Pulse Points Summer 2023: Weathering Financial Setbacks From Natural Disasters

Severe weather can disrupt financial health, yet fewer than expected Americans living in disaster-prone areas carry residential insurance.

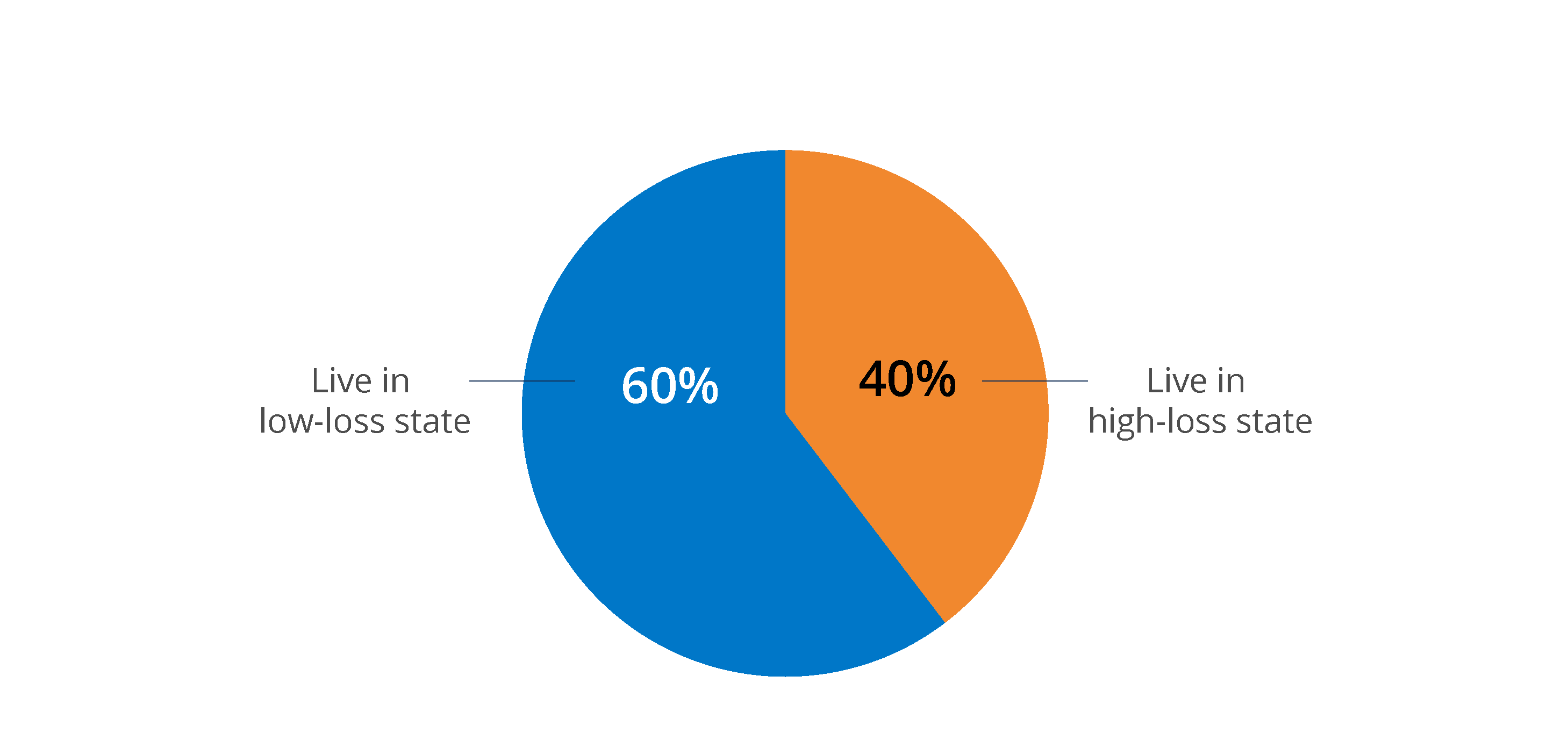

2 in 5 Americans Live in 11 States at Higher Risk for Natural Disaster Losses

Our research shows that two out of five (40%) Americans – 103.4 million in total – live in 11 high-loss states with above-average expected annual losses from natural disasters.20

This suggests that the potential to experience loss from a natural disaster is widespread, emphasizing the importance of purchasing adequate homeowners or renters insurance to prepare for such a possibility. It also indicates that the coverage of a considerable share of Americans may be impacted in the future as insurers raise rates or decline to issue new policies in certain states.

Figure 1. 2 in 5 Americans could experience higher-than-average natural disaster losses.

Percentage of people living in high-loss versus low-loss states.

Note: Loss from natural disaster occurrence determined with FEMA data. N = 5,648 respondents.

Losses from natural disasters are also an equity issue. Those living in high-loss states were more frequently Financially Vulnerable than residents of low-loss states and were also disproportionately Asian, Latinx, or selected multiple races or ethnicities (analyses not shown).21 These findings point to the increased importance of insurance to safeguard the finances of those living in high-loss states, since they may find it especially challenging to weather the financial consequences of a natural disaster.

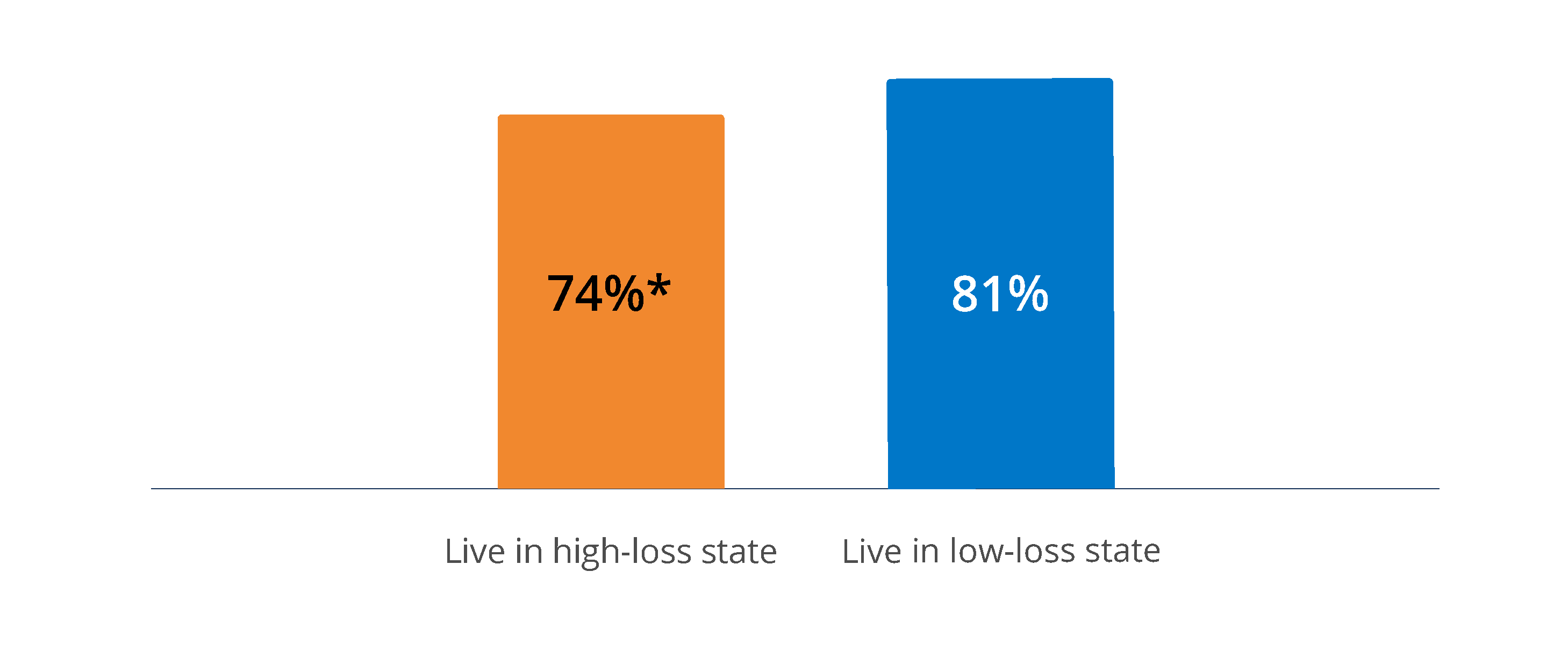

Residents of High-Loss States Less Frequently Use Residential Insurance

Insurance can play a critical role in managing the financial challenges that arise in the aftermath of a disaster.22 Yet, we find that renters and homeowners living in high-loss states were less frequently covered by residential insurance than those living in low-loss states (Figure 2). With lower rates of insurance coverage among residents of states facing the greatest losses from natural disasters, consumers in high-loss states may be financially unprepared should a disaster occur. Moreover, given that residents of high-loss states were more often Financially Vulnerable, they may not have the financial resources to cover unexpected expenses in the wake of a disaster.

Figure 2. Residents of high-loss states carry residential insurance less frequently.

The percentage of homeowners and renters covered by residential insurance living in high-loss versus low-loss states.

Note: * Statistically significant vs. people living in low-loss states (p < 0.05). N = 5,648 respondents.

Indeed, in the wake of a disaster, prior research finds that disparities often widen.23 Although this brief does not examine what happens to consumers’ financial health in the aftermath of a disaster, access to residential insurance in high-loss states may be a contributing factor to financial health disparities. For instance, in analyses not shown, we find that residential insurance coverage is lower among Asian, Black, and Latinx residents of high-loss states relative to White residents of those same states. Assuming that residential insurance offers adequate protection to consumers, this suggests that people of color are less likely to be shielded from financial losses incurred by a natural disaster and may contribute to disparities in wealth among residents of high-loss states.

Lower Residential Insurance Coverage in High-Loss States Driven by Disproportionate Share of Renters

In part, the low rates of residential insurance coverage in high-loss states are driven by the disproportionate share of renters in these states. Over a third (37%) of residents in high-loss states rented their homes, but renters comprised only 27% of residents in low-loss states (Figure 3). Consistent with other research, we also find that renters purchased renters insurance at relatively low rates, regardless of the natural disaster loss in their state (analysis not shown).24, 25, 26

In the event of a disaster, renters are not responsible for financing repairs to the building where they live, but they may need to replace or repair belongings that are damaged or destroyed. Navigating the financial implications of a disaster without insurance may be especially challenging for renters because they typically have lower incomes, less wealth, and lower financial health than homeowners.27 In addition, renters are more often Black or Latinx, so experiencing a natural disaster without insurance may contribute to racial disparities in financial health.28

Figure 3. Residents of high-loss states are more frequently renters.

Percentage of residents who are renters by residence in high-loss and low-loss states.

Note: * Statistically significant vs. people living in low-loss states (p < 0.05). N = 5,648 respondents.

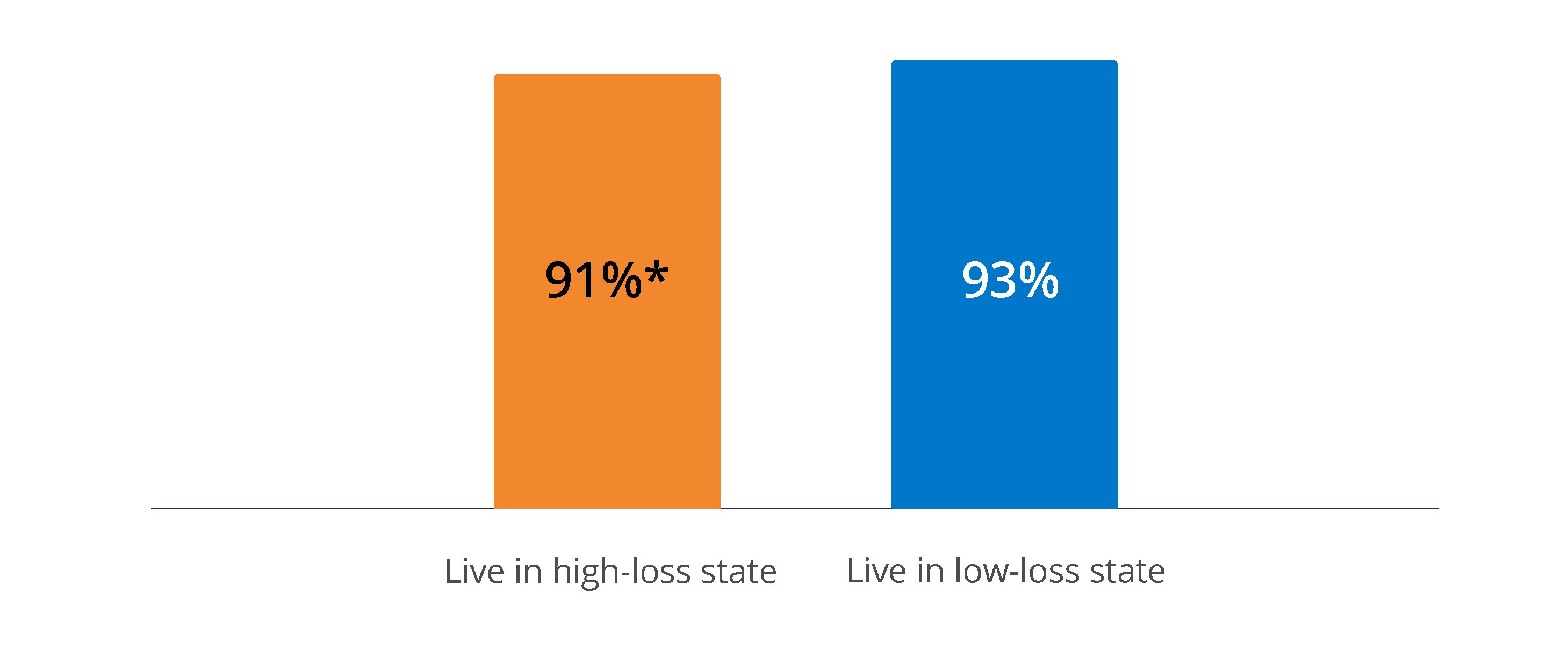

Homeowners Less Frequently Carry Insurance in High-Loss States Than in Low-Loss States

However, renters are not solely responsible for the gap in residential insurance coverage observed between high- and low-loss states. Although most financial institutions require home insurance as part of a mortgage agreement, insurance can sometimes lapse or insurers can cancel policies. In addition, those who have paid off their homes are no longer required to purchase insurance.

Thus, homeowners insurance coverage was relatively common in both high- and low-loss states. However, contrary to what we would anticipate based on the likelihood of loss, homeowners in high-loss states less frequently reported coverage than homeowners in low-loss states (91% vs. 93%). While this difference is small, it represents about 8.8 million Americans living in uninsured homes in 11 high-loss states, which is about 240,000 more than the number of Americans residing in uninsured homes across all 39 low-loss states.29 This difference may also grow in the future as insurance providers reconsider offering new applications for coverage in high-loss states.

Figure 4. Homeowners in high-loss states less frequently carry homeowners insurance.

Percentage with homeowners insurance coverage among homeowners by residence in high-loss and low-loss states.

Note: * Statistically significant vs. homeowners living in low-loss states (p < 0.05). N = 3,991 respondents. These analyses focus on homeowners who knew if they held home insurance.

Lower-Income Homeowners Are Less Frequently Covered by Insurance

Along with fewer insurance options and different perceptions of risks, the ability to afford insurance plans is one barrier that prevents insurance takeup. Cost may play a role in the homeowners insurance gap observed between high- and low-loss states. In states prone to natural disasters, insurance premiums can be more expensive, but residents in these states also typically have lower household incomes.30, 31 To understand whether affordability is associated with the lower takeup of residential insurance in high-loss areas, we show how homeowners insurance coverage varies by household income in high- and low-loss states.

First, consistent with prior findings, homeowners with lower incomes less frequently carry insurance.32 We find that this is true in both high- and low-loss states. For instance, regardless of disaster loss, about 3 in 4 homeowners with household incomes less than $30,000 carried insurance, whereas coverage was nearly universal among those with incomes of $100,000 or greater. This suggests that low household incomes may act as a barrier to insurance takeup, regardless of the risk of natural disaster loss.

Second, once income is accounted for, we show that the takeup of homeowners insurance coverage is very similar for homeowners in high- and low-loss states (Figure 5). The one exception to this pattern was homeowners with household incomes between $30,000 and $59,999. For homeowners in this income bracket, insurance coverage was less common in high-loss states than low-loss states (87% vs. 94%). For all other income groups, there was no discernible difference in the takeup of homeowners insurance.

Figure 5. Households with higher incomes more frequently have insurance.

Percentage of homeowners with homeowners insurance by income and residence in high-loss versus low-loss states.

Note: * Statistically significant vs. homeowners living in low-loss states (p < 0.05). N = 3,991 respondents.

Because many high-loss states also have a greater share of households with lower incomes, some of the gap in insurance ownership between households in high- and low-loss states can be explained by differences in the income distributions of these states, where high-loss states have greater proportions of households with lower incomes.33 However, given the greater risk associated with living in high-loss states, we would anticipate insurance ownership in these states to be higher on average when compared with low-loss states, rather than equal. This lack of difference could stem from either an inability to obtain insurance or a difference in consumer preferences.