Pulse Points Spring 2023: Bracing for the End of Student Loan Forbearance

New analysis suggests that many borrowers anticipate difficulty restarting payments when forbearance likely ends this summer – but proposed policy changes could help.

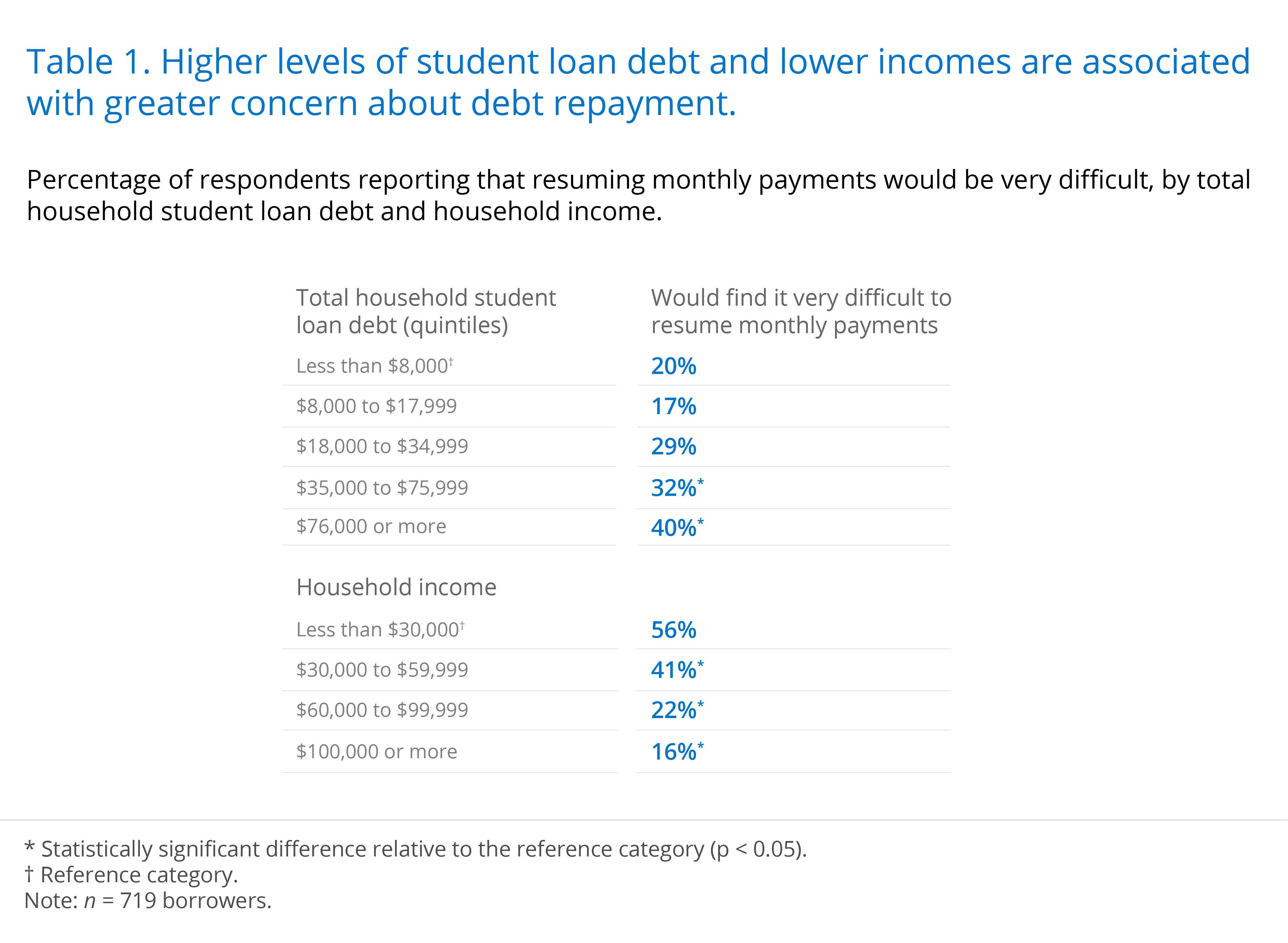

Over Half of Student Loan Borrowers Have Repayment Concerns

In the our most recent Financial Health Pulse survey, which was fielded between April 13 and May 15, 2022 (during forbearance but before forgiveness or IDR changes were announced), we asked federal student loan borrowers to tell us how much difficulty they would have making their monthly student loan payments in a hypothetical scenario where the payment pause ended “next month.” Respondents were asked to rate the level of difficulty on a 4-point scale, from “very easy” to “very difficult.”

Over half (59%) told us they thought restarting payments would be at least somewhat difficult, including 29% who said repayment would be very difficult. In early 2022, 43 million Americans had federal student loans subject to forbearance, meaning around 12.5 million borrowers would find it very difficult to make monthly payments.12

Borrowers with higher student loan debt balances and lower household incomes more frequently anticipated finding repayment very difficult. Those with total loan debt between $35,000 and $75,999 or greater than $76,000 more often anticipated difficulties with repayment. In addition, around half of borrowers with annual household incomes under $30,000 (56%) anticipated that repayment would be very difficult, more than three times as often as people with incomes over $100,000 (16%; see Table 1).

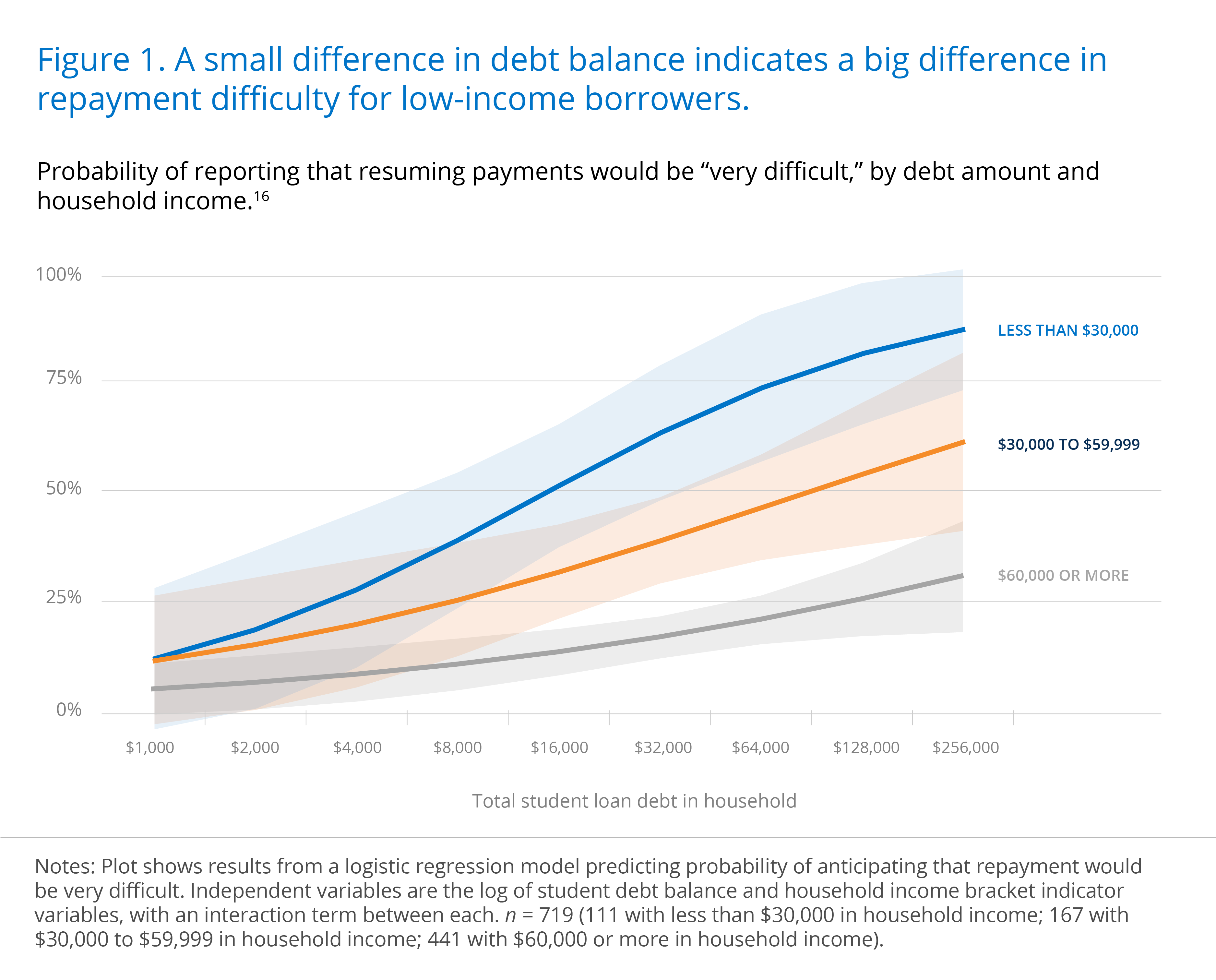

Small Differences in Student Loan Balances Are Associated With Bigger Repayment Concerns for Low-Income Borrowers

Using estimates from a model predicting repayment difficulty based on total student loan balance and annual household income, we find that the relationship between debt balance and difficulty differs for borrowers of different income levels. Starting at about $4,000 in student loan debt, those with incomes less than $60,000 begin to report higher levels of difficulty than borrowers with higher incomes. The difference between these lower-income groups and those earning $60,000 or more then widens as the amount of debt increases (see Figure 1). Put differently, we find that small differences in student loan debt balances are associated with larger differences in repayment difficulty for people with household incomes under $30,000 relative to those with household incomes above $60,000.14

Income-Driven Student Loan Repayment Plans May Be the Key to Supporting Borrowers’ FinHealth

IDR plans, which are targeted toward borrowers with low incomes and/or high debt balances, may help borrowers who anticipate struggling with repayment.

We cannot identify who is on an IDR plan in our data. However, we can roughly identify borrowers who would have lower monthly payments on an IDR plan by comparing their incomes to their student debt load in accordance with guidance from the Department of Education.15 We identify survey respondents whose debt balances are at least as large as their discretionary incomes (household income minus 1.5 times the federal poverty guideline for their household size) and note that they would likely have lower payments under IDR as currently designed. We also identify those whose discretionary incomes are less than $0 and identify them as borrowers who would owe $0 per month on an IDR plan.

Some of these likely IDR beneficiaries are already on IDR plans, but many are not. Prior estimates using federal student loan data show that about 30% of borrowers were on an IDR plan in late 2020.16 Yet, we estimate that around 49% of federal student loan borrowers would have lower monthly payments with an IDR plan, suggesting that approximately one out of every five borrowers (19%) would have lower payments under IDR but are not taking advantage of it.17 Further, we estimate that 16% of federal student loan borrowers in our data would owe $0 per month on an IDR plan.

Borrowers who anticipated struggling with repayment are poised to benefit from IDR at an even higher rate: 7 in 10 struggling borrowers (71%) would likely owe less on an IDR plan than on a standard repayment plan, and over one-fourth of borrowers who anticipated that repayment would be very difficult (27%) would owe $0 per month if they were on an IDR plan. The fact that borrowers who anticipate struggling to repay their student loan bill would owe $0 under IDR suggests that many borrowers who need IDR most are not utilizing it (see Figure 2). Another 44% would still owe some amount per month, but less on an IDR plan than a standard repayment plan.

In addition, the majority of borrowers with household incomes under $30,000 (83%) – a group who anticipated difficulty at much higher rates – would not owe any monthly payments under IDR (analyses not shown). Thus, the high rates of repayment difficulty experienced by the lowest-income borrowers could be meaningfully reduced via increased IDR enrollment, aligning with prior research suggesting that many low-income borrowers would benefit from switching to IDR and that the lowest-income borrowers are actually less likely to be on IDR plans than moderate-income borrowers.18, 19

Under the Biden administration’s proposed changes to IDR, borrowers’ repayment difficulties will likely lessen. If implemented, we estimate that the number of borrowers owing $0 per month under IDR will grow from roughly 16% to 27% as guidelines would shift from defining discretionary incomes as 1.5 times to 2.25 times the federal poverty rate. The new regulations could also improve IDR takeup among the most at-risk borrowers by automatically enrolling those who are 75 days delinquent on payments into an IDR plan.

Written by

-

Manager, ResearchFinancial Health Network

Manager, ResearchFinancial Health Network -

Director, Policy and Research

Director, Policy and Research