Pulse Points Summer 2021: The Impact of Stimulus Payments and Reopening the Economy

From April 1 to June 30, 2021, Americans balanced saving and new spending opportunities, with minimal changes in earned income.

Liquid savings balances stop climbing as people spend stimulus funds.

The historic growth in liquid savings balances that dominated headlines and wallets in the first quarter of 2021 ceased during the second quarter. The year began with the disbursal of two stimulus payments, in January and March, which tipped the personal savings rate to 26.9% in March 2021, according to the U.S. Bureau of Economic Analysis. During the second quarter, people began spending down those payments and returned to more normal savings activity with a monthly savings rate of 9.4% by June 2021, which remains higher than the pre-pandemic rates that hovered around 8%.

In the Pulse transactional data, this change in savings behavior is visible in median liquid balances. Balances in liquid accounts grew 29.9% in the first quarter of 2021 when people received their stimulus payments. Then, during the second quarter, liquid balances began to fall back down. Still, June balances ended 10% higher than January balances, giving individuals incremental liquid savings buffers for emergencies or additional spending.

Balances in Liquid Accounts in Q1 and Q2

Balances rose throughout Q1 alongside stimulus payments and tax refunds. Balances fell somewhat in Q2 but remained higher than the start of the year.

This line graph shows balances in liquid accounts between January and June 2021. Source: Pulse Transactional Dataset (Jan. 1 to June 30, 2021). Sample size: 323 individuals. Notes: Liquid accounts include checking accounts, savings accounts, prepaid cards, money market accounts, and cash management accounts. See Methodology section below for additional notes.

Post-stimulus spending declined, except in recreation and travel.

Overall spending in the second quarter of 2021 slowed from the boom that had accompanied the disbursement of stimulus payments beginning in January and March 2021, as seen in our Spring 2021 Pulse Points. Consumer sentiment, which began the quarter at its highest rate since the pandemic began, fell once more as people continued to adjust their expectations about prospects of an economic recovery over the summer of 2021. Amidst the lack of confidence and the lack of additional stimulus payments, spending was 8.8% lower within the Pulse dataset at the end of June compared with the start of the quarter. In the middle of the quarter, the economy also saw spending level off, too. The U.S. Bureau of Economic Analysis found that overall personal consumption expenditures levelled off from major growth of 5.2% in March, fell by 0.1% in May and recovered by 1% in June.

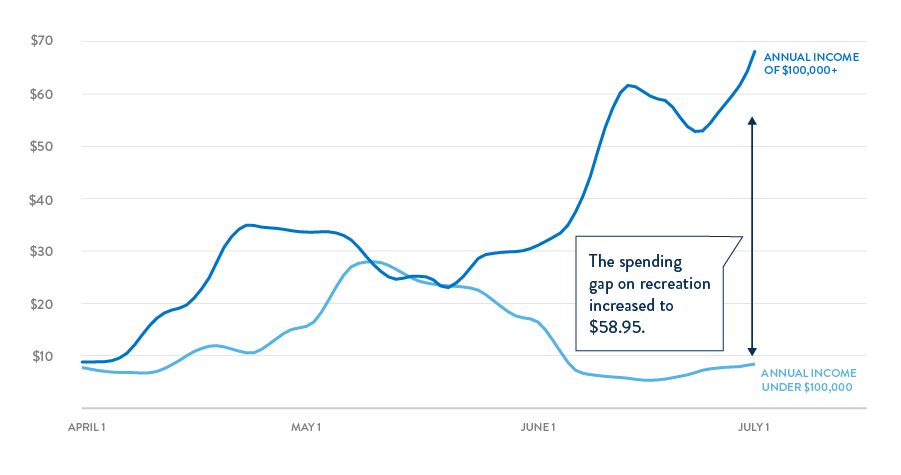

The categories of recreation and travel were two exceptions to the spending trends we observed in the Pulse data. The monthly average spent on recreation increased by over 280% ($8 to $31) and on travel by over 70% ($54 to $92) in the Pulse dataset. These growth areas appear to be driven by higher-income individuals: Those with household incomes over $100,000 per year saw a sixfold increase in the Pulse dataset, while those with household incomes below $100,000 per year saw no significant growth in spending on recreation. This could imply that the return to normal activities following COVID-19 lockdowns has been concentrated among higher-income households.

Q2 Recreation Spending Varied Based on Annual Income

Average recreation spending on credit cards rose over the quarter for people in households earning over $100,000 and remained flat for those earning less than $100,000

This line graph shows how recreation spending varied based on annual income between April and June 2021. Source: Pulse Transactional Dataset (April 1 to Jun 30, 2021). Sample size: 373 individuals, 150 from households that who have earned $100,000 or more (represented in the dark blue line), and 223 from households that who have earned less (represented in the light blue line). Notes: Household income is determined using data from Pulse surveys. Spending categories are retrieved through the Plaid application programming interface (API). There’s more information in the methodology below for additional notes.

Incomes outside of stimulus and tax payments stayed constant, except for those most negatively impacted by the pandemic.

Despite high consumer expectations and reports of rising wages throughout the second quarter of 2021, there was no dramatic change in incomes when removing tax refunds and late stimulus payments. At a national level, the U.S. Bureau of Economic Analysis reports that personal income declined in April and May 2021 compared with March 2021 (falling by 13.6% and 2.2%, respectively), but only recovered by 0.1% between May 2021 and June 2021. This decline is likely due to the fluctuation from the receipt of stimulus payments and tax refunds.

In the Pulse data, this overall decline in income during the second quarter of 2021 has simultaneously worsened income inequities. People who experienced housing insecurity, food insecurity, or went without medical care during the pandemic (which, in this brief, we will refer to as “experiencing hardship”) have consistently had lower incomes than those who did not experience these hardships. For the people experiencing hardship, there is a sizable and significantly negative trend in income over the second quarter of 2021. This implies that there is no immediate reprieve from the difficulties of the past year for those who have suffered most from hardships throughout the COVID-19 pandemic, and there may even be a further divergence in outcomes in the latter half of this year.

Q2 Liquid Account Inflows Changes for Those Who Did and Did Not Experience Hardships

Inflows to liquid accounts fell over the quarter for people who had experienced hardship, and remained steady for those who had not.

This line graph shows income changes for people who did and did not experience hardships between April and June 2021. Source: Pulse Transactional Dataset (April 1 to June 30, 2021). Sample size: 264 individuals, 67 who have experienced hardship (represented in the light blue line) and 197 who have not (represented in the dark blue line). Notes: Liquid accounts include checking accounts, savings accounts, prepaid cards, money market accounts, and cash management accounts. Hardship is defined as the experience of at least one of the following in the past 12 months: food insecurity, trouble paying housing costs, or foregone healthcare or medication due to costs. There’s more information in the methodology section below for additional notes.

While three months is a short period of time for recovery to occur, reported macroeconomic trends led to the expectation of a small but meaningful increase in incomes over the quarter. Job growth accelerated from April to June 2021 with a preliminary 1.2% growth in total nonfarm employment since the end of the first quarter. Reservation wages (the minimum wage people would accept at a new job) also grew, driving up wages to attract workers back to frontline roles and increasing average wages and salaries by almost 1%. Further, child care needs, which had kept 9% of Financially Vulnerable adults from being able to work, are beginning to be alleviated as schools and child care options began to reopen before summer break. As people return to work and changes in wages spread more broadly, it may take longer than a few months to influence incomes within the Pulse dataset. Time will tell how these economic shifts will interact with other factors, such as the deployment of child tax credits, and risks of further COVID-19 disruptions, such as capacity restrictions as states respond to the Delta variant.

Inflows and Outflows

Account inflows dropped sharply in April since the government administration of stimulus payments largely concluded, while outflows trended downward as individuals adjusted their spending accordingly.

Account Balances

Liquid account balances trended downward over the period of April 1 – June 30, 2021. This was likely due to individuals spending down high balances, which were caused by stimulus payments and tax refunds.

Credit Card Balances

Credit card balances remained consistent over the period of April 1 – June 30, 2021, with a median 30-day balance of about $1,100 per person.

Written by

-

Senior Associate, Policy and ResearchFinancial Health Network

Senior Associate, Policy and ResearchFinancial Health Network -

Senior Manager, Data

Senior Manager, Data