Pulse Points Fall 2022: Responses to Record-High Gas Prices

As gasoline prices reach all-time peaks, how are Americans adjusting their buying patterns to cope? Analysis of Financial Health Pulse® survey and transactional data suggests that increasing gas costs and consumers’ financial health status may affect how often they refuel and how much they spend per trip to the pump.

Charting Gas Spending Over Time

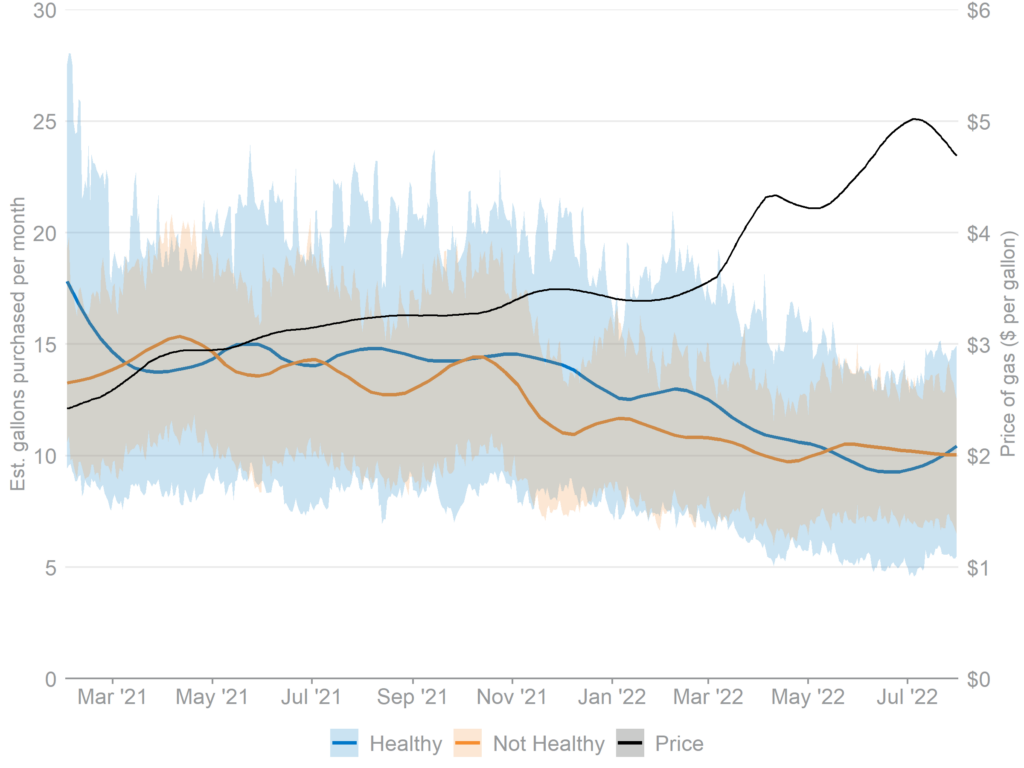

Total gas consumption in our sample decreased steadily overall as prices rose from February 2021 through July 2022 (Figure 1). The downward trend was similar for both Financially Healthy people and Financially Unhealthy people, and each group’s sensitivity to price over this period was statistically indistinguishable.5 This shows that both Financially Healthy people and Financially Unhealthy people in our sample reduced their gas consumption at similar rates as prices increased.

Figure 1. Gas consumption decreased overall as prices rose.

Daily average of monthly gas purchases (30-day rolling total, in gallons) and 30-day rolling national average retail gas price.

Notes: Shaded areas are 95% confidence intervals plotted around the mean activity estimated on each day. Lines have LOESS smoothing applied as a visual aid. n = 353 people observed on each day (125 Healthy, 228 Not Healthy).

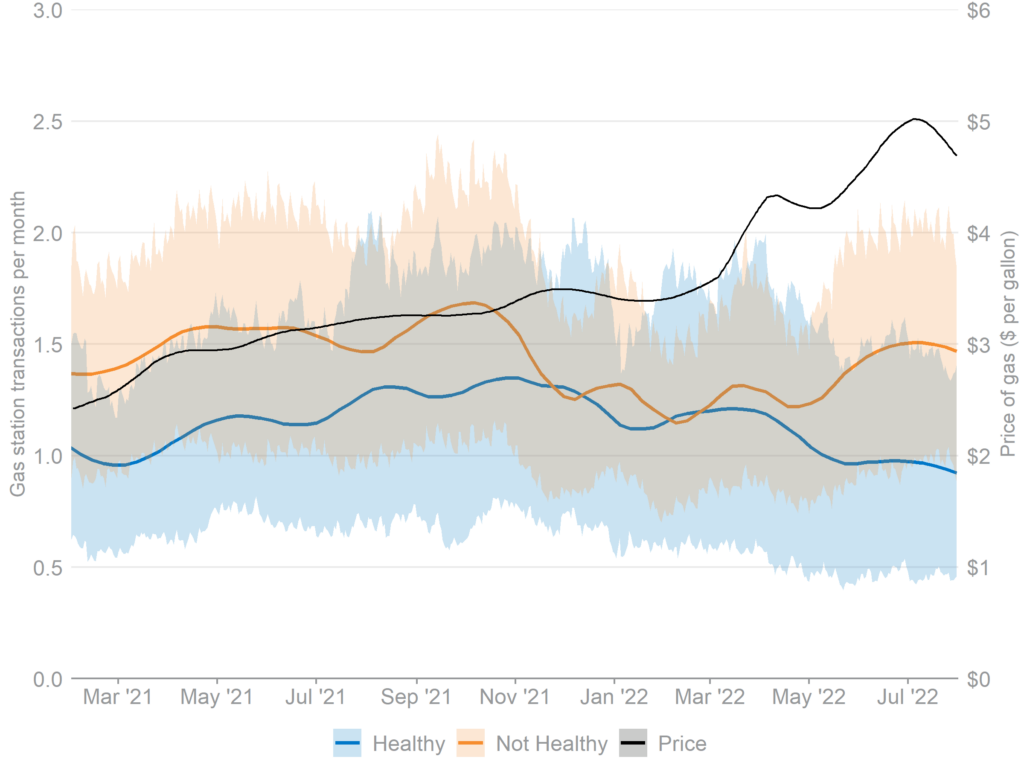

Despite a steady decline in the amount of gas purchased, there were no dramatic changes in frequency of gas station visits in our sample overall (Figure 2). However, each group’s trend in number of trips to the pump per month after March 2022 suggests that when gas prices began their steepest climb, people who are not Financially Healthy may have begun increasing their number of monthly gas refills relative to Financially Healthy people.6

Figure 2. Frequency of gas station purchases by financial health tier may have started to diverge in March 2022.

Daily average of monthly gas station transactions (30-day rolling total) and 30-day rolling national average retail gas price.

Notes: Shaded areas are 95% confidence intervals plotted around the mean activity estimated on each day. Lines have LOESS smoothing applied as a visual aid. n = 353 people observed on each day (125 Healthy, 228 Not Healthy).

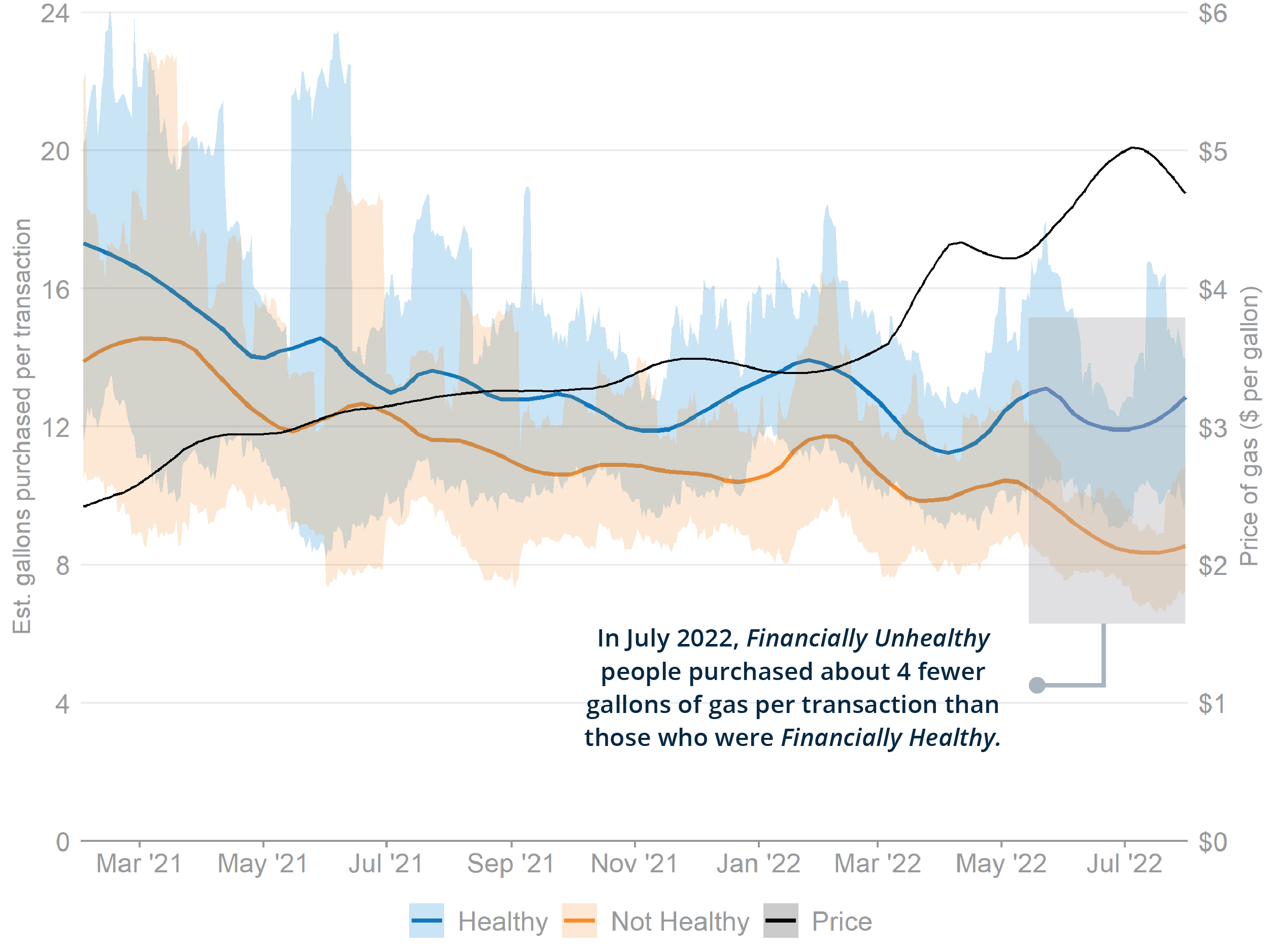

The estimated number of gallons of gas purchased per transaction (i.e., the average transaction size) may have also diverged between Financially Healthy and Unhealthy people. Figure 3 shows that during the period with the steepest price increases (March 1-July 31, 2022), the amount of gas purchased per transaction stayed roughly steady for Financially Healthy people and decreased slightly for Financially Unhealthy people in our sample. This is what we would expect to see if Financially Unhealthy people responded to price increases by purchasing gas in smaller increments. Together, these two visual trends suggest that people who are not Financially Healthy might have responded to increases in the price of gas not only by cutting back on the total amount of gas they purchased per month, but also by increasing the frequency and reducing the size of their purchases.

Figure 3. Financially Unhealthy people purchased smaller amounts of gas per transaction when gas prices were highest.

Daily average of estimated gallons of gas purchased per transaction and 30-day rolling national average retail gas price.

Notes: Shaded areas are 95% confidence intervals plotted around the mean activity estimated on each day. Lines have LOESS smoothing applied as a visual aid. n = 353 people observed on each day (125 Healthy, 228 Not Healthy).

Is Frequency of Refills Related to Price Increases?

Historical trends in the number of trips to the gas station and the amount purchased per trip offer clues to how gas purchases varied for each group over time, but other methods are needed to estimate the relationship between price and consumer behavior directly. Regression analysis allows us to model the relationship between price and transaction frequency for Financially Healthy and Unhealthy people to test whether each group responded to price increases differently at different price points.7

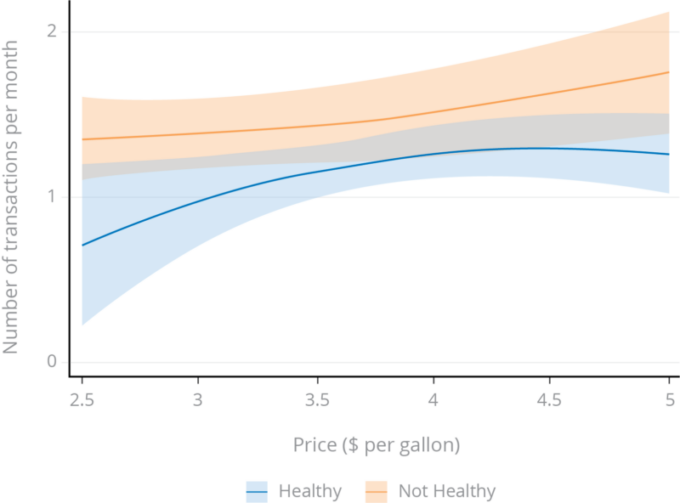

Our results show that each group’s predicted relationship between price and transaction frequency is distinct.8 This is true even after taking into account differences in overall gas consumption between the two groups and seasonal differences in demand for gas. Predictions from our regression model with these controls taken into account are plotted in Figure 4.

Overall, people in our sample increased the frequency of their gas station visits by about 0.18 transactions per month for every $1 price increase. Those who were not Financially Healthy increased their trips to gas stations when gas prices were very high, while those who were Financially Healthy maintained roughly the same number of trips to the pump per month once prices reached $4 per gallon. In other words, Financially Unhealthy people increased the frequency of their gas purchases relative to Financially Healthy people when gas prices were near $5 per gallon, holding total gas consumption constant.

Comparisons of the slopes of each model at different price points confirm that when gas prices were highest (between $4.50 and $5 per gallon), Financially Unhealthy people in our sample were increasing their number of purchases per month at a faster rate than Financially Healthy people (between 0.24 and 0.45 purchases per month faster for each $1.00 increase).9

Figure 4. When gas prices were very high, Financially Unhealthy people increased the frequency of their gas purchases relative to Financially Healthy people.

Estimates of transaction frequency by price, after controlling for total gas consumption and seasonality.

Notes: Plot shows predicted transactions per month for each group, produced by an OLS regression model with a quadratic term for price and controls for gallons purchased per month and monthly indicators to control for seasonality. n = 192,738 person-day observations. Standard errors clustered at the person level (n = 353). Shaded areas are 95% confidence intervals. Though confidence intervals overlap slightly, the estimated number of transactions per month are statistically significantly different at lower price points (~$2.50 to ~$3.25) and higher price points (~$4.50 to ~$5). Contrasts of marginal effects show that the slopes of each line are statistically significantly different between ~$4.50 and ~$5.

Written by

-

Manager, ResearchFinancial Health Network

Manager, ResearchFinancial Health Network