Even as Inflation Declines, People in the U.S. Seek Ways To Cope

A recent Financial Health Pulse® survey finds half of people in the U.S. are using four or more strategies to cope with inflation, such as relying on charities or food banks.

In May 2023, the annual inflation rate was 4.1%, down from 8.5% one year prior. Yet despite declining inflation rates, many in the U.S. were still feeling the crunch. Previous studies show that the American public continues to be concerned about inflation, but there has been little investigation into how they are adjusting their finances to cope with inflation-related price increases.

According to data collected from April through June of 2023 by the Financial Health Network as part of its Financial Health Pulse® study, 90% of people reported using at least one of 11 specific coping strategies in the last year to deal with the impact of recent price increases.

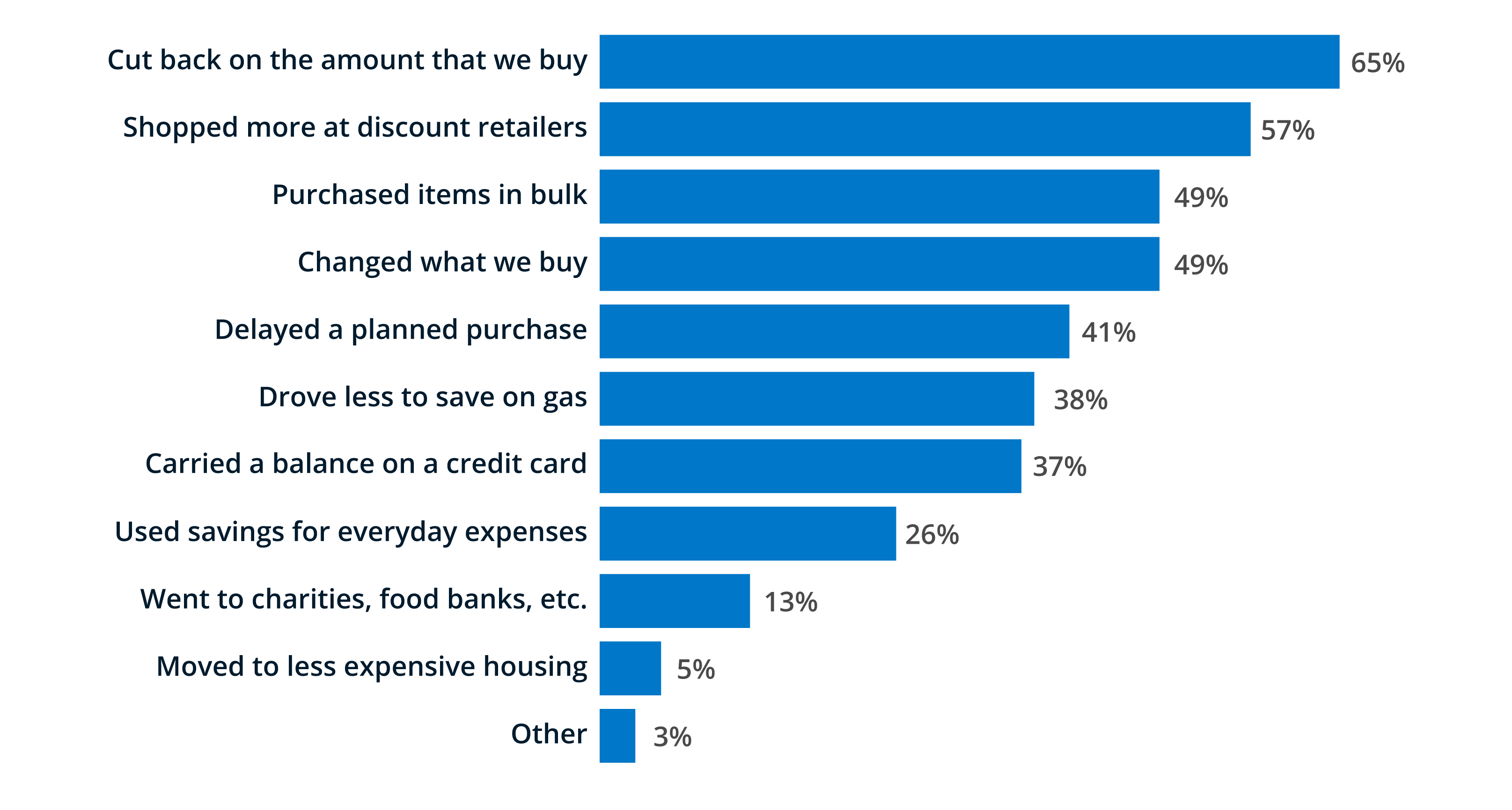

Out of nearly a dozen different coping strategies, the most commonly reported strategies involved people shifting where, what, and how they purchased goods. Some of the most commonly used coping strategies included cutting back on the amount they buy, shopping more at discount retailers, purchasing items in bulk, and changing what they buy.

Figure 1. People most often changed their shopping behavior to cope with price increases.

Percentage who reported each coping strategy.

Note: Data from the 2023 Financial Health Pulse® survey. N = 8,262 respondents who had a FinHealth Score® and responded to the question, “Have you or has anyone in your household taken any of the following actions in the last year to help you deal with the impact of these price increases? Please select all that apply.”

Those who were Financially Vulnerable, meaning they struggled with almost all aspects of their financial lives, reported using many of these coping strategies at a higher rate. Although coping strategies can generate slack in tight budgets, some may necessitate difficult trade-offs and have repercussions for well-being. For instance, more than 4 in 5 people who were Financially Vulnerable (84%) cut back on the amount they buy. And in some cases, this may have contributed to serious hardship. Among Financially Vulnerable people who cut back on the amount they buy, more than a third (37%) indicated that someone in their household had to forgo healthcare because they could not afford it.

Financially Vulnerable people sometimes turned to coping strategies that were less often used by others. Nearly half (48%) reported using their savings to pay for everyday expenses, over a third (36%) turned to charities or food banks, and 12% reported moving to less expensive housing. Black and Latinx people also more frequently reported using each of these strategies than White and Asian people.

“It is concerning to see the most vulnerable people having to make such difficult choices to deal with inflation. Dipping into savings and turning to charities and food banks may provide some slack in peoples’ budgets.”

Necati Celik

Not only were most people using a coping strategy, the typical American reported multiple coping strategies with half using four or more strategies in the last year.

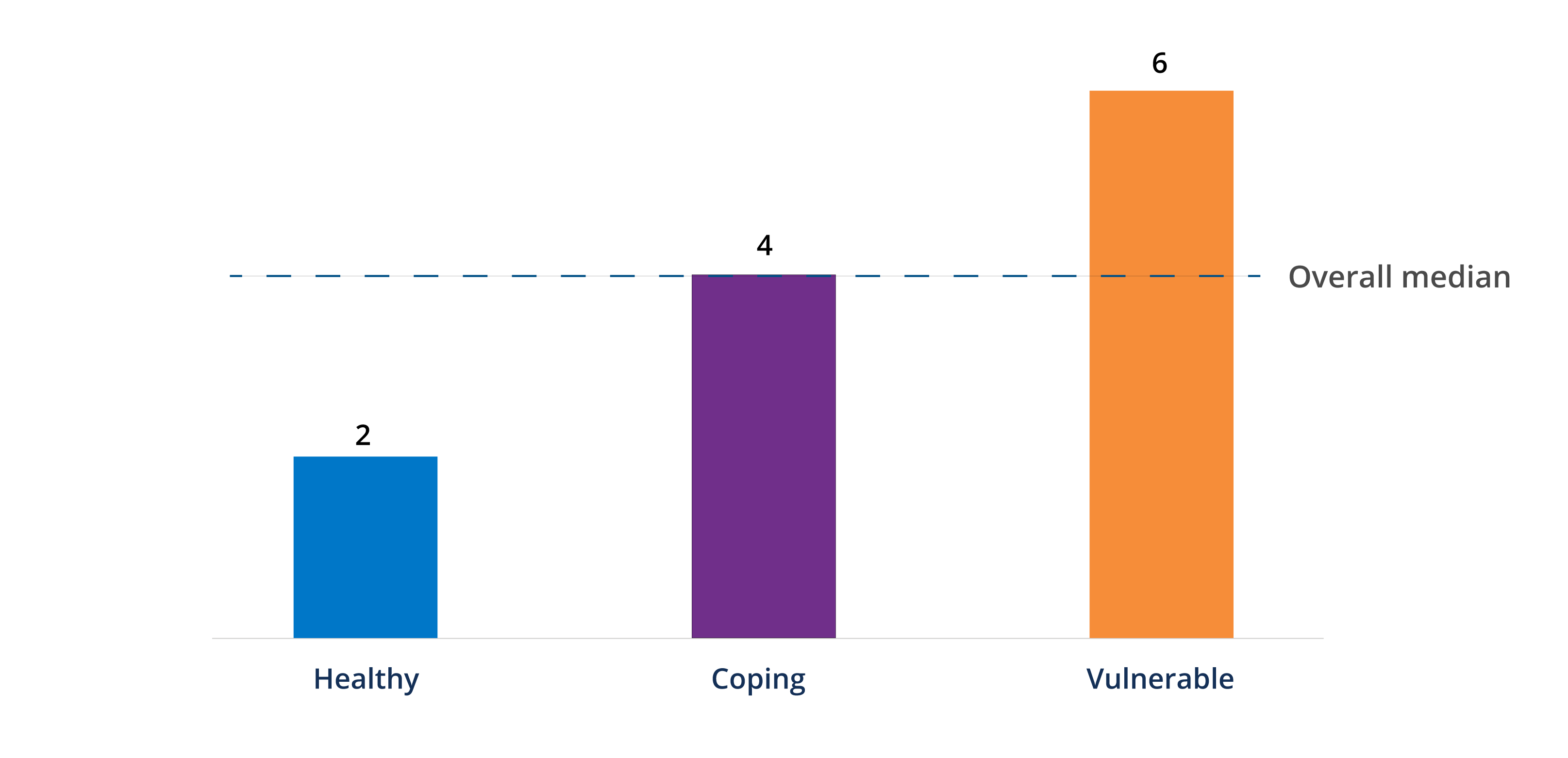

Moreover, those who were Financially Vulnerable relied on more strategies than others. Half of Financially Vulnerable people reported using six or more strategies in the last year. In contrast, half of Financially Healthy people, who are not struggling with any aspects of their finances, reported using just two or more. Financially Coping people, who are struggling with some, but not all, aspects of their finances, typically reported using four coping strategies.

Figure 2. Financially Vulnerable people used more coping strategies.

Median number of coping strategies reported, by financial health tier.

Note: Data from the 2023 Financial Health PulseⓇ survey. N = 8,262 respondents who had a FinHealth Score® and responded to the question, “Have you or has anyone in your household taken any of the following actions in the last year to help you deal with the impact of these price increases? Please select all that apply.” Statistics reported are the median number of coping strategies reported, out of the 11 choices offered on the questionnaire.

“Our findings show that the typical person in America is relying on a constellation of coping strategies to manage inflationary pressures, but that Financially Vulnerable people are needing to be especially resourceful in response to inflation. These pressures may have lasting consequences for their financial health, even as inflation slows.”

Andrew Warren

Acknowledgements

The Financial Health Pulse is supported by the Citi Foundation, with additional funding from the Principal Foundation. The findings, interpretations, and conclusions expressed in this piece are those of the Financial Health Network and do not necessarily represent those of our funders or partners.