By John Hammond, StartU

Today marks the 3rd annual #FinHealthMatters day; an event started by the Center for Financial Services Innovation to draw attention to the 57% of Americans — approximately 138 million adults — that are struggling financially today. This year’s theme is student health; emphasizing the financial health of college students in America today.

At StartU, this is an issue we are confronted with regularly. It’s important to keep in mind that many of the founders we feature are trying to launch a business while also footing the bill for a $200,000 degree. As you can imagine, this is a dangerous recipe.

As VP of Wharton’s personal finance club, I have an innate appreciation for events calling attention to student financial health. Not just for founders, but for the nearly 75% of students not sure they could come up with $1,000 within the next month if an unexpected need arose. So I looked into how the student loan process works (disclaimer: it’s confusing) and came with 3 tips on how to manage your student debt while trying to start a business — or a life.

1. Educate yourself (because they don’t teach you this stuff in school)

In case you’re not already familiar with the student debt crisis in America today, here’s a quick summary:

Clearly, things are not great….and they’re getting worse. Rising interest rates, tuition, and student populations are causing student debt to grow by roughly $230 million every-single-day.

So what’s this look like for your average individual?

Average college students, roughly 70%, graduate with $37,500 in student debt; equating to about a $350 monthly payment. If this seems manageable to you, know the reality is far different.

The effect is compounding. Your student loan debt correlates to higher interest rates for other financial products like a mortgage or auto loan and ultimately, a higher total cost of ownership in the end. On average, students take nearly 19 years to pay off their loans; significantly delaying their abilities to begin life post-graduation.

Students’ struggles largely stem from a poor understanding of how their loans will actually function. The first step every borrower needs to take is educating themselves on their specific funding needs and what to expect from the loans they do take out.

- Know what your monthly payment will be

- Know if your interest rates are fixed or variable

- Know whether or not your loans are accruing interest while you are in school (subsidized vs. unsubsidized loans)

- Know if you have the option to refinance

Websites like studentloanhero and nerdwallet provide tons of great information around how student loans work in an easily digestible format.

If educating yourself on these topics seems daunting, just reach out to your school’s financial aid office. Most universities will help students (and alumni) figure out the answers to these questions.

2. Don’t take out more loans than you need to

Doy!

Here’s the approach most students take when acquiring their loans:

- Step 1: Look up whatever the university projects as the overall annual budget (tuition + cost of living, etc.)

- Step 2: Get a loan for that full amount

- Step 3: Be in debt for the next 20+ years

Click, click, boom. When the government approves everyone’s loan applications, drowning yourself in debt is scarily easy.

That’s why every student needs to define their specific funding needs before taking out loans. Look up the expenses your university projects and go line-by-line to see whether or not they line up with your reality. Wharton’s budget include $5,700 for projected “transportation” expenses; not sure if my classmates are flying first class or what, but that’s definitely not my reality.

After calculating your specific funding needs, explore alternative sources of funding. Figure out just how much the cost of education you can fund outside of loans. Whether it’s breaking open the piggy bank, asking for a personal loan from mom and dad, or applying for grants and scholarships; anything interest free is key. Leave yourself some cash in case of emergencies, but the more interest free funding you can acquire the better.

Which brings me to me final point…

3. Start paying down your loans as early as possible (ideally while in school)

Sound bold? Bare with me.

The single largest gap I’ve seen in students’ understanding of their loans is the level of magnitude with which accruing interest impacts their loan repayments.

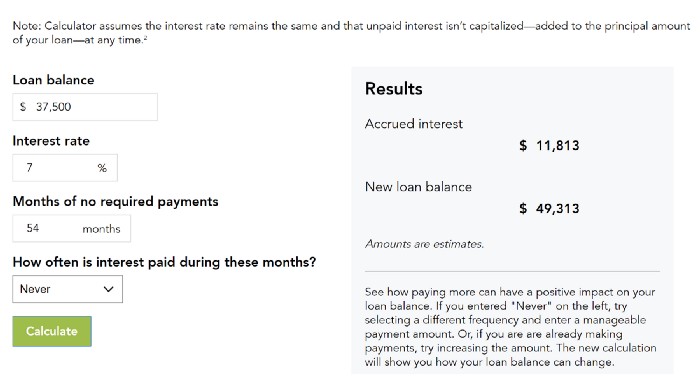

Put it this way, we said the average student graduates with $37,500 in loans earlier, right? Well that number is only a portion of what you actually end up paying. Depending on federal loan interest rates, you’ll wind up paying between ~$47,000 and ~$52,000 total and this only if you make every payment on-time and in full — which may be idealistic.

So basically, take your original loan balance and tack on about an extra 40% to get the total amount you’ll end up paying in the end.

Are you depressed yet?

Don’t worry, there are ways for you to mitigate this insidious interest. The biggest one being to simply start making payments as early as possible. Interest payments are based on the principal amount of the loan you take out. Lower your principal = lower your interest = lower your total payment.

That’s why it’s so important to know whether or not your loans are accruing interest while in school. Chances are, at a least a portion of them will be.

Consider the following example, $37,500 taken out in your freshman year turns into nearly $50,000 by the time you have to start making payments if you are accruing interest that entire time.

But obviously students are strapped for cash, especially ones that are trying to start their own business. You may simply not be able to pay down this interest while in school or afford to put much cash aside as prepayments. This is understandable. Just know that every early payment you do make has an exponential effect. A simple $30-$40 dollars every month before you graduate or on top of monthly payments after you graduate goes a long way.

Still, I know that the vast majority of students aren’t going to do this.

Most students just don’t have the discipline, motivation, or stomach to log on every month and throw a few bucks at their seemingly overwhelming loan balances on a consistent basis. Honestly, I don’t blame you — I have trouble just looking at my credit card statement.

Luckily, there are now some startups that will do this for you. Consider the new FinTech startup Chipper, for example. Their application rounds up your daily transactions and contributes the aggregate towards your student loans every month. Think Acorns but for paying down your student debt faster.

Chipper: A new startup focused on student lending

Chipper: A new startup focused on student lending

How Chipper Works

How Chipper Works

The average student loan can end up costing you more than double what you originally took out if you stick to the minimum payments every month.

You can save over $6,000 and shave 4 years off your repayment period if you make additional payments regularly. But budgeting for this isn’t easy.

Chipper makes this effortless by rounding up your everyday purchases to the next dollar and setting aside your spare change for principal payments.

These are the type of services student borrowers need. It makes loan repayment easier, faster, and more efficient with minimal required effort. All users have to do is download the app, link their accounts, and let Chipper handle the rest.

Current students can also take advantage of this service before payments on their loans are due. In fact, they stand the most to gain. According to Chipper, students who use Chipper for all four years will walk across stage at graduation with 33% less debt simply by rounding up their everyday transactions while in school.

Chipper is preparing to launch in May. As a promo, the company will pay $5 toward your loan if you signup for early access and it’s completely free to use for students.

Can you guess who’s been on the wait-list for months? (it’s me).

To summarize:

Follow these steps while trying to wrestle with the costs of starting your own business on top of the mountain of debt your school is charging you. All borrowers, not just founders, would benefit from the following:

- Educate yourself on how the student lending process works, what your specific loans terms mean, and how this will impact your paycheck after graduation.

- Don’t take out more loans than needed by projecting what your personal expenses will be and exploring interest-free sources of funding (e.g. personal loans from family/friends, grants/scholarships, etc.)

- Begin paying down your loans as early as possible (ideally while in school). Combating accruing interest is the single biggest step borrowers can take towards reducing their overall debt burden. New companies like Chipper are making this easier than ever before.

Each of these tips are things I wish someone had told me as I was navigating the student lending process. My hope is that #FinHealthMatters day brings awareness to the struggles students are current dealing with as a result of their debt along with actionable solutions to plan for and manage their future financial freedom post-graduation.

If more attention is paid, more guidance may be given, and we may actually begin to respond to the Student Debt Crisis in an effective manner.

This blog post originally appeared April 25, 2018 on StartU as a part of Financial Health Network’s #FinHealthMatters Day. To learn more about FinHealthMatters from Financial Health Network, sign up here.

*All views and endorsements expressed in this blog entry are solely those of the author and do not necessarily reflect the views or endorsements of Financial Health Network.