Financial Health Frontiers: Households Under Financial Pressure

The first brief of our Financial Health Frontiers Initiative takes a deeper look at the evolving financial lives of “middle-class” households and why their financial health depends on a holistic approach.

-

Program:

-

Category:

About Financial Health Frontiers

Supported by the Citi Foundation, Financial Health Frontiers is an ambitious initiative that aims to identify the needs, challenges, and opportunities for the next era of financial health. Guided by an Advisory Council of industry experts, business leaders, policymakers, advocates, and researchers from across the country, the Frontiers initiative asks: What are the trends that will most influence financial health over the next generation? How can we harness them for greater and more equitable financial health? Who is not at the table now but has a critical stake in the financial health movement?

In our initial publication, “Financial Health Frontiers: Shaping the Future of Financial Health,” we looked back at the evolution of the financial health field over the past 20 years, examined successes and challenges, and explored critical headwinds and tailwinds that will shape financial health in the years to come. This and forthcoming briefs explore opportunities to increase financial health broadly and equitably.

Introduction

The promise of joining the ranks of the “middle class” historically served as a beacon of hope to many Americans – offering a vision of financial security, if not wealth, and opportunity for the future. But today, earning a “middle-class” income no longer guarantees a comfortable lifestyle, a shift that has vast implications for the country’s economic future and social fabric. High costs for essentials like housing, healthcare, childcare, and education, to name just a few, make surviving – much less thriving – a challenge for many Americans.

This is not a new problem, but one that has been brewing for decades. Between 1990 and 2019, the median family’s income grew 140%, but the cost of childcare grew more than 200%, prescription drugs about 175%, and higher education almost 400%.1 At the same time, the ranks of the middle class – as measured by income – have contracted amid an intensifying wealth gap and enduring racial and gender disparities.2, 3, 4

Moreover, even in the face of positive macroeconomic indicators, the high cost of living is creating deep barriers to economic mobility and contributing to pessimism about the future.5, 6 Far beyond an individual or household issue, global research shows that this sort of malaise is contributing to continued polarization and potentially hampering broader economic growth.7, 8, 9

Indeed, the dire state of Americans’ financial health – their ability to manage day-to-day expenses, be resilient to shocks, and pursue future goals – should present a call to action for policymakers, community leaders, and businesses alike, no matter their politics or ideology. These issues span sectors – and like financial health itself, the solutions must also be holistic, requiring collaborative and cross-sectoral partnerships and innovations. In this brief, we detail how the cumulative effect of high prices across a range of expenses is straining the budgets of families, connect this reality to the decades-long hollowing out of America’s middle class, and ask:

Is greater and more equitable financial health possible? How can we cross sectors and ideologies to restore the middle-class promise?

Financial Health: Building Holistic Security

The challenges in affording day-to-day expenses and the inability to build for the future are encapsulated in the country’s anemic financial health – a holistic concept that refers to people’s ability to spend, save, borrow, and plan in ways that allow them to be secure and pursue opportunities. Year after year, only about one-third of Americans are considered “financially healthy,” with deep fissures by gender, race, and disability.10

By going beyond narrow concepts like household income or credit score, financial health acknowledges that numerous factors intersect to contribute to a family’s ability to thrive. It’s an outcome shaped by place, class, race, gender, history, opportunity, and many other factors – some mutable, some not. It is a concept that reflects one’s ability not only to make ends meet in the here and now but also to protect against shocks and make progress toward long-term goals. In many ways, being financially healthy encapsulates a vision for middle-class security.

Today, the majority of Americans are not financially healthy, with expenses outpacing income, little wiggle room to protect against financial shocks, and diminished hope for the future. No amount of scrupulous budgeting and meticulous planning can overcome math that simply doesn’t add up.

A Struggling Middle Class, No Matter the Definition

The concept of class has a deep history and is often used to highlight differences in social and economic strata. In contemporary discourse, the “middle class” is often emphasized as both a benchmark for stable household finances and standards of living.11 Different ways to define the middle class all attempt to capture the various social, cultural, and economic resources people draw upon. Regardless of the definition, it appears that the middle class is increasingly squeezed.

One way to measure the middle class is by household income, though ranges vary.12, 13, 14 Pew Research Center, for example, defines the middle class as households earning between two-thirds and twice the national median income, or $67,819 to $203,458 (in 2022 dollars) for a family of four.15 By this metric, about 50% of adults are in middle-class households, a figure which has declined steadily over the past five decades.16 Moreover, the incomes of middle-class households have risen slower than those of upper-income households.17

Other evocative definitions are sometimes used for the middle class, all of which show how the designation is increasingly out of reach. For example, a White House Task Force on the Middle Class convened by the Obama Administration provided an enduring and aspirational definition of the middle class: one’s ability to achieve common goals, like home and car ownership, college education for children, health and retirement security, and occasional family vacations.18 But today, only half of those nearing retirement age have any retirement savings, and homeownership is affordable with the median income in only a handful of metropolitan areas in the country.19, 20

A recent Washington Post study leveraged even more basic lifestyle elements as a barometer for the middle class. These closely echo the Financial Health Network’s definition of financial health: having the capacity to pay all bills on time without worry, savings for the future, resources to afford an unexpected $1,000 expense without going into debt, appropriate and adequate insurance, and the security to retire comfortably. But even with this modest set of criteria, just 35% of the population qualifies as “middle class.”21

Case Studies: ‘Middle Class’ in Income Alone

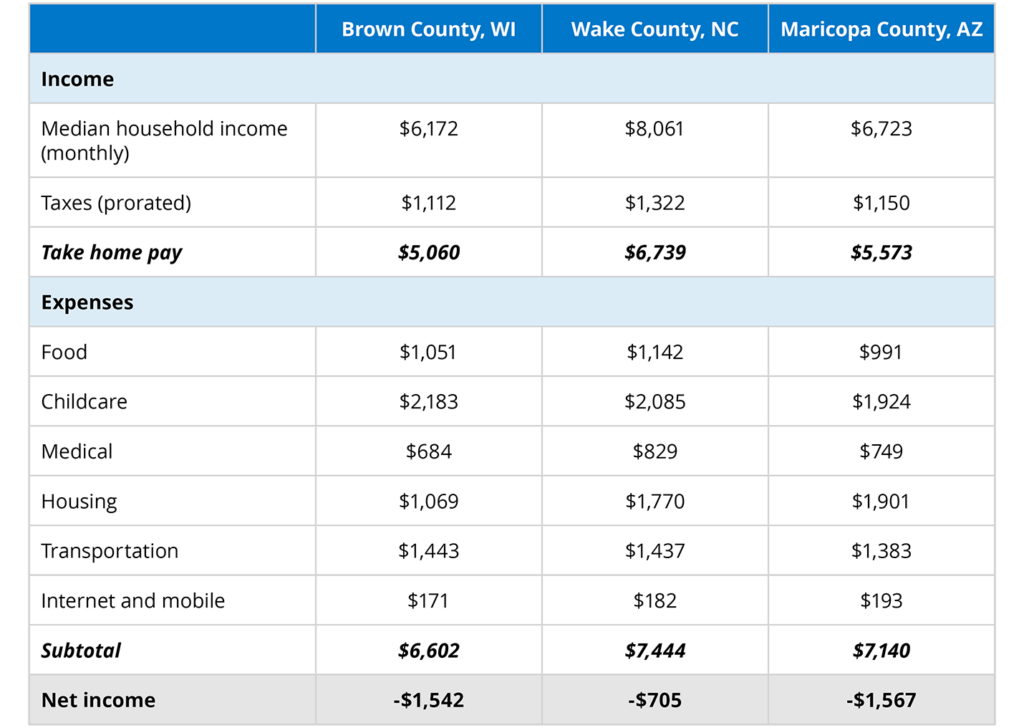

Why is the middle class struggling? It’s helpful to take a closer look at household budgets to understand. Take a few hypothetical families with two adults and two school-age kids living across the country in Brown County, WI, Wake County, NC, and Maricopa County, AZ. These counties represent a range of geographies, rural/urban divides, ideologies, and demographics, yet their residents are confronting a shared challenge of making ends meet.

The median household income in each of these locations ranges from $74,066 to $96,734 – roughly at or above the national median and well over the poverty rate for a family of four.22, 23 One might assume, then, that earning the median household income would be sufficient to get by – indeed, many would consider it a solidly “middle-class” income.

A look at a typical family’s budget, however, demonstrates that the math doesn’t add up. Even meeting basic needs alone – housing, medical care, childcare, transportation, food, and internet – is not feasible, leaving the family with a negative net income.

Table 1. Just a few expense categories eat up the entire income of a household.

Median household income compared with select typical expenses for a family of 4.

Notes: Median household income from US Census. Taxes and expenses estimated by MIT Living Wage Project for a family of four with two working adults.

It’s important to stress that no single issue impacts families’ abilities to get by – it’s the combined impact of a range of financial pressures. In this environment, the standard budgeting heuristic of 50% needs, 30% wants and 20% savings is inapplicable. There’s not enough for needs, much less wants or savings.

Moreover, these issues aren’t unique to the places profiled but reflect a pattern in communities of all sizes across the country. While we have used the median income for each county as a simple measure to demonstrate that even basic expenses surpass income, this figure hides much variability. For example, while the median household income nationally was $74,580 in 2022, the figure was $81,423 for white, non-Hispanic-headed households, $64,936 for Latine-headed households, and just $50,901 for Black households.26 For households headed by women of all races with no spouse present the figure is $47,107.27

As the middle class struggles, the gap between the country’s wealthiest and poorest is a gulf. Today, the richest 10% of households have $6.9 million in household wealth on average, holding 67% of total household wealth. In contrast, the bottom 50% have $51,000 on average, holding just 2.5% of total household wealth.28 Black and Latine families hold pennies on the dollar compared with white families’ wealth.29, 30

A Closer Look at Budgets Under Pressure

As Table 1 demonstrates, families’ financial struggles are a result not of one issue alone, but a compounding set of challenges:

Housing:

In recent years, housing costs have outpaced income growth, creating budget crunches both for renters and owners.31 Fully half (50%) of renters are “cost burdened,” which means they spend more than 30% of income on rent and utilities, with Latine and Black renters particularly likely to be cost-burdened.32 Utility costs and home insurance premiums have also been on the rise, a trend that is likely to continue with the warming climate.33, 34

Healthcare and Medical:

The Kaiser Family Foundation consistently finds that healthcare is cited as a key financial challenge for American households, and the growth in health costs has far outpaced inflation.35, 36 Not infrequently, families elect to forgo health care in order to make ends meet.37 These issues are particularly acute for people with disabilities, many of whom live on very low incomes. The Financial Health Network has found that a third (32%) of people with disabilities say they had skipped needed medical care due to cost, a choice that could have deep reverberations for overall health.38

Childcare:

For many families, childcare has now surpassed rent as the most costly monthly expense.39 The Department of Labor found that the annual cost of childcare for one child ranged from $5,357 to $17,171, even as most childcare workers earn low wages.40, 41, 42 As costs rise, many families are left to choose between career and family, a decision that disproportionately affects the financial well-being of women.43

Internet and Mobile:

Inequitable access to broadband can impact education and job access, with significant financial health implications. Twenty-two percent of Americans in rural areas and 28% of those in Tribal lands lack coverage, compared with just 1.5% in urban areas.44 Broadband coverage is also critical for financial service access; 15 million consumers live in online banking deserts, without reliable or high-speed internet.45

Food:

The cost of groceries is perpetually on many families’ minds, and with good reason. Research from Feeding America shows that in 2022, 13.5% of all people and 18.5% of children were food-insecure, with rates even higher among communities of color.46

Transportation:

Gas prices impact household spending and behavior, and financially vulnerable households face tradeoffs about how much to spend at the pump.47 Beyond the price of gas, transportation prices add up for many families. A survey by SaverLife and the FINRA Foundation of SaverLife’s low-and moderate-income clients found that nearly one-third (32%) spent a quarter or more of their monthly income on transportation.48

More Than Individual Budgets at Risk

These cost-of-living pressures are doing more than straining individual households’ budgets – they are contributing to a lack of economic mobility. The Harvard-based research center Opportunity Insights has found that 90% of children born in 1940 ultimately earned more than their parents. The same is true of only half of those born in 1980.49 Again, the racial divides are vast: in 99% of neighborhoods, Black boys earned less in adulthood than white boys who grew up in families with comparable income, indicating that many kids of color do not have access to the same pathways to economic outcomes as their white peers.50

Today, Americans feel a deep pessimism about the future. In a poll that predated the pandemic, about three-quarters of people (73%) believed that the gap between the rich and the poor would grow in the coming decades, and half of the public said children in 2050 will have a worse standard of living than they do today.51 And the implications could be even more dire: as income distribution becomes increasingly unequal, many researchers have hypothesized that it is a contributing factor to the uneasy politics of the moment, with deep polarization and little optimism.52, 53

Financial Health: Bridging Differences To Advance Financial Health for All

Financial health is core to our economy and our collective perspective on the future, but more than that, it is central to a collective American identity. Yet, it has become increasingly clear that financial opportunity and prosperity are out of reach for so many, with barriers particularly entrenched for some people and places.

Financial health should be front and center in the conversation about America’s future, no matter one’s politics or ideology. Indeed, the financial health challenges the vast majority of Americans face – making ends meet, saving for the future, and creating security for their families – are challenges shared by both sides of the aisle, with profound implications for future generations. In a divided country, financial health for all is a holistic goal that we can share, bringing us together to influence public policy and shape our collective efforts.

We propose that financial health be central to efforts to improve Americans’ economic opportunity, build quality of life, and dismantle historical barriers. We suggest several core focus areas for this endeavor:

Measurement, Evaluation, and Research

We manage what we measure, which is why it’s critical that we understand the state of financial health across the country. The Financial Health Network and others recognize that traditional economic measures – gross domestic product (GDP), the consumer price index (CPI), and the aggregate unemployment rate – do not fully capture the true state of families’ finances.54 And now, multiple actors across public and private sectors are already changing how they assess financial health. For example, the Treasury Department is developing a Financial Inclusion Strategy with measurement at the fore.55 State and local measurements – for use by stakeholders in various institutions and sectors – provide deep and tailored insights.56

Measurement, and the research it supports, is a first step to demonstrating “what works” and building the knowledge base. This, in turn, is essential to build solutions for the middle class across industries and sectors. Research initiatives could include analyses of how community and place-based factors, like housing supply, labor markets, environmental risks, and educational investments, shape opportunities for financial health and the middle class. Equally helpful could be evaluations of public policies that are targeted at making a difference in household and community economic well-being and the risks of not building the middle class.

Innovation

We must continue to explore new solutions that address the challenges families face in making ends meet. Part of innovation involves deeply understanding the financial realities that people are facing. Shedding light on the pain points that consumers are experiencing is a necessary first step to innovation: we must better understand the realities and choices that families are facing, with a particular focus on how different communities experience the barriers to a middle-class lifestyle.

Innovators could look at the big expenses that many American families face – childcare, housing, transportation – and think about both the challenges and the unconventional opportunities that these issues might bring. Innovations could and should address both affordability and also asset and wealth-building, making meaningful progress on both sides of a household’s balance sheet. Families and households face intersecting challenges; solutions likewise need to address these intersections. In particular, we hope that new solutions are relevant for, responsive to, and built by the communities for whom the middle class has been kept out of reach.

The holistic nature of the problem should guide how institutions and organizations develop solutions. Take, as examples, the work of several Financial Health Frontiers Advisory Council members:

-

- Engaging Employers in the Housing Crisis: The National Urban League is increasing access to homeownership for Black households by conducting housing fairs with employers. This practice encourages employers to reflect on their wages; identify opportunities to provide homeownership stipends; and better understand housing as central to workforce objectives like diversity, career advancement, and employee retention.

- Uniting Financial Services and Health Systems for Overall Health: The National Credit Union Foundation has created a model for credit unions and healthcare systems to work together to address the interconnected nature of financial and physical health. Their work shows that credit unions, healthcare providers, and public health leaders can collaborate to lessen the financial stress of patients and build a more holistic continuum of care that addresses people’s overall health, with a particular focus on cancer patients.57

- Connecting Nonprofits, Trainers, and Employers To Advance Financial Health: The Business Roundtable develops partnerships between community-based organizations, training and education providers, and businesses to strengthen employers as key levers to promote financial health. One salient effort focuses on a network of large companies and partnerships to improve employment opportunities for individuals with criminal records. Another effort focuses on supporting companies to ensure that there are pathways to hiring and promotion for Americans without college degrees, which helps companies expand the number of qualified applicants and extends economic opportunity more broadly, including to underrepresented groups.58

Collaboration

Broadening financial health and building the middle class is a massive endeavor, requiring collaboration and cooperation that crosses sectors and puts aside politics for the entire country’s well-being. Indeed, innovative solutions to the problems outlined in this brief are and should be inherently collaborative.

A litany of actors – from businesses to community-based organizations to government agencies to policymakers working in sectors like housing, education, transportation, finance, and healthcare to name a few – play a role in improving financial health and building the middle class. There is no single actor who can measure, innovate, or solve this challenge alone. We all must work together and holistically to take bold steps to build America’s middle class and bolster financial health for all.

We’d love to hear from you and explore opportunities for collaboration across sectors and industries. To engage with Financial Health Frontiers and stay up to date about financial health in the U.S., please also sign up for our newsletter at finhealthnetwork.org/programs/financial-health-frontiers.

Acknowledgments

Financial Health Frontiers is grateful to the visionary members of its Advisory Council for their input and guidance:

Naomi Camper, Chief Policy Officer, American Bankers Association

Kelvin Chen, Senior EVP and Head of Policy, Consumer Bankers Association

David Clunie, Principal and Head of Community Relations, Edward Jones

Dr. Tamarah Duperval-Brownlee, Chief Health Officer, Accenture

Anne Evens, CEO, Elevate

Maria Flynn, President & CEO, Jobs for the Future

Jonay Foster Holkins, Founder, Trendline Strategies LLC

Abby Hughes Holsclaw, Senior Director, Asset Funders Network

Gigi Hyland, Executive Director, National Credit Union Foundation

Gary Koenig, Vice President, Financial Security, AARP Public Policy Institute

Laura MacCleery, Senior Director, Policy & Advocacy, UnidosUS

Racheal Meiers, Senior Director, Community and Social Health, Kaiser Permanente

Harold Pettigrew, President & CEO, Opportunity Finance Network

Leigh Phillips, President & CEO, SaverLife

Nasir Qadree, Founder and Managing Partner, Zeal Capital Partners

Ida Rademacher, Vice President and Co-Executive Director, Financial Security Program, Aspen Institute

Cy Richardson, Senior Vice President for Programs, National Urban League

Kareem Saleh, Founder & CEO, FairPlay AI

Kristen Scheyder, Senior Vice President, Citi Foundation

John Soroushian, Senior AI Advisor, FinRegLab

Jennifer Tescher, President and Chief Executive Officer, Financial Health Network

Erin White, Senior Director, Corporate Initiatives, Business Roundtable

Thank you to the many Financial Health Network staff who supported the creation of this publication.

The Financial Health Frontiers initiative is supported by the Citi Foundation.

![]()

The findings, interpretations, and conclusions in this piece are those of the Financial Health Network and do not necessarily represent those of our funders or Advisory Council members.

- “The Cost of Living in America: Helping Families Move Ahead,” The White House Council of Economic Advisers, August 2021.

- “How the American Middle Class Has Changed in the Past Five Decades,” Pew, September 2022.

- Economists debate the extent to which wealth inequality has grown depending on what data and assumptions are included in the analysis of tax data, arguably the most complete source to measure household wealth. See: Thomas Piketty, Emmanuel Saez, & Gabriel Zucman, “Distributional National Accounts: Methods and Estimates for the United States,” The Quarterly Journal of Economics, May 2018, and Gerald Auten & David Splinter, “Income Inequality in the United States: Using Tax Data to Measure Long-Term Trends,” Journal of Political Economy, September 2023.

- Ana Hernández Kent & Lowell R. Ricketts, “The State of U.S. Wealth Inequality,” Federal Reserve Bank of St. Louis, August 2024.

- Kim Parker, Rich Morin, & Juliana Menasce Horowitz, “Looking to the Future, Public Sees an America in Decline on Many Fronts,” Pew Research Center, March 2019.

- Rogé Karma, “The U.S. Economy Reaches Superstar Status,” The Atlantic, June 2024.

- Yangfeng Gu & Zhongyuan Wang, “Income Inequality and Global Political Polarization: The Economic Origin of Political Polarization in the World,” Journal of Chinese Political Science, November 2023.

- Nolan McCarty, Keith T. Poole, & Howard Rosenthal, “Polarized America: The dance of ideology and unequal riches,” MIT Press, January 2008.

- Jonathan D. Ostry, Andrew Berg, & Charalambos G. Tsangarides, “Redistribution, Inequality, and Growth,” International Monetary Fund Staff Discussion Note, February 2014.

- Andrew Warren, Wanjira Chege, Kennan Cepa, & Necati Celik, “Financial Health Pulse® 2024 U.S. Trends Report: Diverging Financial Health Indicators,” Financial Health Network, September 2024.

- Alyssa Fowers, Emily Guskin, & Scott Clement, “How Americans define a middle class lifestyle – and why they can’t reach it,” The Washington Post, February 2024.

- Richard V. Reeves, Katherine Guyot, & Eleanor Krause, “A dozen ways to be middle class,” The Brookings Institution, May 2018.

- Richard V. Reeves, Katherine Guyot, & Eleanor Krause, “Defining the middle class: Cash, credentials, or culture?” The Brookings Institution, May 2018.

- Ben Horowitz, “Defining ‘low- and moderate-income’ and ‘assessment area’,” Federal Reserve Bank of Minneapolis, March 2018.

- Alyssa Fowers, Emily Guskin, & Scott Clement, “How Americans define a middle class lifestyle – and why they can’t reach it,” The Washington Post, February 2024.

- “How the American Middle Class Has Changed in the Past Five Decades,” The Pew Charitable Trusts, September 2022.

- Rakesh Kochhar, “The State of the American Middle Class,” Pew Research Center, May 2024.

- “Annual Report of the White House Task Force on the Middle Class,” The Obama White House, February 2010.

- Brittany King, “Women More Likely than Men to Have No Retirement Savings,” United States Census Bureau, January 2022.

- “Home Ownership Affordability Monitor,” Federal Reserve Bank of Atlanta, July 2024.

- Alyssa Fowers, Emily Guskin, & Scott Clement, “How Americans define a middle class lifestyle – and why they can’t reach it,” The Washington Post, February 2024.

- The national median household income was $75,149 in 2022. The median household income for Brown County, WI is $74,066; for Wake County, NC is $96,734; and for Maricopa County AZ is $80,675. These data reflect the ACS 5-year estimates, which we chose to use given that we are examining data at the county level. See: “QuickFacts,” United States Census Bureau.

- “2023 Poverty Guidelines: 48 Contiguous States (all states except Alaska and Hawaii),” Office of the Assistant Secretary for Planning and Evaluation, U.S. Department of Health and Human Services, 2023.

- These estimates of income are from the American Community Survey 5-year estimates and is the median of all households, not solely families of four. See: “QuickFacts,” United States Census Bureau.

- There are different approaches to estimating household costs and expenses. The Living Wage Institute at MIT uses a number of data sources to derive estimates of local costs for these categories of basic needs. See: Amy K. Glasmeier, “What is a living wage and how is it estimated?” Massachusetts Institute of Technology, 2024.

- “Median Income in the Past 12 Months (in 2022 Inflation-Adjusted Dollars),” United States Census Bureau.

- Ibid.

- Ana Hernández Kent & Lowell R. Ricketts, “The State of U.S. Wealth Inequality,” Federal Reserve Bank of St. Louis, August 2024.

- Ibid.

- “Nine Charts about Wealth Inequality in America,” Urban Institute, April 2024.

- Alexander Hermann & Peyton Whitney, “Home Price-to-Income Ratio Reaches Record High,” Joint Center for Housing Studies of Harvard University, January 2024.

- “America’s Rental Housing,” Joint Center for Housing Studies of Harvard University, 2024.

- Madeleine Ngo & Ivan Penn, “As Utility Bills Rise, Low-Income Americans Struggle for Access to Clean Energy,” The New York Times, January 2024.

- Benjamin J. Keys & Philip Mulder, “Property Insurance and Disaster Risk: New Evidence from Mortgage Escrow Data,” National Bureau of Economic Research, June 2024.

- Lunna Lopes, Alex Montero, Marley Presiado, & Liz Hamel, “Americans’ Challenges with Health Care,” KFF, March 2024.

- “Average Family Premiums Rose 4% to $21,342 in 2020, Benchmark KFF Employer Health Benefit Survey Finds,” KFF, October 2020.

- Author’s analysis of 2023 Financial Health Pulse® data.

- Andrew Warren, Wanjira Chege, Meghan Green, & Lisa Berdie, “The Financial Health of People with Disabilities,” Financial Health Network, August 2023.

- Venessa Wong, “Child care costs more than a mortgage payment or rent almost everywhere in the U.S.: ‘There is no escaping it’,” MarketWatch, May 2024.

- 2018 data, adjusted to 2022 dollars.

- Liana Christin Landivar, Nikki L. Graf, & Giorleny Altamirano Rayo, “Childcare Prices in Local Areas,” U.S. Department of Labor, January 2023.

- Brooke LePage, “The Child Care and Early Learning Workforce Is Underpaid and Women are Paying the Price,” National Women’s Law Center, May 2023.

- Meghan Greene, Andrew Warren, & Jess McKay, “The Gender Gap in Financial Health,” Financial Health Network, July 2022.

- “2020 Broadband Deployment Report,” Federal Communications Commission, April 2020.

- Kennan Cepa, Wanjira Chege, & Necati Celik, “Pulse Points Spring 2024: Financial Health Challenges in Banking Deserts,” Financial Health Network, May 2024.

- Approximately 23% of Black individuals and 21% of Latine individuals were food insecure in 2022. See: “Map the Meal Gap 2024,” Feeding America, May 2024.

- Andrew Warren, “Pulse Points Fall 2022: Responses to Record-High Gas Prices,” Financial Health Network, December 2022.

- “Changing lanes: How transportation costs intersect with the financial and life opportunities of people living on low-to-moderate incomes,” SaverLife & FINRA Foundation, August 2023.

- “The American Dream is Fading: Only half of children today grow up to earn more than their parents,” Opportunity Insights.

- Raj Chetty, Nathaniel Hendren, Maggie Jones, & Sonya R. Porter, “Race and Economic Opportunity in the United States: An Intergenerational Perspective,” Opportunity Insights, December 2019.

- Kim Parker, Rich Morin, & Juliana Menasce Horowitz, “Looking to the Future, Public Sees an America in Decline on Many Fronts,” Pew Research Center, March 2019.

- Yangfeng Gu & Zhongyuan Wang, “Income Inequality and Global Political Polarization: The Economic Origin of Political Polarization in the World,” Journal of Chinese Political Science, November 2023.

- Nolan McCarty, Keith T. Poole, & Howard Rosenthal, “Polarized America: The dance of ideology and unequal riches,” MIT Press, 2008.

- Jennifer Tescher & David Silberman, “Measuring the financial health of Americans,” The Brookings Institution, May 2021.

- “Request for Information on Financial Inclusion,” Department of the Treasury, December 2023.

- For example, Financial Health Network partnered with The Chicago Community Trust to understand how families in Chicago and Cook County were faring financially. This is directly impacting the work that local leaders are doing to build more equitable financial health across the city. See: Necati Celik, Ph.D., Meghan Greene, Wanjira Chege, & Angela Fontes, Ph.D., “Financial Health Pulse® 2022 Chicago Report,” Financial Health Network, January 2023, and Carmelo Barbaro, Sylvia I. Garcia, & Tina Tchen, “Closing Chicago’s Financial Health Divide,” Financial Health Network, June 2024.

- See The National Credit Union Foundation’s focus on collaborating to support cancer patients: “Side Effects™: The financial crisis of cancer hiding in plain sight and how credit unions can help,” The National Credit Union Foundation.

- See: “Corporate Initiatives,” Business Roundtable.

Written by

Financial Health Frontiers: Households Under Financial Pressure

Explore the trends. Discover new insights. Build stronger strategies.