Research Paper

Financial Health Solutions: Credit Builder Loans and Rent Reporting

A study with Self examines the potential of two credit-building tools for establishing or improving credit scores.

Self’s credit-building products reached consumers with predominantly subprime credit scores.

Many subprime users of these tools moved to higher credit tiers and were more likely to increase their credit scores.

Users with credit delinquencies at the beginning of the study saw the largest credit score gains.

Most users with limited credit history established a credit score within 60 days.

Data Spotlight

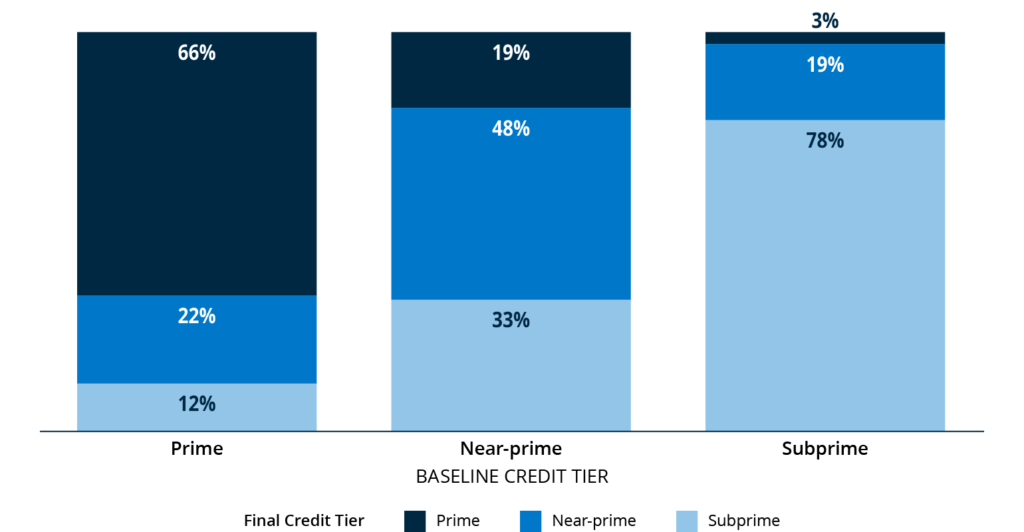

R&B users with subprime credit saw the most pronounced improvements in their credit scores.

Final credit tier for R&B users, by starting credit tier.

Financial Health Solutions: Credit Builder Loans and Rent Reporting

Explore the trends. Discover new insights. Build stronger strategies.