What’s Holding Back Consumers From Using AI Financial Tools?

Financial institutions face multiple challenges driving customer adoption of AI financial tools.

Over the past five years, banks and financial institutions have begun using robo-advisors, general chatbots, and other AI tools to provide customers with financial advice at unprecedented rates.1 Recent research has shown that while consumers are excited by the possibilities AI presents, many remain concerned about AI-generated misinformation.2 With new AI tools emerging in the financial world, we find that financial institutions face challenges in tackling barriers related to trust, awareness, usability, and access that impact adoption across diverse groups.

To better understand the challenges AI tools face with consumers seeking financial advice, it’s essential to examine how people currently use and engage with various personal finance information sources. We find that few households reported using AI tools for information about personal finances in 2024, especially when compared to other advisory sources.

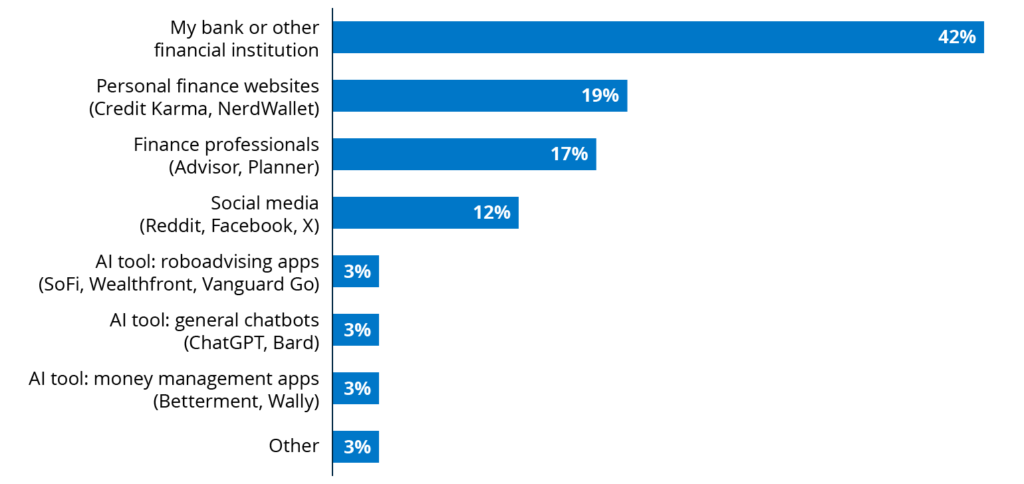

Financial Health Pulse® survey data collected by the Financial Health Network from April through June 2024 reveals that 42% of U.S. households turned to their bank or financial institution for financial information over the past year – the highest percentage among all reported sources (Figure 1).3 By contrast, AI tools like general chatbots (e.g., ChatGPT or Bard4) and automated investing or robo-advisor apps (e.g. SoFi, Wealthfront, or Vanguard Go) had the lowest levels of use, with only 3% of households reporting they used each type of tool for financial information. Money-management apps unaffiliated with a bank that contain AI features, such as Betterment or Wally, had similarly low levels of reported use. Other sources of financial information sit between financial institutions and AI tools in terms of use, including personal finance websites, such as Credit Karma or NerdWallet (19%); financial professionals, advisors, or planners (17%), and social media (12%).

Figure 1. AI tools, such as general chatbots and robo-advising apps, remain less commonly used as sources for financial information.

Percentage of households that reported using each source of information for their personal finances in the past 12 months.

Notes: Financial Health Pulse Survey 2024. N = 7,255.

AI Tool Awareness

Prior research suggests that consumers may rely more on banks, personal finance websites, and finance professionals because they believe financial decisions often involve complex considerations and emotional factors best addressed with the guidance of a human advisor.5 In addition to this preference for human guidance, there are multiple other reasons why AI tools struggle to gain the same level of usage as traditional sources of information.

We find that, in 2024, one of the primary barriers to the adoption of AI tools for financial advice was unfamiliarity. Among respondents who reported not using general chatbots, 26% said that they had never heard of them. Meanwhile, over a third (36%) of those who did not use automated investing or robo-advising apps also said it was because they had never heard of these tools, suggesting that a lack of awareness is an even larger barrier for the use of robo-advising apps than for chatbots.

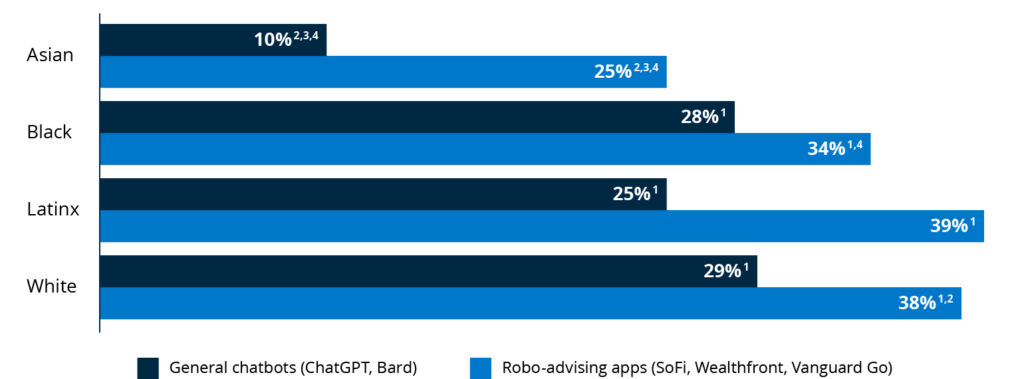

Historical inequities have limited some groups’ access to and awareness of financial services provided through banks and traditional methods, which may then shape how they respond to and engage with emerging AI financial tools.6, 7, With this in mind, we estimated how awareness of AI tools differed by race and ethnicity. We found that Asian households were more likely to be familiar with AI tools like chatbots and robo-advisors than Black, Latinx, and white households. For example, only 10% of Asian households reported not having heard of chatbots, compared with over a quarter of Black, Latinx, and white households (Figure 2). Among Asian respondents, higher levels of awareness may reflect greater exposure to AI technologies. Research has shown Asian American workers have the highest rate of regular exposure to AI in their jobs compared with other racial groups,8 which may make them more aware of both the risks and benefits of AI tools.

Figure 2. Awareness is less of a barrier for Asian households than Black, Latinx, and white households.

Among those who did not use AI tools, percentage reporting “I have never heard of it,” by race and ethnicity.

Notes: Financial Health Pulse Survey 2024. Other racial identities are not shown due to small sample sizes.

1 Statistically significant relative to Asian at p < .05.

2 Statistically significant relative to Black at p < .05.

3 Statistically significant relative to Latinx at p < .05.

4 Statistically significant relative to White at p < .05.

Knowledge, Trust, and Other AI Barriers

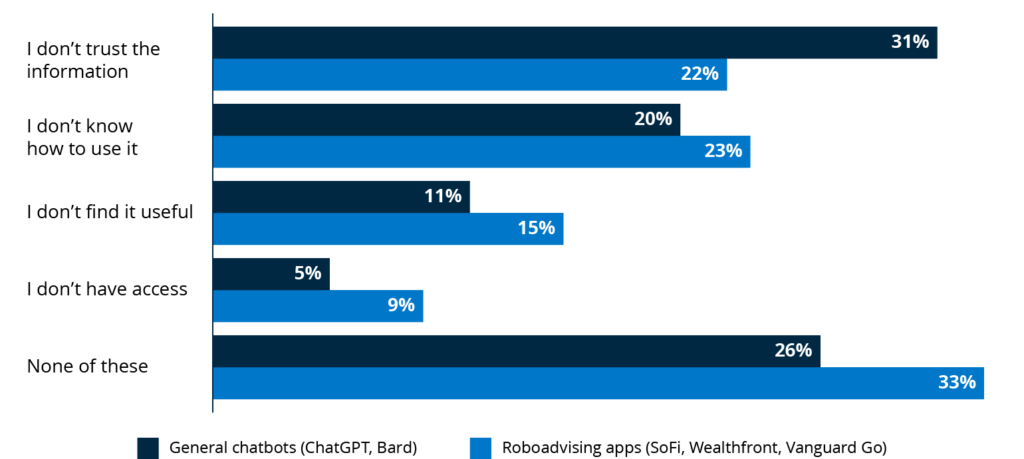

We also aimed to understand why some people who were aware of AI tools were not using them. In the Financial Health Pulse 2024 survey, we asked respondents to select all of their reasons for not using chatbots and robo-advisors. A lack of trust in the information provided by these tools was commonly selected as a reason for not using chatbots (31%) and, to a lesser extent, robo-advisors (22%) (Figure 3). Not knowing how to use the tool was also frequently selected for both chatbots and robo-advisors (20% and 23%, respectively). These results indicate that the barriers to using AI tools for financial advice may vary depending on the type of tool, with distrust emerging as a larger hurdle for chatbots.

However, a significant portion of respondents selected “None of these” in response to this question for both chatbots (26%) and robo-advisors (33%) (Figure 3). These percentages were especially high for Black and Latinx respondents. When asked why they didn’t use chatbots, 41% of Black respondents and 34% of Latinx respondents selected “None of these.” For robo-advisors, 46% of Black respondents and 40% of Latinx respondents selected the same option. These findings may indicate a gap in understanding, relevance, or trust in AI tools that current frameworks are not capturing, particularly among Black and Latinx communities.

Figure 3. Lack of knowledge and trust are among the top reasons why consumers aren’t using AI for financial advice.

Percentage of households reporting each reason for not using AI tools over the past 12 months, among those who reported having heard of the tools.

Notes: Financial Health Pulse Survey 2024. N = 4,530 respondents who reported not using chatbots and 5,283 respondents who reported not using robo-advisors.

Acknowledgements

The Financial Health Pulse is supported by the Principal Foundation. The findings, interpretations, and conclusions expressed in this piece are those of the Financial Health Network and do not necessarily represent those of our funders or partners.

![]()

Written by

-

Associate, ResearchFinancial Health Network

Associate, ResearchFinancial Health Network -

Director, Policy and Research

Director, Policy and Research