Climate Disaster and Renters Insurance: Who’s Protected?

A new FinHealth Spend Spotlight finds many renters don’t hold renters insurance – and those who do still face climate-related risks.

2. The Renters Who Do Hold Insurance Tend to be Disproportionately Financially Healthy, White, and Higher-Income

Among renters, the population with renters insurance tends to be more financially secure already than those without. Seventy-one percent of Financially Healthy renters have renters insurance, compared with just 32% of renters considered Financially Vulnerable (a group characterized by extreme challenges with both short- and long-term finances). As such, households that are already in difficult financial straits face outsized exposure to losses in the event of an emergency.

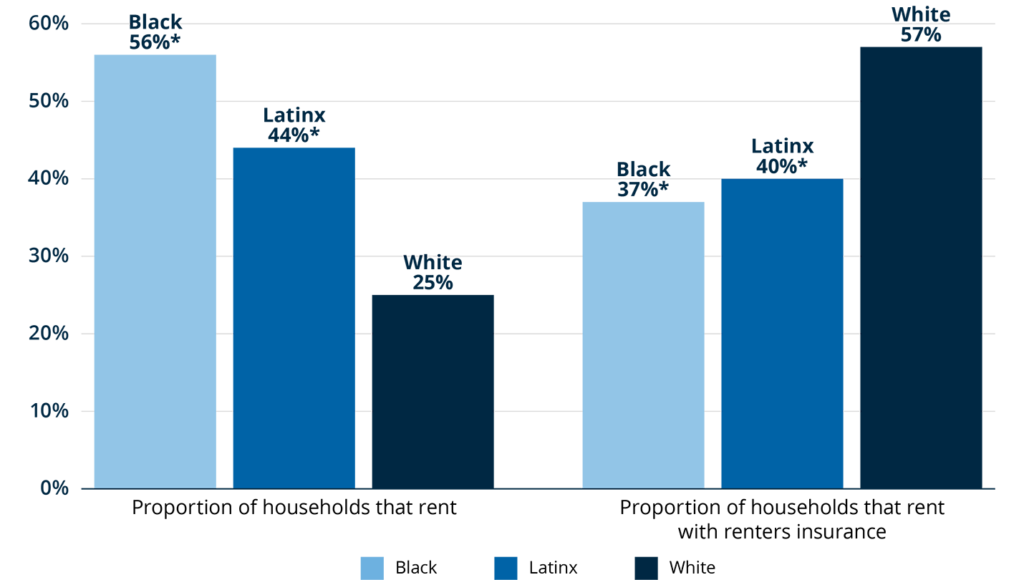

Racial disparities in renters insurance ownership are also vast. Black and Latinx households are more likely to rent (56% and 44% respectively) than white households (25%), yet Black and Latinx renters are far less likely to have renters insurance (37% and 40% respectively) than white renters (57%) (see Figure 1). Even after controlling for household income, Black and Latinx renters are less likely to hold renters insurance than white renters.

Figure 1. Black and Latinx households are more frequently renters, but they hold renters insurance less frequently.

Renter status and renters insurance ownership, by race.

Notes: Rentership status calculated among full sample (N=5,474). Renters insurance status calculated among households who indicated that they rent (N = 1,556).

* Statistically significant relative to white households (p <0.05).