How Digital Communities Can Drive Financial Decision-making and Customer Satisfaction

In collaboration with legal empowerment fintech Upsolve, we explore how incorporating a digital community into fintech tools can support user financial decision-making and improve customer satisfaction.

Higher propensity to take financial action.

Higher financial confidence and self-reported well-being.

Higher satisfaction with the company providing the digital community.

Upsolve’s bankruptcy filing tool helps users who would not otherwise be able to afford to file for bankruptcy. The company’s digital community, meanwhile, appears to make it more likely that consumers will use Upsolve’s tool to file, indicating a way in which digital communities can complement financial services and drive consumers to take financial action that will enhance their financial health.

-

- A digital community can drive users to take major steps like filing for bankruptcy. Although users come to Upsolve’s digital community at all stages of their bankruptcy journey, data on the percentage of users who follow through with filing suggest that Upsolve helps sustain motivational momentum through what can be a complicated process.11 For example, 61% of respondents who have filed for bankruptcy say they would not have filed without engaging with Upsolve’s digital community platform.

- A digital community can reduce the need for high-cost resources. Further, 68% of those who say they wouldn’t have filed without Upsolve report that they had trouble affording an attorney to help them file, significantly more than those who stated they would have filed with or without Upsolve – demonstrating the value of Upsolve’s service and digital community in replacing the need to pay for a bankruptcy attorney.

- More-engaged users are even more likely to take action. People who frequently engage with the digital community are significantly more likely to file for bankruptcy and significantly less likely to be hesitant about bankruptcy. Respondents who engage with the community platforms multiple times per week are 13 percentage points more likely to indicate that they have filed for bankruptcy. 12 There is no significant difference between engaging one to three times per month versus once per month or less.

Digital communities aren’t just ways for fintech companies to engage their users; study results show they also correlate with increased financial well-being for users.

-

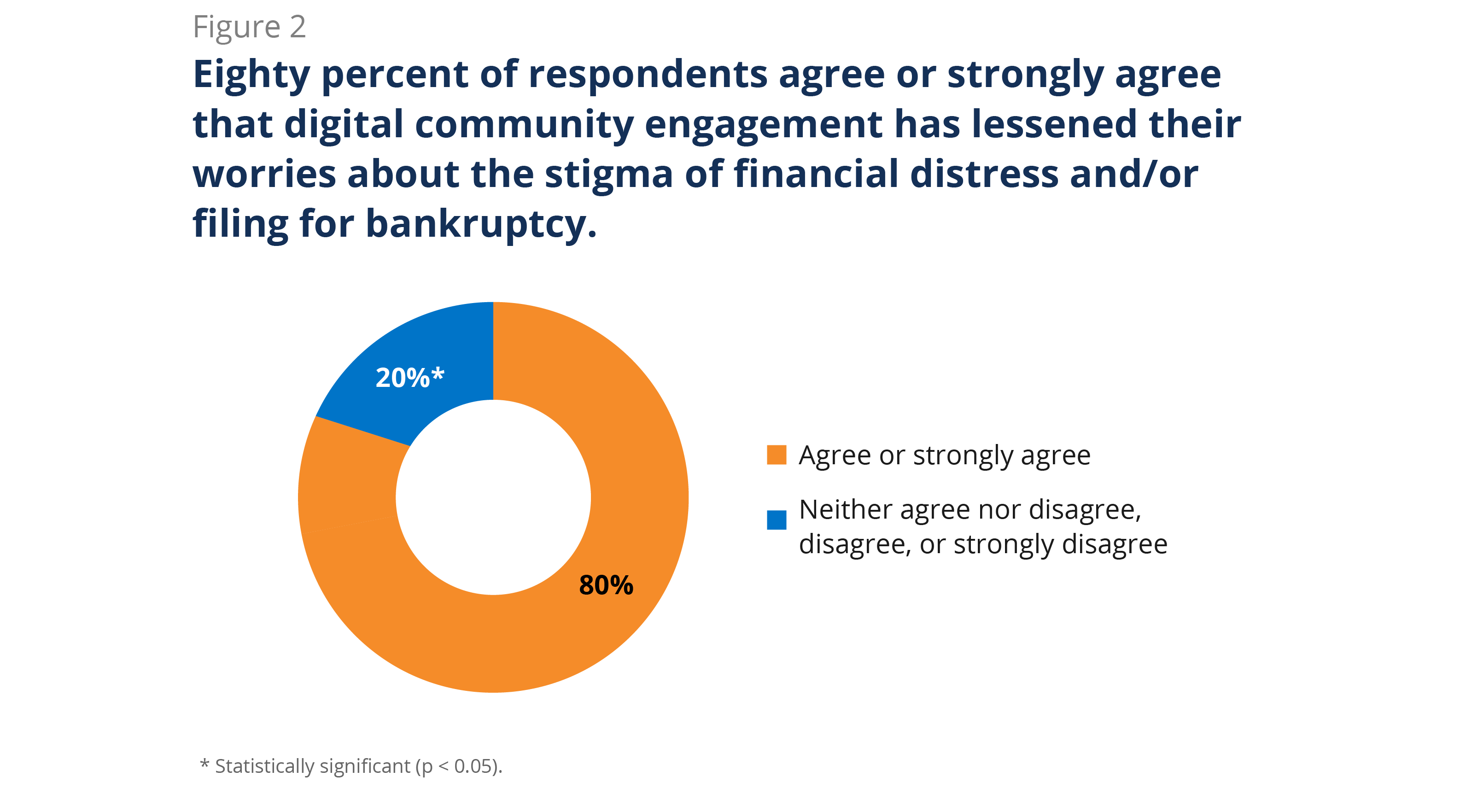

- Digital community engagement can reduce consumer worries about the stigma of financial hardship. Though not all survey respondents were frequent users of the digital community, we found that around 80% of respondents (across engagement levels) either agreed or strongly agreed that Upsolve community engagement lessened their worries about the stigma of financial distress or filing for bankruptcy.13

-

- Connection in a digital community can also drive self-confidence. Sixty percent of all respondents either agree or strongly agree that giving advice to others boosts their self-confidence in making decisions on personal financial matters.

- Benefits to users of the digital community appear to increase as engagement becomes more frequent. Respondents who engage with the community at least once a month are 18% more likely to say they are confident in their ability to reduce their debt or remain debt-free, and 13% more likely to indicate they increased their ability to plan ahead financially, compared with people who engage once a month or less.14

- Participation in a digital community can improve emotional and mental health outcomes. Users who engaged with the platform at least once a month were 13% more likely to report improved stress and mental health, 18% more likely to indicate that they have been able to focus more on family, and 20% more likely to indicate that they have been able to prioritize joy in their lives, compared with people who engage once a month or less.15

Greater customer satisfaction may reduce expenses and increase profitability.16 Digital community engagement can increase both customer satisfaction and retention for the fintech company providing it.

-

- Engaging with a digital community can drive customer loyalty. Those who engage regularly with the digital community are more likely to say they would recommend the fintech tool to a friend or family member. Respondents who engage with the digital community one to three times per month have on average a 0.5-point higher Net Promoter Score (on a scale of 0-10), and those who engage multiple times per week have on average a 0.7-point higher Net Promoter Score compared with those who engage once per month or less, after controlling for current bankruptcy filing, amount of time and money saved through community engagement, gender identity, and education.

- Consumers engage with a digital community for more than just transactional reasons. Eight out of 10 respondents said they check the Upsolve digital community to hear about other people’s experiences, while 20% said they check the digital community to obtain specific product or provider recommendations.

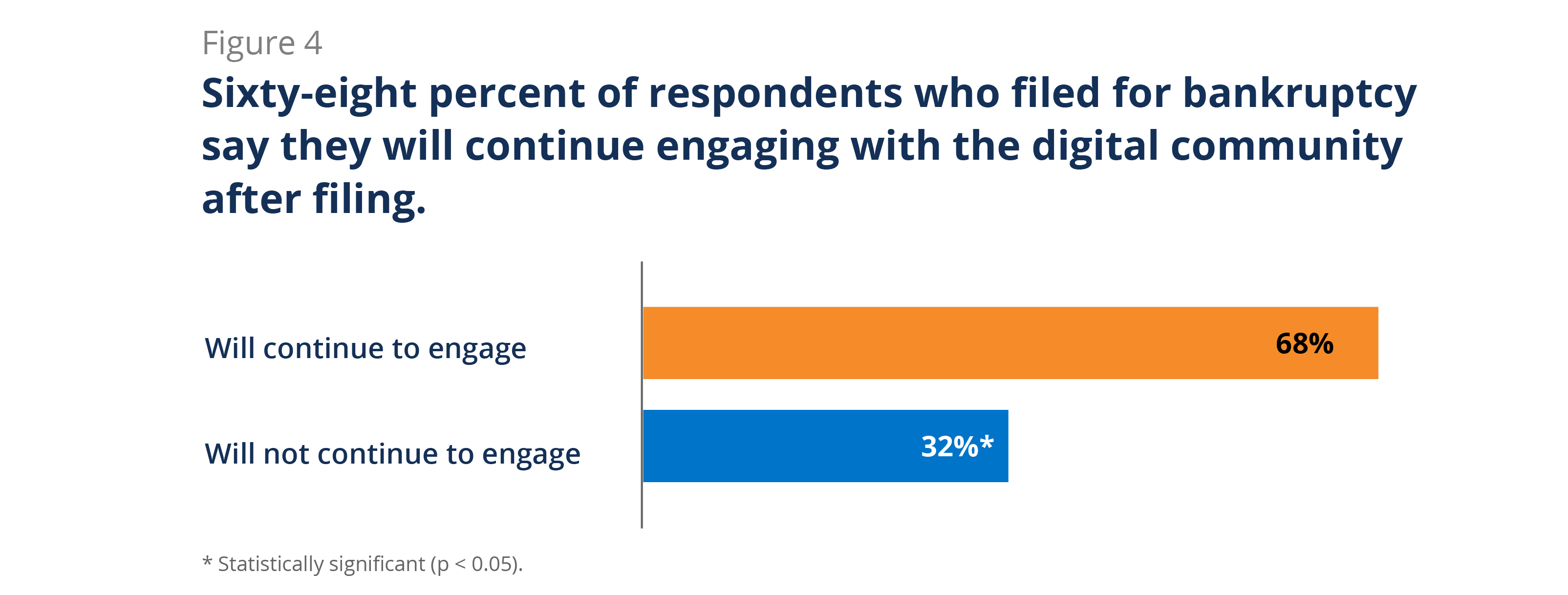

- Digital communities can benefit consumers even after they’ve already taken financial action. Providers that are considering offering a digital community may worry that once a user has obtained the information they are looking for or has taken the financial action they are considering, their engagement with the platform will end. On the contrary, we found that 68% of respondents who filed for bankruptcy say they will continue engaging with the digital community platform after filing.

The Financial Solutions Lab (FSL) was established in 2014 to cultivate, support, and scale innovative ideas that help improve financial health. FSL focuses on solutions addressing acute and persistent financial health challenges faced by low- to moderate-income individuals, Black and Latinx communities, and other underserved consumers.

The Financial Health Network manages the Financial Solutions Lab in collaboration with founding partner JPMorgan Chase and with support from Prudential Financial.

The views and opinions expressed in the report are those of the authors and do not necessarily reflect the views and opinions of JPMorgan Chase & Co., Prudential Financial, or their affiliates.

Written by

-

Senior Manager, Innovation

Senior Manager, Innovation -

Manager, ResearchFinancial Health Network

Manager, ResearchFinancial Health Network

How Digital Communities Can Drive Financial Decision-making and Customer Satisfaction

Explore the trends. Discover new insights. Build stronger strategies.