Strategies To Encourage Credit Score Monitoring Among Young People

A significant portion of young adults don’t regularly check their credit scores, but financial institutions can help turn this trend around.

According to data collected from April through June of 2023 by the Financial Health Network as part of its Financial Health Pulse® study, a third (32%) of Americans did not check their credit score in the last year. Individuals who did not check their credit scores often included those with lower financial health, lower income, or lower education levels; people who self-reported having poor credit scores; renters; Latinx people; and young adults.

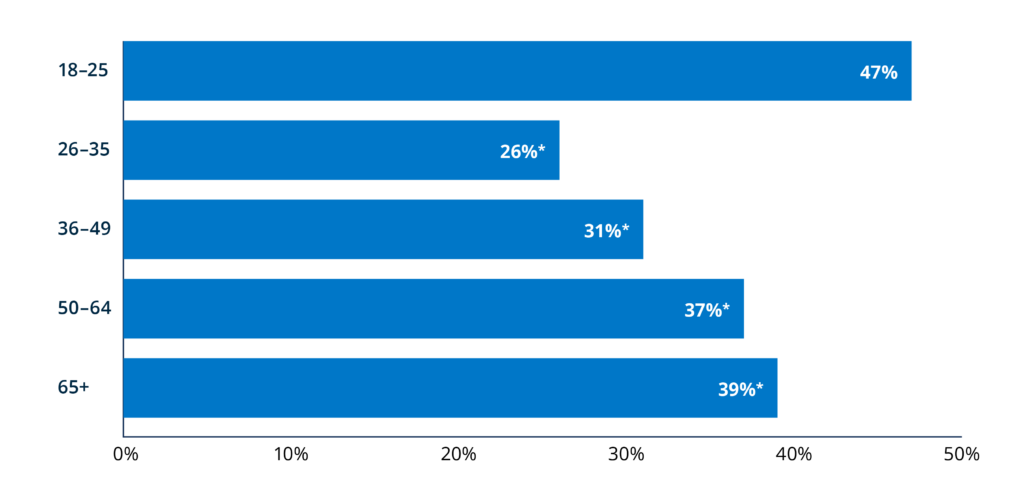

One of the largest gaps in credit checking practices occurred across age groups, with almost half (47%) of young people (18- to 25-year-olds) not checking their credit scores in the last 12 months – a considerably higher share than older age groups (Figure 1).

Figure 1. Almost half of young adults (ages 18 to 25) did not check their credit scores in the last year.

Percentage of people who did not check their credit scores in the last year, by age group.

Note: * statistically significant relative to 18- to 25-year-olds at p < 0.05. Data from 2023 Financial Health Pulse® survey. N = 8,269 respondents who responded to the question, “In the past 12 months, have you checked your credit score?.”

“It is concerning that many young people are not regularly monitoring their credit scores because it leaves them uninformed about their financial well-being and unprepared for potential future financial needs, such as buying a home or a car or even securing rental housing.”

Wanjira Chege

Strategy 1: Help Young People Build Credit by Including Alternative Data in Credit Reporting

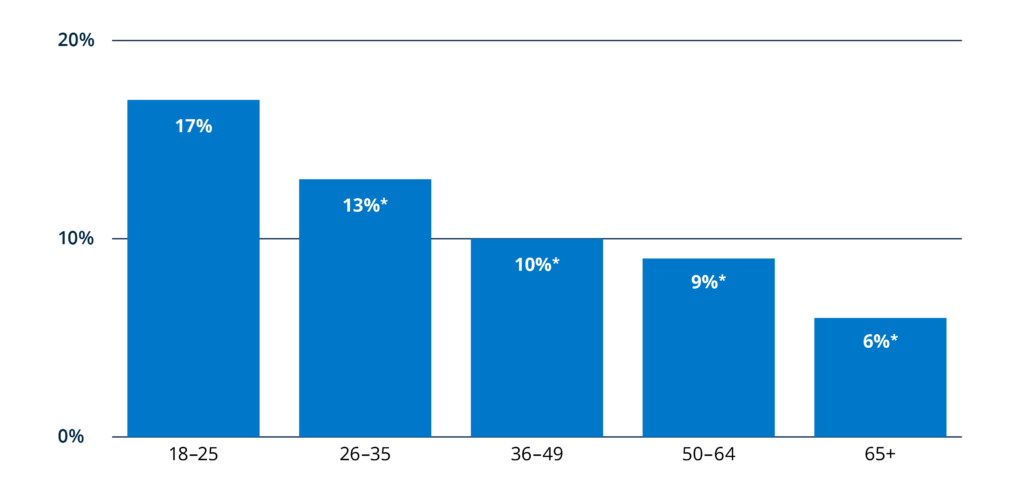

Younger adults may not regularly check their credit scores because they have less engagement with credit products and services. Our data reveal that individuals living in households without auto loans, credit cards, mortgages, small business loans, or past-due medical bills, which are the main components of building credit scores, less frequently report checking their credit scores within the last 12 months. And young adults less frequently have these forms of debt compared with their older counterparts (Figure 2). This suggests that the absence of such debt is related to less frequent credit score monitoring among young adults, potentially because they may not have credit scores at all.9

Figure 2. Young adults less frequently have the forms of debt mainly used to calculate credit scores.

Percentage of people without various forms of debt, by age group.

Note: * statistically significant relative to 18- to 25-year-olds at p < 0.05. Data from 2023 Financial Health Pulse® Survey. N = 8,270 respondents who answered “no” to the following questions: “Do you or anyone in your household currently have one or more of the following types of credit cards? [1.General purpose credit card 2. Store credit card]”, “Do you or anyone in your household currently have any of the following types of debt? [1. Auto loans 2. Small business loans 3. Mortgages 4. Past-due medical bills].”

Financial institutions could help young adults establish a solid financial foundation for their future.

-

- Financial institutions and rental housing providers can more consistently report on-time utility and rent payments to credit bureaus.

- Credit bureaus can consistently incorporate information on on-time rental and utility payments and payment history into credit scores.

- Financial institutions can proactively offer lower-risk credit products, such as secure credit cards, to young people to help them build credit profiles.

Strategy 3: Reduce the Anxiety Associated With Checking Credit Scores

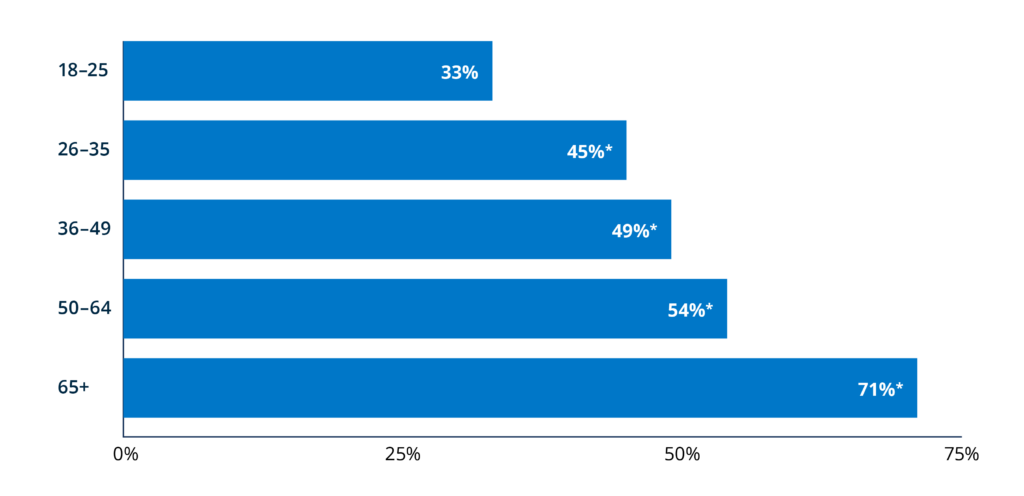

Avoiding disappointing or unpleasant financial news is often cited as a factor influencing various financial behaviors.19 Indeed, young adults less frequently self-report having an excellent or very good credit score compared with their older counterparts (Figure 3), potentially deterring them from regularly checking their credit scores. However, not monitoring credit scores can exacerbate credit problems over time.20

Figure 3. Young people less frequently report excellent or very good credit scores.

Percentage of people with excellent or very good self-reported credit score, by age group.

Note: * statistically significant relative to 18- to 25-year-olds at p < 0.05. Data from 2023 Financial Health Pulse® survey. N = 8,269 respondents who responded to the question, “How would you rate your credit score? Your credit score is a number that tells lenders how risky or safe you are as a borrower.”

Financial institutions can help young people overcome risk avoidance around credit scores.

-

- For young people who have low credit scores because their credit history is relatively short, financial institutions can demystify credit scores and foster a sense of progress by projecting how a young person’s credit score may develop over time with future on-time payments and sharing that information alongside current credit scores.

- By offering tailored debt management support and lower-risk credit products to young people, especially those struggling with credit card debt, financial institutions can transform the credit monitoring experience from one of apprehension to one of empowerment and positive engagement.21, 22, 23

Financial institutions have an important role in helping young people with credit score monitoring. By proactively providing products and support tailored to the needs of young people, financial institutions and professionals not only empower the younger generation with essential financial skills, but also contribute to the overall health of the financial landscape.

“Credit score monitoring is an important part of overall financial health. And while behaviorally informed ‘nudges’ have been used to support a variety of positive financial behaviors, financial institutions have an opportunity to use some of these same approaches to support regular credit monitoring, particularly for young adults.”

Angela Fontes

Acknowledgements

The authors thank David Silberman and Amelia Josephson for their contributions. The Financial Health Pulse is supported by the Principal Foundation, with additional funding from the Citi Foundation. The findings, interpretations, and conclusions expressed in this piece are those of the Financial Health Network and do not necessarily represent those of our funders or partners.