“We tend to spend when the checking account balance is high so I like being able to put in money when I need it, it’s more flexibility. I like the idea of having a buffer account that I can feed into my checking account. I get more control of my finances.” — Matt, Current Payroll Card User

Matt’s experience is an example of how financial products can be a force for good in consumers lives and Financial Health Network believes that providing consumer tools like high quality payroll cards can also improve the bottom line for providers and employers. A payroll card refers to a prepaid card provided by an employer that the employee uses to receive his or her wages each payday. To better understand whether employees are deriving value from these products and how that impacts card usage, Financial Health Network conducted first-of-its-kind in-depth quantitative and qualitative research on this topic. Payroll cards may be perceived as simply a transaction tool to replace cash or checks for low-income employee wages. In Making Payroll Cards Work for Employees, Financial Health Network busts that perception and demonstrates that when the quality of payroll cards improve, diverse consumers benefit and providers experience more engagement and activity on their products.

Myth 1: Payroll card users are primarily low-income consumers

There is a perception that payroll cards are only used by low income employees or hourly-wage workers, but Financial Health Network’s quantitative research found that there is a fairly even distribution of payroll card users across the income spectrum; and notably 16% of payroll card users report an income above $100,000. Qualitative insights indicate that payroll card users also hold a wide range of occupations, from an IT director at a software company (annual income above $100,000) to a sales rep for trade shows (annual income of $60,000 — $99,999) to a home care aide who cleans, cooks, and provides personal care for the disabled and elderly (annual income under $30,000). Payroll card users today clearly come from a range of industries, backgrounds and incomes.

Myth 2: Payroll card users are ‘unbanked’ consumers

Payroll cards have commonly been viewed as an electronic payment option for those employees who do not have access to a traditional bank account for direct deposit, but the data paints a more nuanced picture. In Financial Health Network’s sample of payroll card users, weighted to be nationally representative, 84% own a checking account, and 74% have a debit card linked to their checking account. Not only are these consumers ‘banked’, but they are actively choosing payroll cards over other forms of electronic wage receipt. Of those consumers who perceived a clear choice in whether to receive a payroll card, 85% were also offered direct deposit. The large, overlapping population of payroll card users who both own a checking account and were offered direct deposit by their employer indicates that many employees had an available, comparable traditional financial option, but chose a payroll card. Our research indicates that this active choice of payroll cards above other products is potentially driven by the combination of ease, and cross-functional potential, of the cards.

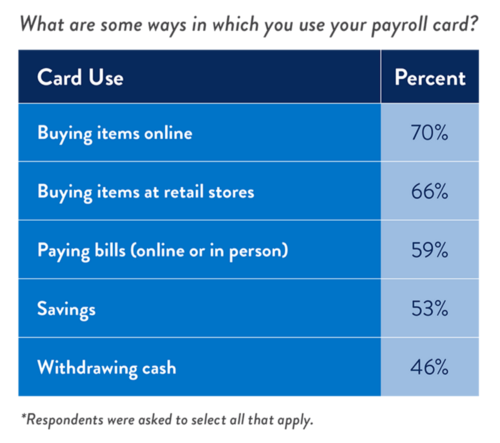

Myth 3: Payroll Cards are only viewed as a transaction product

Financial Health Network found that many payroll cards users, like Matt, use this product for much more than simply receiving and spending pay. Financial Health Network performed a cluster analysis with the quantitative data to reveal trends in payroll card users’ experiences, habits, and preferences and identified a segment of consumers that interact with their payroll cards in diverse ways to serve their financial needs. 26% of the payroll card sample were categorized as ‘Engaged Users’. These consumers leverage the card for budgeting by only spending money from their card for a distinct purpose, and for saving by leaving a certain amount on the card each pay period for a rainy day. The segment of users who leverage their payroll cards for financial needs beyond just transacting also expresses the highest levels of satisfaction with the product.

What this means for employers and providers

Employees are seeking payroll cards to help manage their financial lives, which in turn can improve their financial health. Financial Health Network’s report, Employee Financial Health: How Companies Can Invest in Workplace Wellness found that poor employee financial health can increase absenteeism, increase health insurance claims, prompt employee turnover and employees dealing with financial matters on the job alone could cost employers $7,000 per employee per year. Increasingly employers are understanding that investing in the wellness of their employees is an important part of company performance, of recruiting success, and other factors.

For providers, payroll cards are an opportunity to serve a diverse set of consumers and increase customer engagement. Consumers who leverage their payroll cards across many financial functions are more likely to keep funds on their card, and use the product more actively. By delivering high quality payroll cards that appeal to many different consumer needs, providers have an opportunity to increase the number of consumers that take up the product, as well as increasing the volume of transactions and funds stored. “It’s a comforting, reliable instrument. I know it’s going to be filled up at a specific time, without fail. It’s never wrong. I have a close relationship with that pay card. I think of it as, it’s sort of like your whole career in your hand right there. It all comes down to this.” — Vera, Current Payroll Card User

What Employers and Providers can do

Employers have an opportunity to understand and champion the financial health of their employees. Fifty-eight percent of employers are already offering employees some help with at least one component of financial wellness. Receipt of pay is one of the cornerstones of the employer-employee relationship and high quality payroll cards enable employees to insert more control and ease into their financial life. When offering payroll cards employers must ensure that employees have a clear choice in whether or not to receive the product, and that clear and easily accessible information and support are provided.

Providers should work closely with employer partners to ensure that clear information are provided for payroll cards. High-quality printed materials and online reference tools about payroll cards can help consumers understand that they have a choice, and enable them to select the payment method that works best for their day-to-day financial systems. Providers should also focus on designing multi-functional payroll products, with strong digital functionality, that appeal to a diverse set of consumers.

As the design and delivery of the card continues to improve, consumers will engage more with the product, which can improve their day-to-day financial management and reduce workplace stress, while also increasing funds maintained on the card and transactions performed with the card. More information about who the payroll card user is, and how they derive value can be found in Financial Health Network’s report Making Payroll Cards Work for Employees.