Beginning in the first quarter of 2024, the NCUA began requiring credit unions with over $1 billion in assets to include line items for overdraft and NSF fee revenue in their quarterly reports, aligning with the reporting requirements already in place for banks. Each credit union’s data was made publicly available. Notably, the NCUA has since reversed this decision and will no longer publish overdraft revenue data for individual credit unions beginning in 2025.6 Given this change, only one year’s worth of authoritative data for 445 credit unions will be available – providing an important snapshot of the fees charged across the market. While these credit unions represent only around 10% of credit unions nationwide, they collectively account for approximately three-quarters of credit union members and approximately 80% of the assets and deposits held by all credit unions as of the fourth quarter of 2024.7 (In contrast, the data the CFPB had collected in 2015, and on which it based its subsequent estimates, covered only six credit unions with assets above $1 billion.)

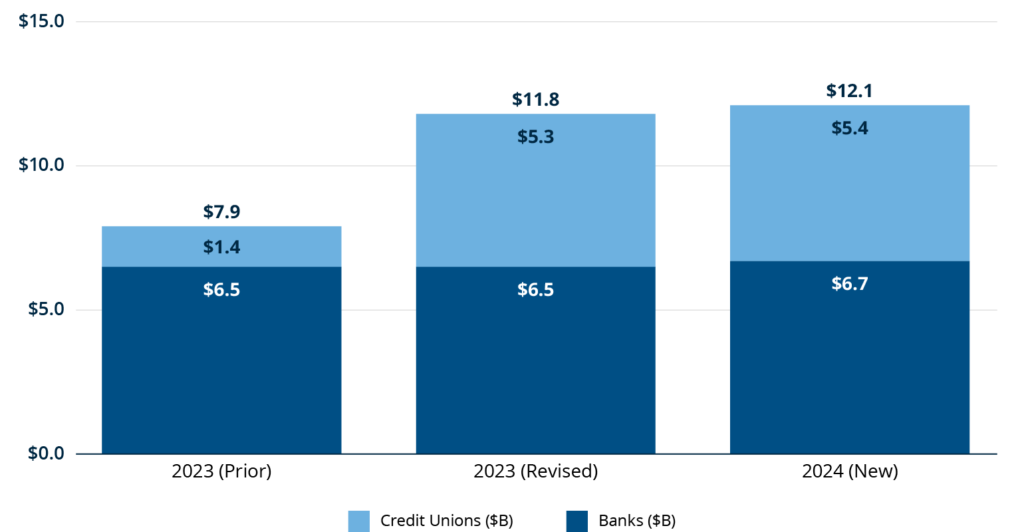

Drawing on these reports, the Financial Health Network has revised its estimate of the amount of overdraft and NSF fees consumers paid in 2023. We also used this data to estimate the amount they paid in 2024.8 As indicated in Figure 1, our prior estimates understated the total amount of overdraft and NSF fees by approximately $3.8 billion. Based on the newly available data, we now estimate the fees paid by credit union members in 2023 reflect 45% of total overdraft and NSF fees, rather than the 18% we previously estimated.9

The new data implies that the CFPB may have underestimated the share of overdraft and NSF fees attributable to credit unions in 2019. At the same time, the share of overdraft/NSF revenue attributable to credit unions since 2019 has likely increased, since between 2021 and 2023, most large banks either made significant reforms to how they charge overdraft or NSF fees or lowered their overdraft fees. Although some credit unions have taken similar steps – for example, BECU, the nation’s fifth largest credit union, lowered its overdraft fee to $10 in 2022 – credit unions have generally been slower to make changes. For instance, of the banks with over $10 billion in assets, almost two-thirds stopped charging NSF fees by the third quarter of 2023 – including 27 of the top 30 recipients of overdraft/NSF fees in 2021. In contrast, only 4 of the 20 credit unions with assets above $10 billion stopped charging NSF fees between 2021 and the third quarter of 2023.10

The Financial Health Network now estimates that in 2024, consumers of “very large financial institutions,” defined as banks and credit unions with over $10 billion in assets, paid $5.2 billion in overdraft fees. Of that amount, credit union members paid an estimated $735 million, or 14%.11 The overdraft rule the CFPB issued in December would cover these large financial institutions and require them either to lower their overdraft fees or to follow stricter guidelines for their overdraft programs.12