Buy Now, Pay Later: Implications for Financial Health

In this brief, we leverage findings from a nationally representative survey to better understand the buy now, pay later (BNPL) market, the users who are driving it, and the implications for their financial health.

BNPL Is a Modern Twist on Payment Plans

Buy now, pay later offers point-of-sale loans that allow consumers to pay for online or in-store retail purchases over a set period, typically four payments over six weeks. These loans allow consumers to purchase products immediately and pay only a portion of the cost upfront.

Deferring payment is not a new concept; rather, BNPL is an updated approach to payment plans such as layaway, rent-to-own, and other retail installment programs. BNPL loans, however, have gotten a fintech refresh and are typically offered by third-party companies through an online application during checkout.

The BNPL landscape is rapidly changing. Companies offering BNPL services include Affirm, Afterpay, PayPal, Sezzle, Zip, and Klarna; numerous banks, payment processors, and other firms have also entered the game in recent months. During the 2021 holiday season, BNPL was nearly ubiquitous at online retailers.

Though the dominant BNPL product has a pay-in-four model, several providers offer repayment options varying in terms, number of payments, interest, fees, and more. This and BNPL’s semblance to other installment products have made defining and measuring the market particularly challenging.

As part of our 2022 FinHealth Spend Report, which analyzes fees and interest paid by consumers on dozens of everyday financial services, the Financial Health Network fielded a nationally representative survey in November 2021, querying 5,033 households about their use of a wide range of financial services, including BNPL. The FinHealth Spend survey explored three types of BNPL services, which we defined in our questionnaire as follows:

-

- Short-term financing with no interest (these are typically less than six months and often follow the pay-in-four model).

- Financing with repayment periods of six months or more, with no interest.

- Financing with repayment periods of six months or more, with interest assessed.

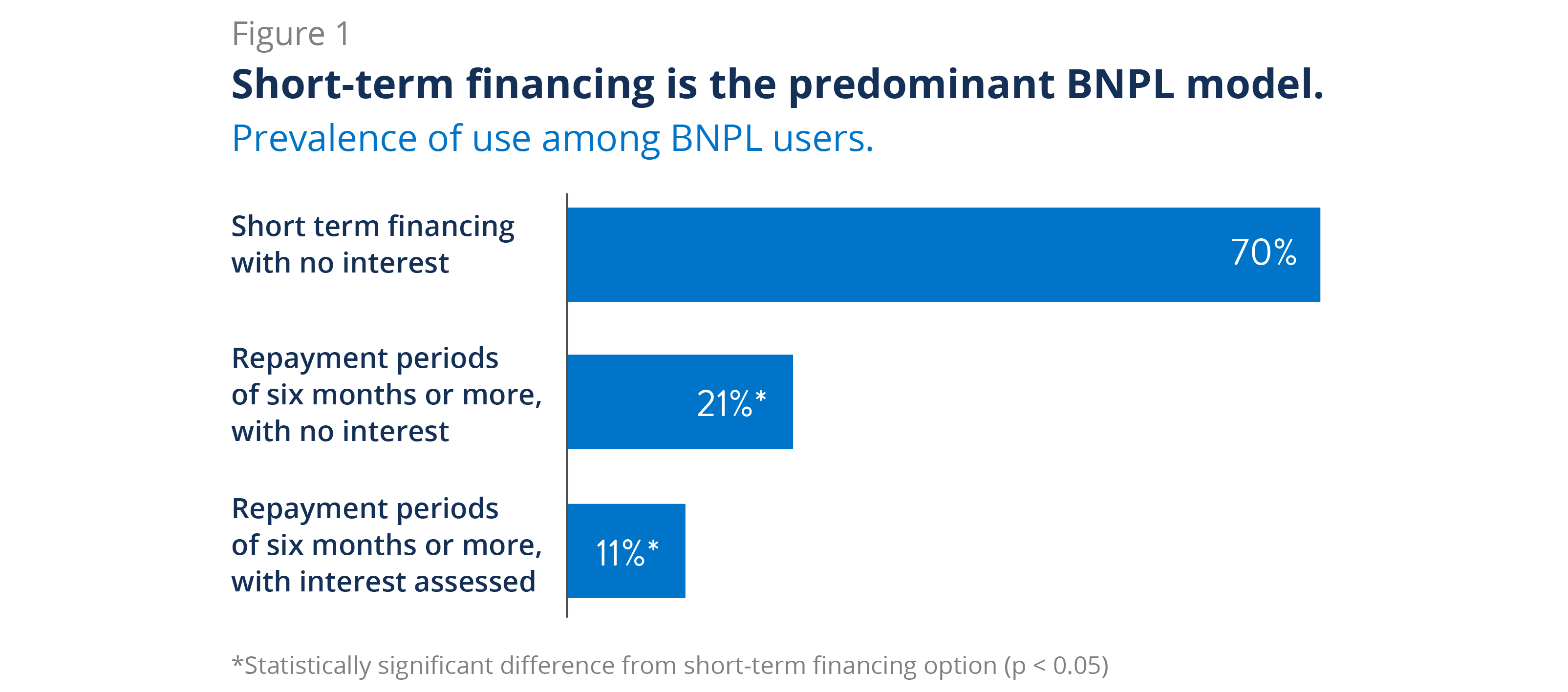

Our survey found that approximately 10% of households in America used BNPL in the 12 months prior to November 2021.⁴ Of these, the vast majority of BNPL users (70%) used a service that offered short-term financing with no interest (Figure 1). About one-fifth (21%) reported using longer-term, no-interest models, while only 11% said they used a BNPL service that applied interest.⁵

Younger and Less Financially Healthy Households Are More Likely To Use BNPL

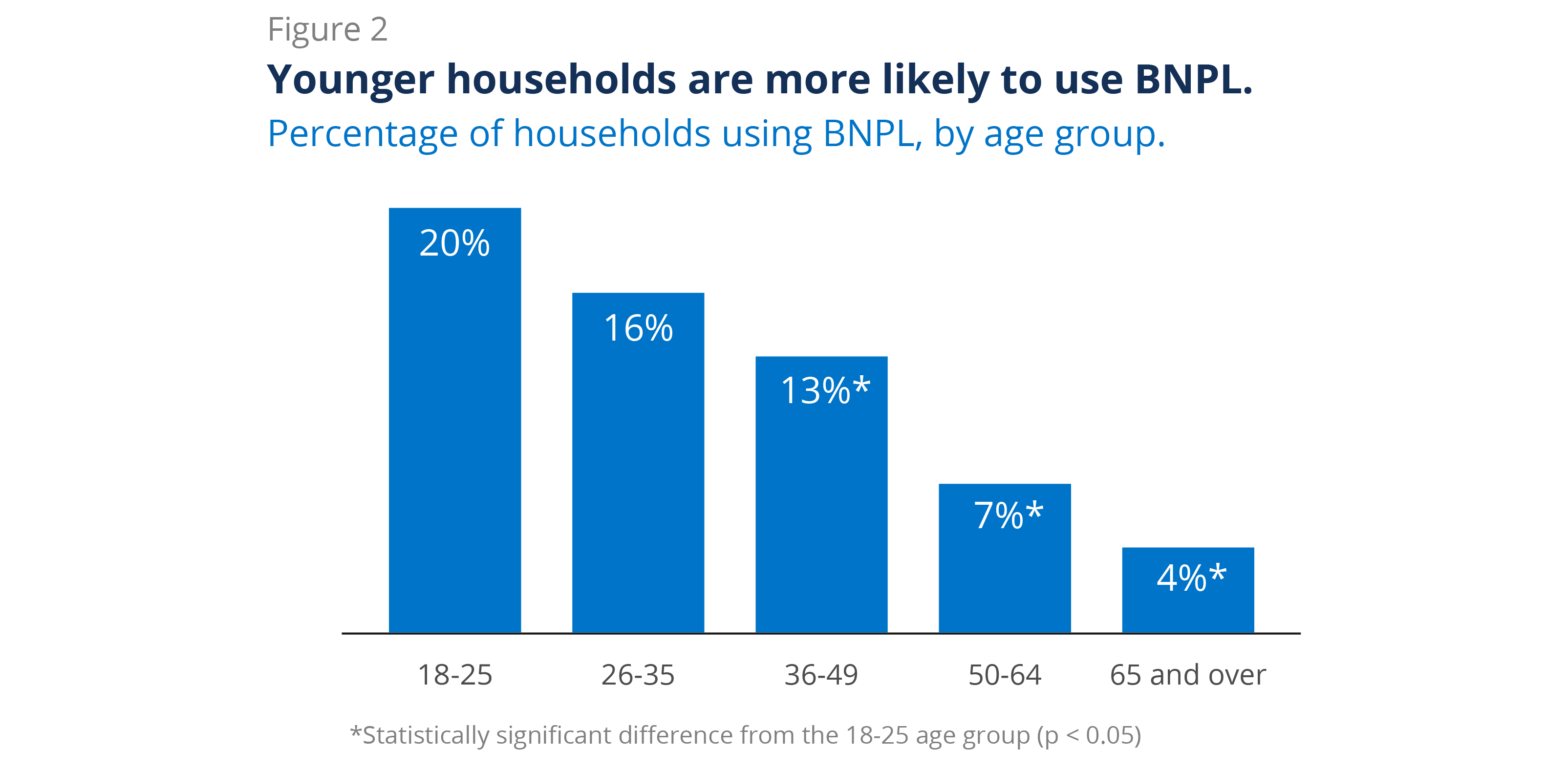

Previous research on the growing BNPL market has shown prevalence among younger generations – particularly millennials and Generation Z – who may be looking for a tech-friendly alternative to credit cards.⁶

Indeed, our survey found that 20% of respondents 18-25 reported that they had used a BNPL service in the last 12 months, compared with 16% of respondents 26-35 and only 13% of respondents 36-49 (Figure 2).

Latinx respondents are nearly twice as likely to turn to BNPL than White respondents: 16% of Latinx households report having used BNPL in the 12 months prior to November 2021 – as have 12% of Black households – compared with 9% of White households.

Importantly, our data show that BNPL users are less financially secure than nonusers. Financially Vulnerable households are those who struggle to spend, save, borrow, and plan, according to the FinHealth Score® measurement framework. As opposed to Financially Healthy households, Financially Vulnerable households struggle in almost all areas of their financial lives. Financially Vulnerable households are nearly four times more likely to use BNPL than Financially Healthy households (18% vs. 5%). Additionally, 24% of households that reported using BNPL are considered Financially Vulnerable, compared with 13% of households that don’t use BNPL.

BNPL users are also more likely to struggle with credit. Nearly half of BNPL users (43%) report having subprime credit scores, compared with 24% of nonusers.⁸ Additionally, BNPL users who hold credit cards are more likely to have outstanding credit card debt: 77% of BNPL users who also have credit cards say they have carried a balance on their credit cards over the past year, compared with 49% of nonusers. Interestingly, 23% of BNPL users and a similar percentage of nonusers (26%) do not use a credit card.

Nearly One-Third of BNPL Users Report Increased Spending

No-interest BNPL products offer consumers the benefit of deferring payment on a purchase at no additional cost. This can provide consumers more purchasing power and a convenient short-term repayment mechanism. It could also help them avoid incurring additional revolving credit card debt.

However, if BNPL induces consumers to overspend their budget and take on net additional debt, even at 0% interest, this could have a negative impact on savings, borrowing, and, ultimately, financial health. Among BNPL users in our survey, 30% said they spent more than they would have if BNPL had not been available to them at the time of purchase (Figure 3). Further, when asked what payment method they would have used had BNPL not been available, 34% of BNPL users responded that they would not have made the purchase at all (Figure 4).⁹ Taken together, 47% of users said that the availability of BNPL led them either to make a purchase they otherwise would not have made or to spend more than they would have without BNPL.

This suggests that while in some cases BNPL may act as a stand-in for credit or debit card purchases, in other cases BNPL may have triggered purchases or incremental spending outside consumers’ normal spending patterns.

About the FinHealth Spend Report

The FinHealth Spend Report, previously known as the Financially Underserved Market Size Study, is one of the Financial Health Network’s longest-running research initiatives. The report analyzes household spending on dozens of financial products and services, leveraging extensive secondary research as well as a nationally representative survey on consumer spending. Through this initiative, we gain insight into the impact that interest and fees have on families in the United States and uncover disparities in our system.

The Financial Health Network collaborates with the University of Southern California Dornsife Center for Economic and Social Research to field the FinHealth Spend survey to its online panel, the Understanding America Study.

The FinHealth Spend Report is made possible through the financial support of Prudential Financial.

![]()

Written by

-

Senior Manager, Financial Services SolutionsFinancial Health Network

Senior Manager, Financial Services SolutionsFinancial Health Network -

Policy & Research Advisor

Policy & Research Advisor -

Manager, ResearchFinancial Health Network

Manager, ResearchFinancial Health Network

Buy Now, Pay Later: Implications for Financial Health

Explore the trends. Discover new insights. Build stronger strategies.