Research Paper

Reexamining Overdraft Programs: A Guide for Financial Institutions

Reforming overdraft can help institutions improve customer finhealth, acquire new customers, and boost loyalty.

Frequent Overdrafters

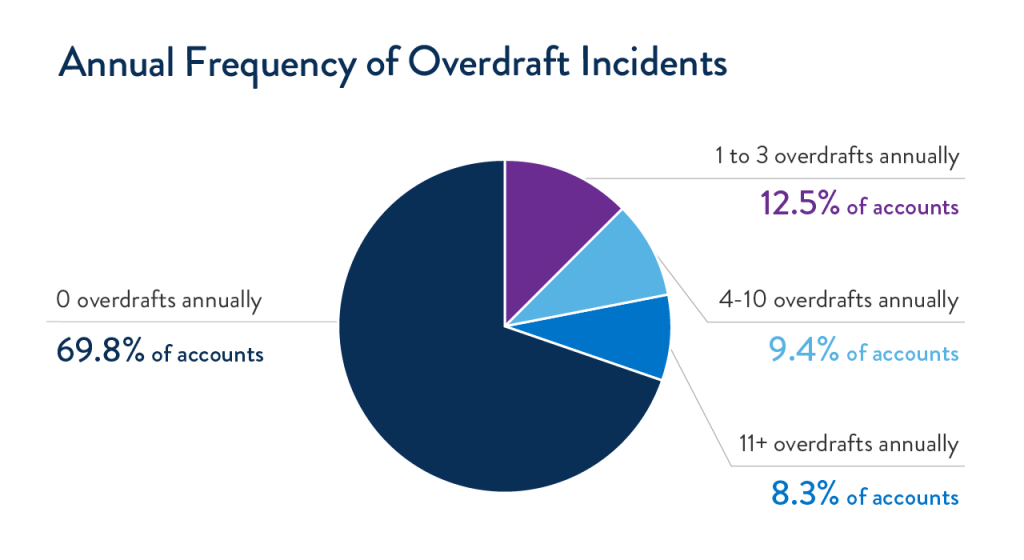

Among those who overdraw their accounts, more than 40% do so infrequently, with one to three incidents annually. On the other hand, more than 25% overdraw frequently, with at least 10 overdrafts or non-sufficient funds fees annually. Among frequent overdrafters, 50% are very frequent users, with 20 or more overdrafts annually.

For these customers, overdraft can be a substantial cost and a significant drag on their financial health, and it could cause them to leave the banking sector altogether.

Written by

-

Senior Manager, Innovation

Senior Manager, Innovation -

Senior AdvisorFinancial Health Network

Senior AdvisorFinancial Health Network -

Senior Director, Financial Services Solutions

Senior Director, Financial Services Solutions

Reexamining Overdraft Programs: A Guide for Financial Institutions

Explore the trends. Discover new insights. Build stronger strategies.