Innovating Against Predatory Lending Products

A majority of American payday loan borrowers make less than $30k per year and end up on average paying $520 in fees to borrow $375 over five months. Learn how DailyPay is innovating against predatory lending products.

Presented by DailyPay

*This article was sponsored by DailyPay. All views and endorsements expressed in this article are solely those of the author and do not necessarily reflect the views or endorsements of the Financial Health Network.

![]()

With most workers living paycheck to paycheck and yet being paid only once or twice a month, unforeseen events between getting paid can be devastating, especially since more than half of all Americans cannot cover a $1,000 emergency with savings. For financially vulnerable people, existing options are expensive and extremely limited compared to people with higher incomes and more savings. Despite decades of difficult and important work on this issue, the market that many are left turning to is controlled by predatory lending products. This is why payday loans and bank overdrafts are used by so many to make ends meet, and lawfully permitted, despite the exorbitantly high interest and other charges to individuals and families who can afford them the least. Unfortunately, today predatory lending products are only getting more expensive. They also now layer on top of each other to cause a multitude of interconnected financial problems for people.

Public-sector and private-sector solutions are needed to combat this crisis that will not get better on its own. In the private sector, financial technology companies over the past several years have developed an extremely low-cost or free non-credit alternative for those frequent overdrafters and payday loan borrowers. Encouraging this industry’s expansion with smart, thoughtful safeguards is an important solution to dismantling our nation’s predatory financial systems.

But there is no silver bullet in this fight. Despite a number of banks reforming their overdraft fee policies due to public pressure, the average fee is still $35. Meanwhile, payday loan fees have been increasing despite bipartisan support to ban these products in 18 states. A majority of payday loan borrowers in America make less than $30,000 per year and end up paying $520 in fees on average to repeatedly borrow the same $375 over five months. When initially borrowed, payday loans are theoretically intended to be paid back whenever the borrower’s next paycheck arrives – in two weeks or one month. But research has shown that 4 out of 5 borrowers re-borrow their loans when they come due because of high interest and other charges. These fees get so high that 1 in 4 borrowers re-borrow their $375 loan nine times before paying everything back.

The $520 in payday loan fees assumes zero late fee charges, so the total is almost definitely more1. This number also does not factor in potential bank overdraft fees if the storefront lender uses the Automated Clearing House (ACH) network to directly deposit the loan and recoup payments. Today almost all storefront lenders operate this way, so if a borrower has insufficient funds when a minimum payment is requested, an average overdraft fee of $35 can be assessed by the borrower’s bank.

And it gets worse: According to the Center for Responsible Lending, the average fee charged by online payday lenders is even higher and for less money than their analog predecessors, with $793 in fees for a $325 loan2. This fee average also assumes no late fee charges or bank overdrafts over the course of five months. For these reasons, the amount of fees is likely a staggering $800 or more over five months to borrow just $325 from an online payday lender. This is an unconscionable amount of wealth to pull out of families and communities that are earning the absolute lowest incomes in this country.

Online payday lenders can only debit for repayment, which presents a host of additional problems. A 2016 Consumer Financial Protection Bureau (CFPB) study reported that a disturbingly high 42% of borrowers’ bank accounts had at least one failed repayment attempt3 by their lender due to insufficient bank funds4. These borrowers then had an average of $185 in overdraft fees charged to them by their banks5. But what’s worse is that the CFPB found that 74% of these borrowers’ bank accounts were closed within the 18-month duration of the study’s research6. The average time between failed deductions and account closure showed how these loans and their excessive fees played a direct role in account closures, how loan repayments failed because accounts were already headed towards closure, or both.7

Newer research is needed since the time of the CFPB study, but the high interest and other charges for such small amounts of money is too much to ignore. It is why wide bipartisan support exists to ban payday loans. But despite 18 states doing so and another six curbing certain lending activities, the owners of these predatory products made record profits during the worst year of the pandemic, and as many as 12 million Americans are still estimated by the CFPB to use them each year. Physical locations of payday lenders alone are still quite ubiquitous. A recent study by the CFPB found 14,348 payday loan storefronts in the United States.8 By comparison, this is about the same number of Starbucks locations throughout the country and slightly more than the 14,027 McDonald’s locations. What’s most troubling, but not surprising, is that payday lenders operate predominantly in communities populated by people who can least afford their excessive fees.

When the data above is considered, it is hard to comprehend why payday lenders are allowed to operate at all in this country or even why anyone would willingly choose to use these products. But when a borrower needs money quickly to pay a bill or for child care, a $15 fee for every $100 borrowed doesn’t sound so bad until the multiplying starts to occur.

Some bills just cannot be paid late, or can only be late for so long. According to a recent report by ABC News, Americans paid a combined $561 million in late payment fees to electrical utilities alone in 2019. While these late fees range from roughly $5.80 to $17.50, when accounts are not up to date, electricity can be shut off and not returned until an account is paid back down to zero.

Child care payments also rarely match a payroll schedule. But whether it’s a daycare center or an individual caregiver, for working parents, this is typically the last expense they can afford to pay late. Without being up to date on child care payments, working parents can’t work.

But when predatory lending still pervades the market, an “all-of-government” approach is needed to fix the layered systematic problems in law and in practice. This must be combined with an “all-of-the-economy” approach – a financial innovation “space race” that reconsiders the unwritten rules of money that still limit people’s access to their own money when they need it most.

Bold government action is an important part of this process. The path and outcome of strong political leadership like the Overdraft Protection Act, which was introduced by Democratic Congresswoman Carolyn Maloney of New York and received a hearing in March 2022, is unclear. The future of the Veterans and Consumers Fair Credit Act, which would cap all lending at 36%, is even more uncertain, despite bipartisan support in the U.S. House. We understand that, by design, legislation requires compromise to get things done. But people need help now.

Fortunately, in the last few years, select financial technology products have begun providing affordable alternatives for people without adequate savings. Extremely inexpensive earned wage access (EWA) providers and neobanks with generous overdraft policies would likely be popular even without today’s overlapping crises, but both are in such high demand because of the pain created by predatory lenders.

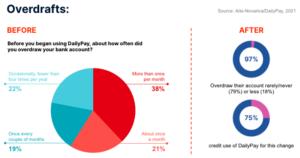

Recently, DailyPay commissioned a study with the Aite-Novarica Group, an independent research and advisory firm specializing in consumer protection in the technology and financial services industries. Aite-Novarica studied more than 1,000 DailyPay users and after their work, they found significant payday loan relief: Ninety-five percent of DailyPay users who had been using payday loans stopped doing so either completely (81%) or less frequently (15%) once they gained access to the DailyPay platform; eighty-eight percent of those DailyPay users credited the platform for this change. The Aite-Novarica Group conservatively estimated that these frequent payday loan users save between $624 and $930 annually by using this low-cost substitute.

Aite-Novarica’s research also conservatively estimated $660 or more in annual savings for those that previously overdrew their bank accounts regularly. Ninety-seven percent of these users report they now either rarely or never overdraw their accounts (79%), or they say their occurrences of overdrafting have lessened (18%). Three-fourths of respondents attributed this relief to the use of the on-demand payroll platform.

Additional research is needed to assess more than just DailyPay’s users, but when deployed responsibly as with DailyPay’s platform, employer-integrated earned wage access is an incredibly useful tool for people who otherwise lack affordable access to the money they’ve already earned. Innovations like earned wage access and technology-enabled overdraft protection, together with new consumer protection laws and thoughtful enforcement of existing ones, are an important part of the solution to the problems caused by predatory lending products and overdraft.

Today, we are at an inflection point: The right fintech products and services are opening doors to affordable financial products and services for more people than ever before. Earned wage access, particularly when provided in a low-cost, verified employment environment, builds a bridge to the equitable financial future so many have been working toward. We continue to stand with all like-minded allies in this battle against the billions of dollars charged to Americans by predatory lenders each year, and we welcome all other government and industry partners to join us.

1See Payday Lending in America: Who Borrows, Where They Borrow, and Why, the Pew Charitable Trusts, 2012, Page 41, Footnote 24.

2 Id.

3 See Online Payday Loan Payments, By the CFPB, April 2016, Page 23 of the Report.

4 Similarly, in March 2022, research by Morning Consult found that 1 in 5 users of Buy Now Pay Later financial services missed a payment in January 2022 and 1 in 3 overdrafted their bank account.

5 Id. at page 3.

6 Id. at page 23.

7 Id.

8 See Consumer Financial Protection Bureau Releases Notices of Proposed Rulemaking on Payday Lending; Payday, Vehicle Title, and Certain High-Cost Installment Loans (page 12). February 2019.