By Thea Garon, Senior Director, Necati Celik, Associate and Andrew Dunn, Manager, Financial Health Network

Since mid-March, the United States has lost more than 21 million jobs amid the COVID-19 pandemic. In order to help people get by, the Treasury Department began distributing recovery rebates, or “stimulus payments,” on April 11 as part of the CARES Act. As the government debates the need for another stimulus package, new data from the U.S. Financial Health Pulse show that stimulus payments have provided a valuable lifeline to millions of people who lost their jobs during the crisis.

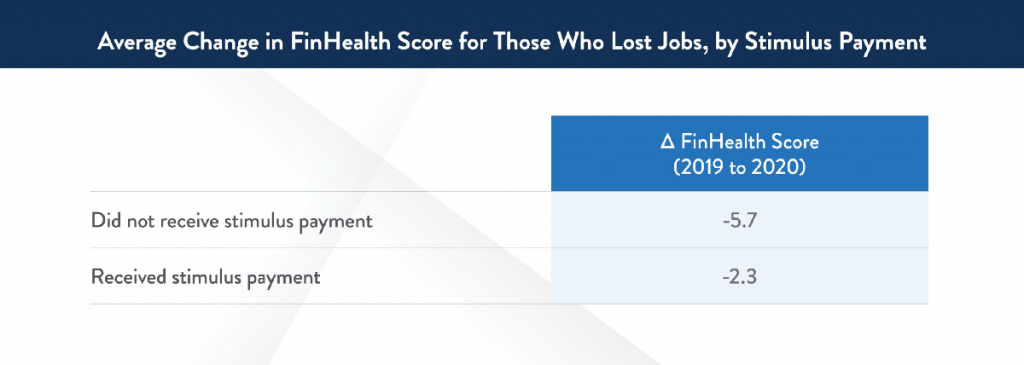

For this analysis, we used data from the 2019 and 2020 U.S. Financial Health Pulse surveys (administered in April and May of each year) to explore changes in financial health among the 341-person sample whose income decreased because of job loss from COVID-19. Within this sample, we compare the 56% of people who had received a stimulus payment by the time the survey was completed (May 7) with the 38% of people who had not received a stimulus payment by that date (an additional 6% of respondents were not sure if they had received a stimulus payment). We use the FinHealth Score®, a metric that assesses respondents’ financial health on a scale from 0–100, to measure financial health.

Our research shows that receiving a stimulus payment appears to help people weather the negative consequences of losing a job because of COVID-19. On average, those who lost their jobs and did not receive a stimulus payment experienced a 5.7 point decrease in their FinHealth Scores, while those who lost their jobs and did receive a stimulus payment experienced a 2.3 point decrease in FinHealth Scores. In other words, people who did not receive a stimulus payment experienced a decline in their financial health that was 2.5 times larger than those who did receive a stimulus payment. (See endnotes for more information on the research methodology.)

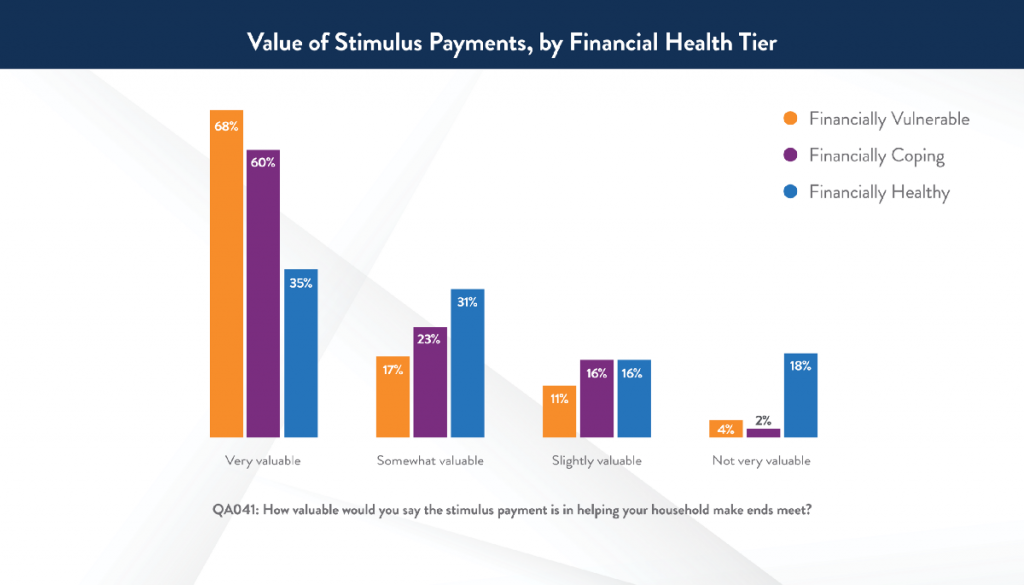

More importantly, it appears that stimulus payments may be most valuable to those who are least financially healthy. Among all people who received a stimulus payment (not just those who lost a job), more than two-thirds (68%) of Financially Vulnerable respondents said the stimulus payments were “very” valuable, compared with 60% of Financially Coping respondents and just 35% of Financially Healthy respondents.

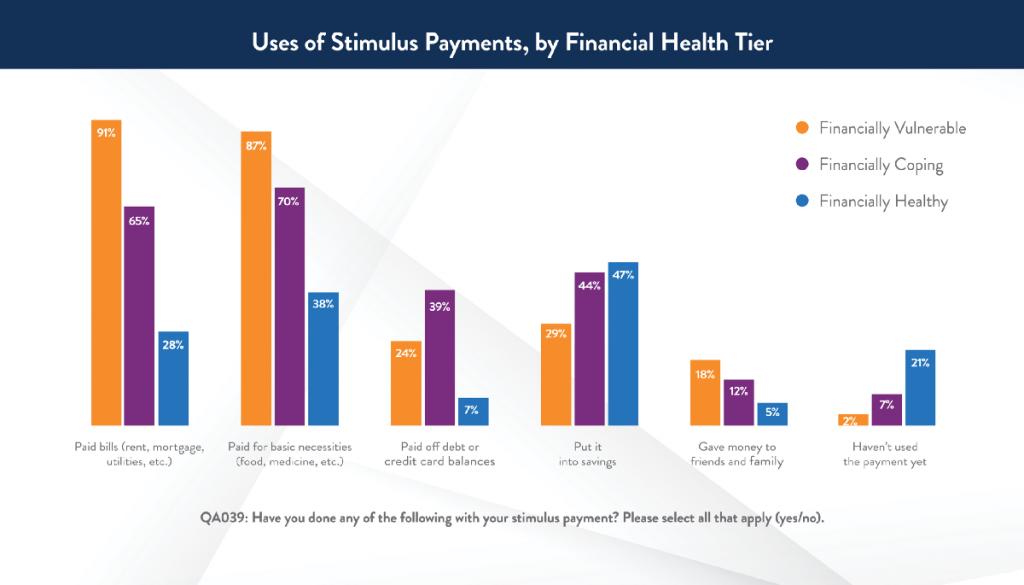

Financially Vulnerable respondents were far more likely to use the payments to pay bills (such as rent, mortgage, or utilities); to cover basic necessities (such as food and medicine); and to give money to friends and family. Financially Coping respondents were more likely to use the payment to pay off debt or credit card balances, while Financially Healthy respondents were more likely to put the money into savings.

While more research is needed to explore the effectiveness of different relief policies, this analysis joins the growing body of research showing that stimulus payments are helping people cope with less income. As policymakers consider additional policy interventions amid persistently high unemployment, we hope these findings underscore the critical role that supplemental income can play in preventing a financial health crisis for millions of Americans.

Methodology Notes: The FinHealth Score® results presented in this blog post are based on a fixed-effects regression that controls for all observed and unobserved time-invariant factors, as well as the following time-variant factors that are significantly correlated with year-over-year changes in financial health: homeownership, self-reported health status, income predictability, health insurance coverage, being the caregiver of an adult, starting a new job, having a major medical expense, and experiencing a natural disaster. Household income is also a time-variant factor that was omitted from independent variables because of collinearity with job loss. In a separate subgroup analysis of people who lost their jobs, we confirm that the correlation between stimulus payments and change in FinHealth Score remains significant after including 2020 household income along with other demographic factors. Results are significantly different from null at a 95% confidence level.

The U.S. Financial Health Pulse is made possible through a founding partnership with Flourish, a venture of The Omidyar Group. Additional support is provided by MetLife Foundation, founding sponsor of the Financial Health Network’s financial health work, and AARP. The Financial Health Network is partnering with the University of Southern California Dornsife Center for Economic and Social Research to field the survey to their online panel, the Understanding America Study. The Financial Health Network is working with engineers and data analysts at Plaid to collect and analyze transactional and account data from study participants who authorize it.