Digital Currencies and Financial Health

Digital currencies have the potential to improve financial health for millions, but it depends on how they are designed and integrated into the financial services infrastructure.

*This article was sponsored by PayPal. All views and endorsements expressed in this article are solely those of the author and do not necessarily reflect the views or endorsements of the Financial Health Network.

![]()

Millions of people in the United States live outside of the formal financial system and transact primarily in cash, but many more are underserved by the current system. These underserved individuals and families are paying excessive fees for check-cashing and short-term loans, which negatively impact their financial health. The current financial system needs an upgrade.

There is a tremendous opportunity to expand our focus from traditional notions of financial inclusion to the broader goal of universal financial health – to make the financial system more affordable, efficient, and inclusive for everyone. Innovations in technology and digital currencies, including the use of distributed ledgers, cryptography, and smart contracts, may be a powerful part of the solution.

Financial inclusion has been cited as a key motivation behind many central banks’ efforts to explore a central bank digital currency (CBDC). In economies where cash usage is declining, CBDCs could provide the inclusion and safety of a government-backed currency without requiring consumers and businesses to have an account with a traditional financial institution or to handle paper bills and currencies. More broadly, CBDCs may also improve financial health by enabling faster, lower-cost, and safer access to payments, including disbursements from the government.

Private forms of digital currency also have the potential to democratize financial services. Private digital currency could help revamp the underlying financial infrastructure, permitting greater access to core consumer financial products. Responsible customer-centric innovation will be an essential foundation for any effort to utilize these new capabilities for positive financial health outcomes.

However, even for forms of digital currencies that are designed with openness and accessibility at their core, barriers to access remain. Lack of smartphone devices, internet connectivity, and identity documentation, amongst other issues, need to be solved for the benefits of financial health to fully materialize in the digital economy.

Defining Financial Health

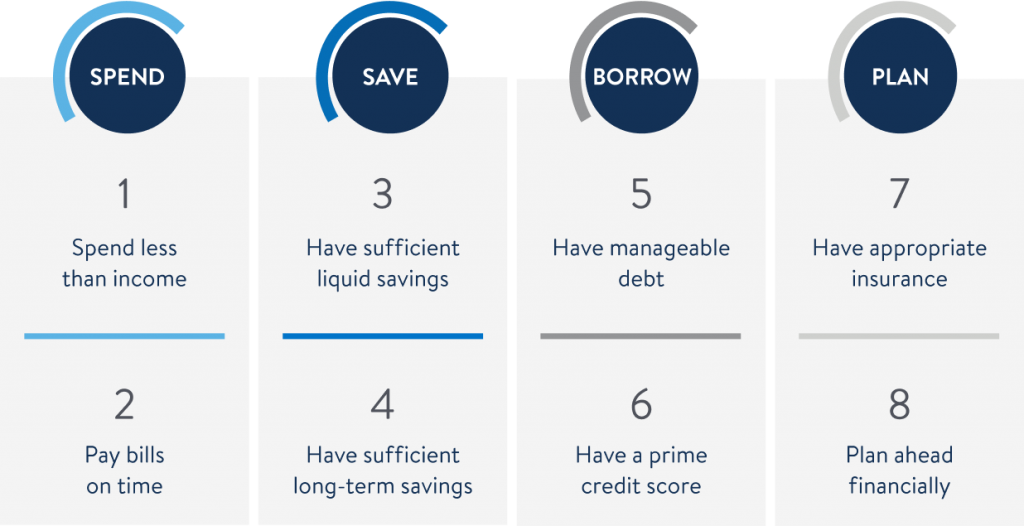

Financial health is crucial to the overall well-being of individuals, families, and communities. The Financial Health Network’s definition is helpful: Financial health refers to the ability to spend, save, borrow, and plan in a manner that enables resilience and the pursuit of opportunities over time. Financial health can be measured by the following eight indicators:

While only 5% of U.S. households are unbanked, more than two-thirds of Americans are not financially healthy. The pandemic exacerbated financial health challenges for millions of Americans, particularly women and communities of color. Depending on how it is designed, a digital currency – be it a CBDC or a private form of digital currency – could have a significant impact on financial health. Digital currencies could transform people’s ability to manage day-to-day financial needs, build resilience, and pursue opportunities.

A Thought Experiment

Since digital currencies are still in a nascent phase, it is worthwhile to consider how these new forms of money could impact financial health.

A CBDC is the digital form of a country’s fiat currency and a claim on the central bank. Instead of printing paper currency, the central bank issues digital tokens (or a digital bearer instrument) or accounts backed by the full faith and credit of the government. In 2021, 87 countries (representing over 90% of global GDP), including the U.S., are currently exploring a CBDC, compared with only 35 countries in May 2020.

Despite this momentum in CBDC research around the world and pilot programs in several countries, the ultimate designs of CBDCs have yet to crystallize. Much will depend on the combination of complex choices around factors like access, privacy, distribution, and transfer mechanisms, as well as the coordination of governance standards (or lack thereof).

Private forms of digital currency are also in their early days. Stablecoins, a privately issued digital currency (the value of which is pegged to a reference asset), have gone from a $20 billion market to more than $125 billion in just one year, bringing these new assets into greater focus. The market and models for stablecoins are highly diverse and, like CBDCs, the design choices can greatly impact the assets’ potential impact on consumers’ financial health.

In short, both CBDCs and private forms of digital currency are emerging and evolving constructs, and it is important to assess the tangible benefits these new assets could bring to consumers’ financial health.

Receive

The structure and rhythms of spending, saving, borrowing, and planning are preceded by the ability to earn income and receive funds. The way people receive money can have a significant impact on the other elements of financial health, and improvements in this regard could adaptively optimize people’s capacity to build a stable financial life.

For example, timely and, at times early, wage access for full-time workers and those with more volatile incomes could enable them to pay bills on time, lowering the cost of uncertainty and delays that cascade to other parts of their financial lives. A digital dollar and private digital currencies that are instantaneously available could provide an efficient way to receive the inflows of tax refunds, government-to-person (G2P) payments, business-to-consumer (B2C) payments, and peer-to-peer (P2P) payments. Real-time access would give people much more control and choice over the inflows and outflows of funds.

The ability to receive money in the form of digital currency may also have an outsized positive impact on savings. One of the biggest sources of savings for many Americans is G2P payments, whether tax refunds, stimulus payments, or child tax credits. Without having to account for delays and unpredictability, G2P payments received instantaneously and accessed ubiquitously as a digital dollar may simplify and facilitate savings decisions.

In addition, small business owners may find receiving business-to-business (B2B) payments from others in the small and medium-sized enterprises (SME) supply chain a particularly compelling use case for digital currencies. For example, SME merchants whose purchases are invoiced in a CBDC or private digital currency will likely want to invoice in the same currency to ensure they can easily make those purchases. Digital networks with private digital currencies can be particularly effective at yielding access and utility benefits, allowing for new possibilities for commerce.

Spend

Cash flow management (having the right amount of money at the right time) is key to maintaining financial health. To spend less than one’s income and to pay bills on time depends in part on the timely availability of funds. A mismatch of balances and payments can result in overdraft, insufficient funds, and/or late fees. The cost and inefficiencies of the payments system often manifest in the high fees consumers pay to use alternative financial services providers, such as check cashers ($2 billion annually) and small-dollar payday lenders ($7 billion annually), and when experiencing bank overdraft fees ($24 billion annually) in the U.S. The average American household pays nearly $250 in these types of fees every year. Moreover, when consumers incur these fees, it can greatly impact their credit eligibility and costs, which then compounds the negative impact on financial health.

While some criticize decisions and behaviors that lead to fees as a function of financial illiteracy or irrationality, extensive research has shown that cashing checks at check-cashers can, in fact, cost less than using the formal financial system and, consequently, represent an optimal and rational choice for some consumers. It can take three to four days for a check to clear in the bank after deposit, but consumers can use cash right away when using check-cashers, without being subject to overdraft fees. The fee structure transparency and instant access, compared with the opacity and timing uncertainty of traditional financial services, is partly why consumers are willing to pay high fees at alternative financial services providers.

Digital currencies could greatly reduce the incidence and cost of payment delays and associated fees – if a CBDC were designed to provide an alternative, real-time form of receiving income and paying expenses, and if private digital currency networks allowed instantaneous settlement. The overall cost of access may also diminish with these new digital assets, given efficiency and competition benefits, making spending more efficient and financial lives healthier. The money that was previously spent on fees and penalties could then be directed toward greater savings.

Save

Having sufficient liquid and long-term savings is key to building financial resilience and weathering shocks. However, 25% of Americans have no emergency savings. And, 69% of Americans are living paycheck to paycheck, meaning they would experience financial difficulty with day-to-day cash flow management if their paychecks were delayed, let alone saving for emergency or long-term needs.

For 30% of Americans, a tax refund is the single largest cash flow infusion in a year. Nearly half of Americans place some of their tax refunds into savings. Most households reported placing a significant portion of their COVID-19 stimulus checks into savings. Unfortunately, many of these G2P payments are highly inefficient. Approximately 35 million individuals had to wait months to receive their stimulus checks, if they received them at all. G2P payments delivered quickly and at scale via a digital dollar could make a dramatic difference, especially in times of disaster, such as a global pandemic or natural disasters.

G2P payments delivered as a programmable CBDC could be designated only for certain purposes (e.g., discounted groceries), to encourage tax-advantaged savings schemes, and/or to nudge consumers toward savings (e.g., automate savings as default).

The benefits of programmability would also apply to private forms of digital currency. Digital assets are already becoming a popular form of savings. The movement of money can be seamless, particularly when it relies upon an interoperable or harmonized network. The straightforward movement of money between payments and savings could incentivize greater savings behaviors.

Finally, interoperability between CBDCs, private digital currencies, e-money, cash, and commercial bank money will also be critical. Most people in America save their money in private banking institutions. CBDCs and private digital currency payment networks could help with money movement, but they don’t inherently offer a savings utility. Enabling people to easily move their money into savings will be crucial for digital currency networks.

Borrow

Having manageable debt and a prime credit score (660-719) or greater is key to a sustainable and healthy financial future. On-time payments are the single biggest factor affecting a credit score, which determines the options available and cost of borrowing. Typically, a payment must be 30 days late to affect credit scoring. But, as described with stimulus payments, G2P payments can be significantly delayed, which makes late payments more likely and, subsequently, increases the cost of borrowing. While a two-day delay in payment may not immediately impact a credit score, it could result in late fees, siphoning off funds that could be used to pay an outstanding bill that is 30 days late.

A digital dollar and private digital currency networks can help with reducing late payments due to the real-time nature of these new payment systems. To the extent that new forms of money interoperate with existing payment options, they may also lower the cost of borrowing by digitizing some of the payments currently made in cash, and generating a more complete and reliable record of payments that could provide more accurate measurements of creditworthiness.

Plan

Advanced financial planning is usually measured by the use of personal financial management (PFM) or budgeting tools, usage of “buckets” or savings accounts named for a goal, and presence of recurring transfers. If properly controlled and permissioned by the user, consolidated financial data – along with greater ease of fund movement enabled by digital currency – can facilitate greater visibility and unlock new options in financial planning. Mental accounting and budgeting could be made more tangible and actionable with greater transparency and less friction to plan for risks and needs. Free budgeting and financial management apps may be able to offer even more flexible and customized services, such as insurance and investment, in a world where financial services run on an interoperable CBDC and/or private digital currency networks.

Infrastructure Choices Will Implicate Financial Health

A CBDC infrastructure and private digital currency networks could reduce or even eliminate operational and financial inefficiencies, or other frictions, in payments, clearing, and settlement. Infrastructure choices will implicate consumer financial health, and therefore, will need to be made on the foundation of responsible innovation. Digital currencies’ potential ability to improve financial health for everyone will depend on their openness, and the transparency, speed, and ease with which retail consumers can access and move their money. During the pandemic, more than 40% of adults went without medical care due to their inability to pay. Had the economic impact payments arrived in time, perhaps many more people would have been able to seek medical attention and intervention when it was most critical.

CBDCs and private digital currencies, if designed, implemented, and regulated appropriately, could be a once-in-a-century infrastructure innovation that is both responsible and equitable. The largest opportunity lies in coupling digital currencies with other infrastructure updates, like digital identity. Financial services offerings are predicated on the ability of providers to perform Know Your Customer (KYC) due diligence and compliance with anti-money laundering (AML) regulations, which could be made easier by tiered digital ID protocols that could verify identity while protecting user privacy. A digital ID that can be authenticated remotely is key for access, inclusion, participation, and innovation in a digital economy, enabling delivery of a wide range of services that require proof of identity, whether by way of financial services, transportation, or education.

Programmability offers another exciting possibility: Logic could be embedded to perform electronic KYC and sanctions screening, ensure compliance, reduce fraud, and enable tokens or currencies to perform specific functions, such as paying a mortgage on a certain date.

For the above benefits of financial health to materialize, interoperability with existing options, provided by banks and nonbanks alike, is essential to achieving ubiquity and utility. The retail financial system has many actors – credit cards, personal and mortgage loans, payments, checking and savings, wealth management companies, insurance providers, and P2P transfers, just to name a few. For a digital dollar and private digital currencies to make a difference in consumers’ interactions with the financial system and improve financial health, the new assets need to be designed and instrumented to work with the existing system, plugging holes where they exist.

CBDCs and private forms of digital currency can provide more utility to consumers and deliver financial health benefits when financial services providers can build on their infrastructure. For example, P2P payments through new digital currency networks can become even more convenient if other instruments – such as prepaid debit cards on which paychecks are received – can be easily integrated into these new forms of money. Savings for short-term and long-term goals can also be automated and made more efficient if they are linked to digital currency payment networks.

The specifics around the operation of a CBDC or private digital currency network are far from settled, and the financial health benefits are not guaranteed. The choices that policymakers, technologists, and corporate leaders make when designing these new forms of money will determine whether digital currencies will deliver meaningful financial health benefits to consumers.