Strengthening Financial Health for Climate Resilience

Climate hazards have massive financial impacts on households, especially ones that are already struggling. What do they need to be financially resilient in the face of a changing climate?

“Without significant intervention, climate hazards are likely to cause compounding financial burdens for vulnerable households with fewer resources and limited ability to prepare for and recover from shocks.”11

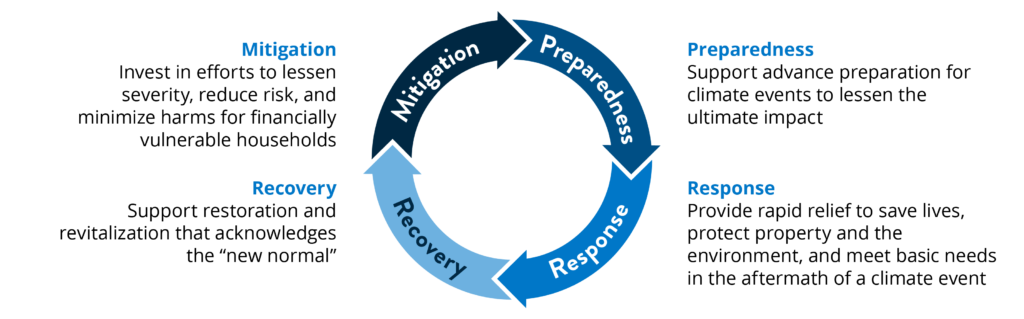

4 Pillars for Household Climate and Financial Resilience

To foster climate resilience, it is critical to strengthen financial resilience. In this brief, we explore what households need financially to be climate resilient. In particular, we focus on financially vulnerable households, which are disproportionately composed of people of color and those with low incomes.12 To understand the barriers and risks that vulnerable families face – and identify the solutions that could support them – we draw on a framework commonly utilized in emergency management. This framework conceptualizes the disaster lifecycle into four phases: mitigation (and adaptation), preparation, response, and recovery.13 These phases comprise four key pillars for building household climate and financial resilience.

Mitigation and Adaptation

Families need clear communication and guidance to help them evaluate risks, prioritize appropriately, and take action. Additionally, innovative financing structures and incentives can help lower cost burdens for vulnerable families and spur adoption of climate-friendly solutions. Community ownership models present another option for expanding access to green solutions.

Preparedness

Households would benefit from tangible, structured guidance that helps them plan ahead. They also need support to build the critical savings they may need during an emergency, and access to affordable insurance to protect their property.

Response

Families need immediate and accurate delivery of aid, along with trustworthy guidance that helps them navigate an overwhelming time. Financial institutions also play important roles and need to offer flexibility, adaptability, and rapid availability. For many families, maintaining employment and the income it provides is critical to make ends meet; employers can allow people to retain income by offering flexible remote or leave policies.

Recovery

Impacted households would benefit from hands-on guidance on how to file claims, access resources, avoid scams, begin longer-term planning, and implement mitigation and adaptation strategies. They also need rapid, hassle-free insurance payouts, access to affordable credit, and flexibility from financial service providers.

Thank you to the many Financial Health Network staff who supported the creation of this publication.

We are also grateful to the advice of other external experts who guided our thinking on this brief, including Danielle Arigoni, Hannah Kramer, Michelle Jones, Casey Bell, and Sarita Turner.

The Financial Health Frontiers initiative is supported by the Citi Foundation.

![]()

The findings, interpretations, and conclusions in this piece are those of the Financial Health Network and do not necessarily represent those of our funders or Advisory Council members.

Strengthening Financial Health for Climate Resilience

Explore the trends. Discover new insights. Build stronger strategies.