Responding to Reform: Overdraft in 2023

After pivotal reforms in 2022, this FinHealth Spend Product Spotlight sheds light on the state of overdraft fees today, how consumers use overdraft, and potential implications for financial institutions and policymakers.

Without Overdraft, Many Would Not Have Made the Purchase

The issue of a “counterfactual” – what people would do if overdraft were not available – has been a central issue of discussion in the overdraft debate. Voices arguing in favor of overdraft protection claim that, if overdraft were not available, people would turn to high-cost payday or pawn loans.10 Meanwhile, a number of large banks have begun offering rapid, small-dollar loans and lines of credit as possible lower-cost alternatives, and numerous companies have introduced technologies that advance access to earned wages.11, 12

To shed light on this issue, we added a question to the 2023 survey that asked a subset of overdrafters what they would have done during their most recent overdraft transaction if overdraft were not available. We specifically asked this question among only those who overdrafted intentionally, as this group consciously made a choice to overdraft the account (and incur the fee) to ensure a purchase or payment went through. The group that overdrafts intentionally is almost exclusively Financially Coping or Vulnerable.

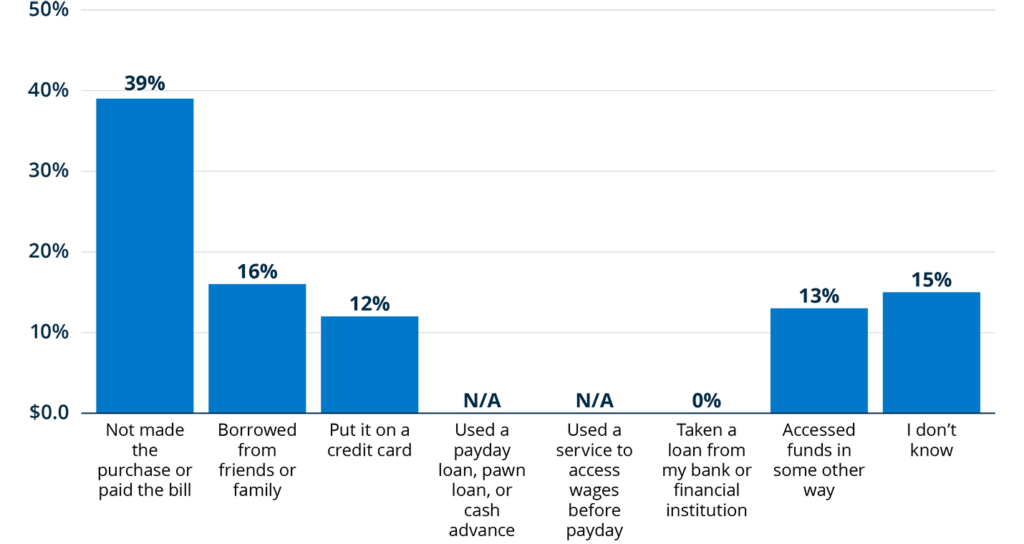

While sample sizes are small (n=114), very few people said they would have either used a service to access wages before payday or utilized an alternative credit product like a payday, pawn, or cash advance loan. Furthermore, not a single respondent answered that they would have “taken a loan from my bank or financial institution,” which could suggest a lack of awareness about the availability of relatively new, lower-cost loans.13 Rather, a plurality of respondents (39%) said they wouldn’t have made the purchase or paid the bill. For at least some of these individuals – who made the intentional decision to incur an overdraft fee to finance a purchase – this finding suggests a pressing need for immediate liquidity, without which they would not be able to make the purchase.

Figure 1. Nearly 4 in 10 intentional overdrafters said they would not have made the purchase or paid the bill.

Alternative payment source, among intentional overdrafters.

(n=114)

Notes: Responses to “Thinking about your most recent overdraft experience, if overdraft were not available, I would have…” Response options were “Taken a loan from my bank or financial institution;” “Used a service such as a payday loan, pawn loan, or a cash advance;” “Used a service to access wages before my payday;” “Borrowed from friends or family;” “Put it on a credit card;” “Accessed funds in some other way;” “Not made the purchase or paid the bill;” and “I don’t know.” No respondents selected “Taken a loan from my bank or financial institution” as an option, and too few responded “Used a service such as a payday loan, pawn loan, or a cash advance” or “Used a service to access wages before my payday” to report.

New Data on Overdraft by Race Reveal Disparities

Previous FinHealth Spend data has established that banked households of color are more likely to incur at least one overdraft/NSF fee than white households.14 This disparity remains true in 2023: 31% of Black households and 24% of Latinx households with checking accounts reported being charged an overdraft fee in 2023, compared with 14% of white households. That said, as in prior reports, we do not find evidence that overdrafting households of color are more likely to overdraft frequently (10+ times) than overdrafting white households.15, 16

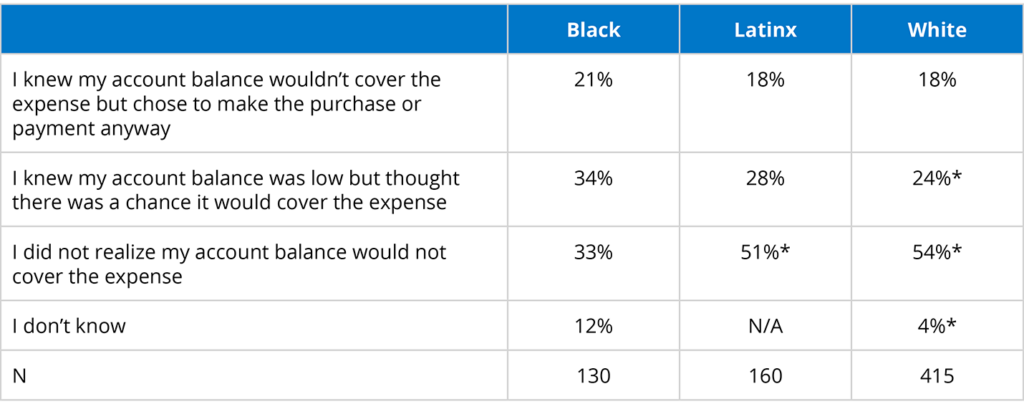

However, this year, we start to shed additional light on the disproportionate impact of overdraft among Black communities. First, when thinking about their most recent overdraft, Black households reported that they were aware that the purchase or payment might result in an overdraft at greater rates than white households, who more often reported that the overdraft was unintentional. More than half (55%) of Black overdrafters said that they were aware that there was at least some risk, compared with 42% of white overdrafters.17

Table 1. Over half of Black households that overdraft report knowing there was at least some risk of incurring a fee.

Intentionality of overdraft, by race/ethnicity.

Notes: Responses to the question, “Thinking about your most recent overdraft/NSF experience, which of the following is most accurate?” Too few Latinx respondents reported “I don’t know” to report.

* Statistically significant difference compared to Black respondents (p < 0.05).

Furthermore, our 2023 data finds a small but statistically significant difference in the size of the purchase or payment that incurs an overdraft. Thirty-one percent (31%) of Black overdrafters said their most recent overdraft was on a purchase or payment of $25 or less, versus 22% of white overdrafters. Conversely, only 22% of Black overdrafters said their last overdraft was on a purchase or payment of $100 or more, compared with 33% of white households.

Taken together, these data points suggest that Black households are more frequently faced with circumstances that lead them to incur or risk incurring an overdraft fee. Intentional overdrafts are more frequently made by those in difficult financial circumstances, and with the average overdraft fee still at about $30-$35, incurring those costs for a $25 purchase suggests a lack of other attractive and immediate options.