being connection and identify potential next steps for research and interventions that could lead to greater, and more equitable, financial health.

This short brief represents our first paper on this topic, and it raises many important questions. The complex interplay between mental and financial well-being has implications for financial institutions, employers, policymakers, and many others. We look forward to future collaboration to better understand how to support people struggling financially – and ensure more people can thrive.

About Financial Health

Financial health, as measured by the Financial Health Network’s FinHealth Score®, provides a holistic way to understand one’s ability to manage their financial lives in the short and long term. Through eight survey questions centered on spending, saving, borrowing, and planning, the FinHealth Score helps categorize respondents into three financial health tiers: Financially Healthy, Financially Coping, and Financially Vulnerable (Figure 1).

Seven in 10 people in America are classified as Financially Coping (struggling with some aspects of their financial lives) or Financially Vulnerable (struggling with almost all aspects of their financial lives).

Figure 1. Interpreting FinHealth Scores.

Stress, Financial Hardship, and Mental Well-Being

For many in America, stress is a way of life. The American Psychological Association’s (APA) 2022 study of stress in America finds that about a third of adults (34%) report that stress is completely overwhelming most days.8 More than a quarter of adults (27%) said that most days they are so stressed they can’t function.9 The 2023 “State of the Global Workplace” poll by Gallup points to a similar story, finding record-high levels of employee stress.10

Finances represent one of the top stressors for many Americans – about two-thirds (66%) of those surveyed for the APA “Stress in America 2022” report said money was a significant source of stress.11 Stress related to money is at the highest level recorded since 2015.12

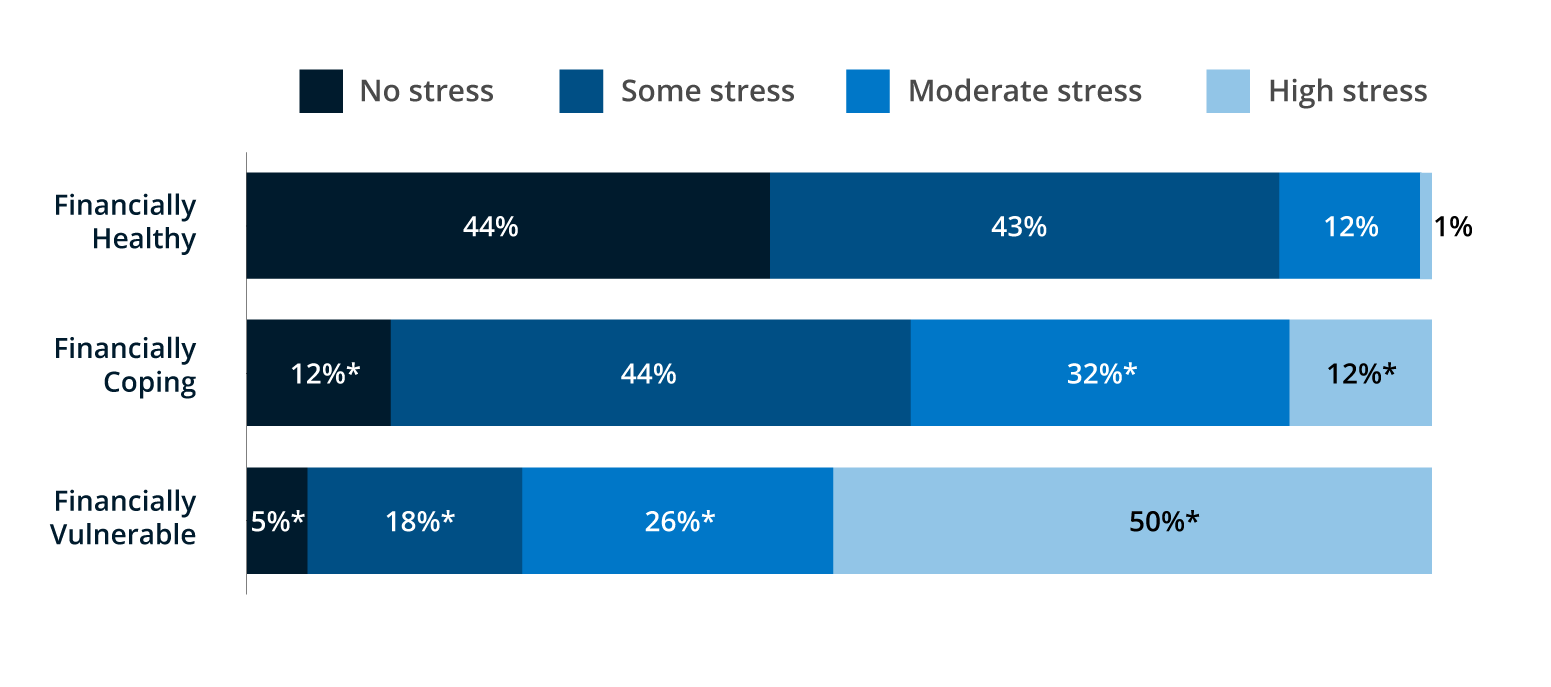

The prevalence of financial stress is perhaps not surprising, given that only about a third of people in America are considered Financially Healthy.13 Our own data from the Financial Health Pulse has consistently found that people who are financially struggling report greater levels of financial stress. In 2023, 76% of Financially Vulnerable people reported experiencing high or moderate stress from their finances, compared with just 13% of Financially Healthy people (Figure 2).

Figure 2. Financially Vulnerable people report dramatically higher levels of financial stress compared with Financially Healthy people.

Level of financial stress, by financial health tier.

Note: * Statistically significant at p < 0.05 vs. Financially Healthy.

Stress Is Not Distributed Evenly

Some populations appear to disproportionately report stress. These groups largely align with those who are more likely to also experience financial hardship, facing larger societal and structural barriers to financial health.14 For example, in addition to lower-income households, women, younger individuals, unmarried people, unemployed people, and renters have been found to disproportionately experience psychological stress of any kind, in particular financial stress.15, 16, 17

Findings by race and ethnicity appear nuanced. One study found that while people of color generally reported more stress than White people, these differences were no longer significant after controlling for other demographic factors.18 Another study on financial anxiety and stress found that, controlling for other demographic variables, Black and Hispanic adults are less likely than their White peers to feel financially anxious.19 Research has yet to establish a consensus on the moderating role of race in experiencing stress.

Limited data is available on people who are lesbian, gay, bisexual, transgender, queer, intersex, and agender (LGBTQIA+). Notably, however, the “Stress in America 2022” study found that members of the LGBTQIA+ community were more likely than those who are not to report that, most days, their stress is completely overwhelming (50% versus 33%, respectively).20

Financial Hardship and Mental Health

At the same time, the research is clear: financial hardship is associated with mental health challenges, such as heightened symptoms of anxiety and depression.21, 22, 23, 24 Numerous studies find that participants with low household incomes report greater incidence of psychological distress than those with higher incomes.25, 26 One study found that those with the lowest incomes in a community are 1.5 to 3 times more likely to experience common mental illnesses than the wealthiest within the same community.27 Another found that cash flow challenges (defined as the inability to meet regular bills on time) and deprivation (the inability to provide the essentials of life) were both associated with mental health problems.28

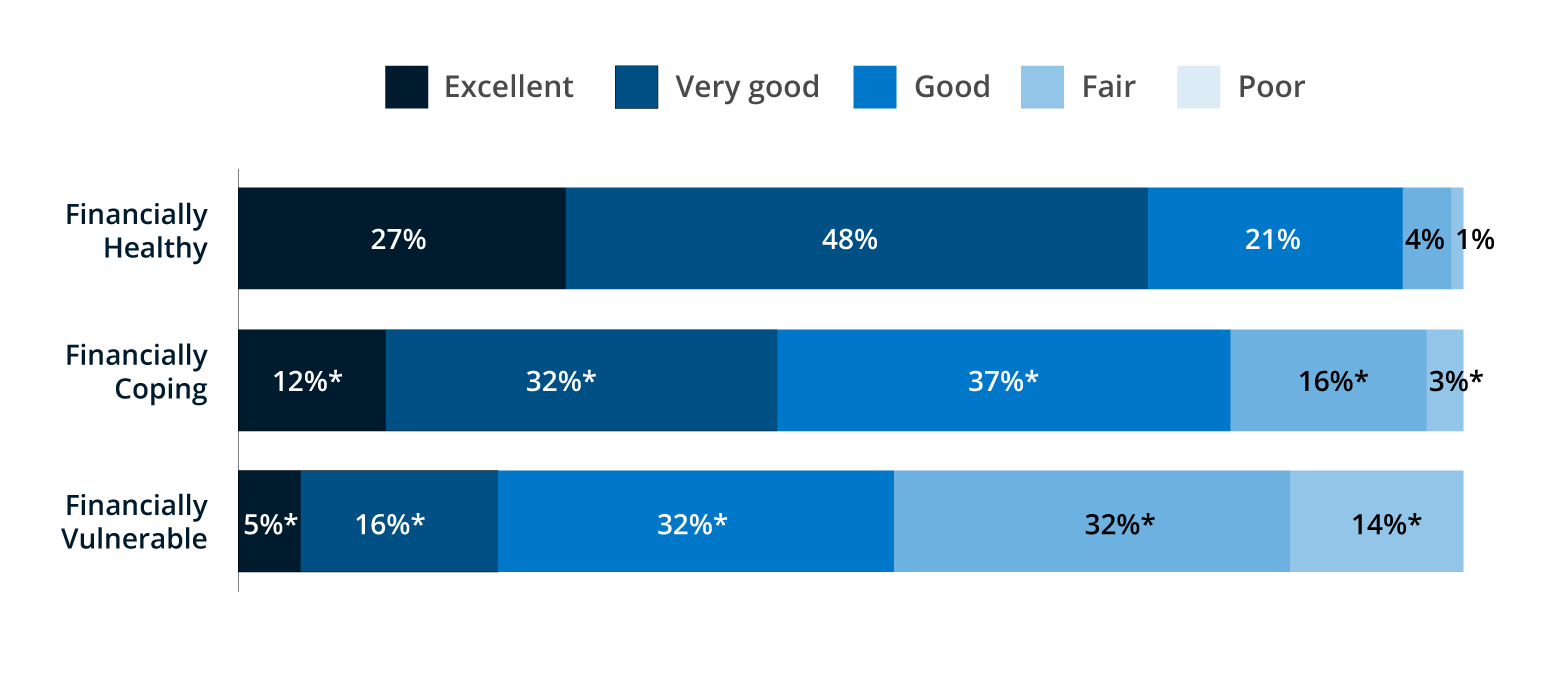

Again, our Financial Health Pulse data corroborate these findings. People who are Financially Coping or Vulnerable report significantly lower levels of mental well-being. Seventy-five percent of Financially Healthy individuals say that their mental well-being is “excellent” or “very good,” compared with 44% of the Financially Coping and just 21% of the Financially Vulnerable (Figure 3).

Figure 3. Financially Healthy people say that their mental well-being is “excellent” or “very good” at far higher rates than those who are Financially Coping or Vulnerable.

Self-reported mental well-being, on a scale from poor to excellent, by financial health tier.

Note: * Statistically significant at p < 0.05 vs. Financially Healthy.

Acknowledgements

We are grateful for the insights and feedback from many Financial Health Network colleagues, including Matt Bahl, Lisa Berdie, Necati Celik, Kennan Cepa, Wanjira Chege, Angela Fontes, Heidi Johnson, David Silberman, and Andrew Warren.

This report was developed with support from Bread Financial. The insights and opinions expressed in this report are those of the Financial Health Network and do not necessarily represent the views or opinions of our partners, funders, and supporters.

![]()

Written by

-

Policy & Research Advisor

Policy & Research Advisor -

Senior Associate, Workplace Solutions

Senior Associate, Workplace Solutions